- Updated:

- Published:

The titans of iGaming: which brands dominate the Global gambling landscape?

Which iGaming brands truly hold the reins of the global betting economy?

To answer this, one must look beyond mere brand recognition. The modern gambling and sports betting ecosystem is a high-stakes arena where player acquisition and projected revenue dictate market survival. By analyzing data across dozens of active countries, Blask has charted the world’s leading operators based on revenue potential, new player acquisition, and geographic reach.

While certain established giants remain entrenched at the top, a quiet revolution is taking place underneath. Disruptors are claiming massive shares of emerging markets, and regional powerhouses are proving that hyper-focus can be more lucrative than global sprawl.

For industry professionals and affiliates looking to partner with top-converting platforms, tracking the best iGaming operators is essential to understanding where the real market power lies.

Below, we break down the definitive global rankings of the top iGaming brands, comparing the early months of 2026 to the same period in 2025 to reveal how the tectonic plates of the industry have shifted.

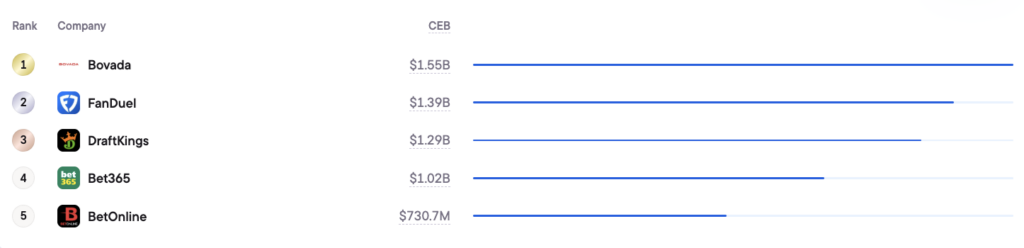

The revenue heavyweights: top brands by CEB

Competitive Earning Baseline (CEB) is a forward-looking metric that harnesses AI-driven insights —evaluating market trends, consumer behavior, and competitive dynamics — to project a brand’s realistic revenue potential.

When it comes to financial scale, the American offshore and regulated markets cast a long shadow over the rest of the world. Yet, the gap between the top contenders is beginning to narrow.

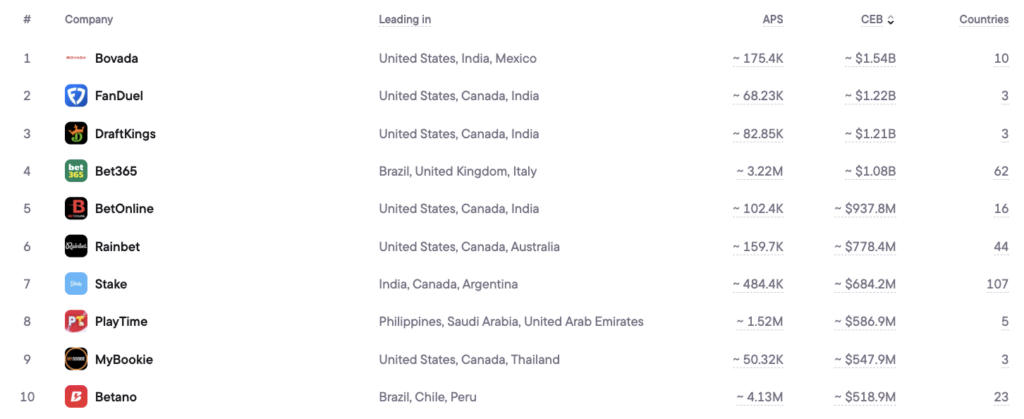

Top 10 brands by CEB (Jan–Feb 2026):

Bovada remains the undisputed king of potential revenue. But its slight dip from $1.55B in early 2025 suggests that a ceiling may exist, or that increased regulatory pressure in the US market is finally making a dent.

FanDuel and DraftKings follow closely, holding their duopoly over the legalized US sports betting landscape, though both have seen a mild cooling compared to their 2025 CEB peaks.

Conversely, European and international giants like Bet365 and the crypto-forward powerhouse Stake have demonstrated robust upward momentum, cementing their influence across a highly diversified global player base.

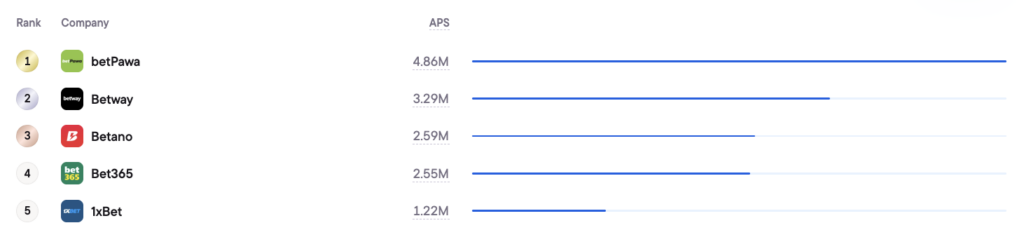

The acquisition engine: top brands by APS

Acquisition Power Score (APS) acts as a barometer for player conversion. It aggregates search trends, social media momentum, and market positioning to measure how effectively a brand attracts new customers.

While American brands dominate revenue, the battle for sheer audience volume is being won in emerging markets — primarily across Africa, Latin America, and Asia.

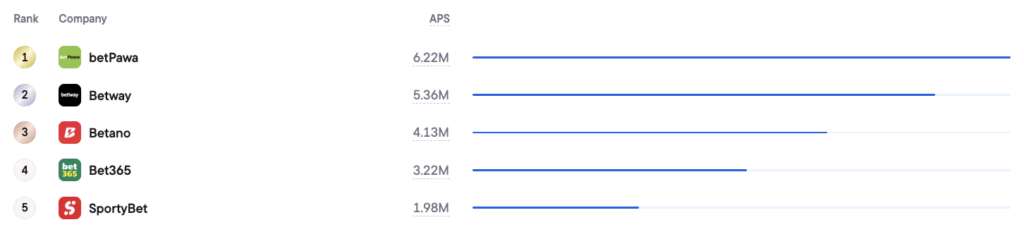

Brands by APS (Jan–Feb 2026):

The story of global player acquisition is written by betPawa and Betway. Focused heavily on the African continent, betPawa’s ability to draw in over 6 million new players in a two-month window is staggering.

Meanwhile, Betano’s aggressive expansion, fueled by major sports sponsorships across Latin America and Europe, has pushed its APS over the 4 million mark, solidifying its reputation as one of the fastest-growing brands on earth.

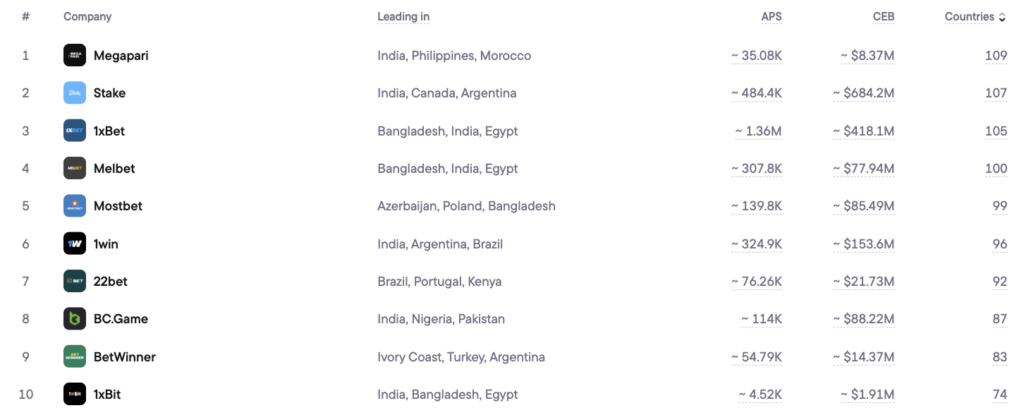

The global footprint: presence across borders

Does being everywhere mean winning everywhere? The data paints a complex picture. Some brands operate in over 100 countries, leveraging a blanket approach to capture disparate pockets of revenue.

The most global iGaming brands (Jan–Feb 2026):

The correlation between sheer geographic reach and top-tier revenue is surprisingly weak. Noticeably absent from the top of the revenue (CEB) charts is Megapari, despite its presence in 109 countries. Meanwhile, FanDuel and DraftKings operate in only 3 countries but pull in over a billion dollars in CEB each.

However, crypto-casinos like Stake manage to strike a rare balance: operating in 107 countries while simultaneously pulling enough high-value players to rank 7th globally in total revenue.

Year-over-year: the 2025 vs. 2026 power shift

Comparing the early months of 2025 to 2026 reveals a fascinating maturation of the industry. The post-pandemic explosion has settled into a strategic ground war.

The revenue (CEB) story: In 2025, the top five revenue spots were virtually identical to 2026. However, looking at the raw numbers, we see a fascinating trend. Bovada, FanDuel, and DraftKings saw a slight contraction in their CEB, likely due to market saturation and tightening advertising regulations.

Yet, brands like BetOnline surged, growing from $730.7M in 2025 to $937.8M in 2026. Stake similarly climbed the ladder, jumping from $598M to $684.2M.

The acquisition (APS) story: Player acquisition is accelerating at a breakneck pace for brands targeting emerging markets.

- betPawa grew its acquisition power from 4.86M players in early 2025 to 6.22M in 2026.

- Betway experienced a massive surge, climbing from 3.29M to 5.36M.

- Betano leaped from 2.59M to 4.13M, proving that strategic market entries (like Brazil and parts of Europe) yield immense dividends.

What truly matters in the race for iGaming supremacy?

Intuition suggests that the most profitable brands should be the largest ones, and that maximum earnings require a maximum global footprint. The reality, as the data proves, is far more nuanced.

It’s not about how many markets you are in; it’s about the value you extract from them.

Brands like FanDuel and Bovada demonstrate the immense power of focusing heavily on high-value, high-GDP markets (the US and Canada). Conversely, operators like Stake prove that a sprawling, borderless approach can succeed if built on a universally accessible framework like cryptocurrency.

The rankings illustrate that simply planting a flag in a new country does not guarantee success. As regulatory frameworks tighten and player acquisition costs rise globally, the next chapter of iGaming will favor those who prioritize depth of market penetration over mere breadth.readth.