- Updated:

- Published:

Middle East conflict registers in Gulf iGaming demand

As armed conflict escalated across the Middle East in late February 2026, Blask data registered a sharp drop in iGaming search demand in Qatar and the UAE and the signal is now spreading toward Azerbaijan.

Most demand shifts in iGaming have a clear cause: a sports event, a regulatory change, a new operator launching. What’s happening across the Gulf right now doesn’t fit any of those categories. There’s no new regulation. No major sporting event has been cancelled. The driver is purely macro — a military conflict reshaping consumer behavior in real time.

Blask data from the two weeks following the escalation that began on February 28 shows consecutive declines in iGaming demand across Qatar and the UAE.

In Qatar, the drop deepened from –23.2% in the first week to –28.1% in the second. The UAE registered –25.5% over the same period. Azerbaijan, which sits at the edge of the conflict zone and shares a long border with the region, is showing early signs of the same contraction.

This is a structural story worth examining. The Blask Index is picking up a signal that goes beyond sports calendars and licensing news.

What happened in late February

On February 28, 2026, military strikes hit the region, triggering retaliatory attacks that spread across six Gulf nations. Kuwait, Bahrain, Qatar, and the UAE moved to high alert. The conflict remained active through March, with Gulf states warning of a military response while stopping short of direct involvement.

The economic fallout was immediate. Global markets sold off. Gaming stocks dropped across the board, with the Roundhill Sports Betting & iGaming ETF falling over 2%. Wynn Resorts and MGM, both building multibillion-dollar resort projects in the UAE, began monitoring the situation closely.

For iGaming operators, the less-covered story is what happened to consumer demand — not investor sentiment.

What Blask Index measures

Blask Index is an AI-enhanced demand signal derived from search activity across iGaming brands. It measures how much user interest operators generate in a given market — behavioral demand from real users, before that demand converts to bets or revenue. Because it’s a leading indicator, it responds to market conditions faster than financial reporting or registration data.

That’s exactly what makes the Gulf data notable. Blask Index didn’t drop because operators changed their product or regulators tightened the rules. It dropped because players stopped searching.

Qatar: a two-week slide

Qatar’s iGaming market entered 2026 on a growth trajectory. The full-year 2025 Blask Index for the country totaled 3.2 million, with 111 active brands competing for demand.

Into early 2026, year-on-year growth was running above +60%. The market’s Competitive Earning Baseline (CEB) — Blask’s estimate of how much operators should be earning based on brand strength and competitive positioning, not internal accounting — reached $134M for Q1 2026 ($67M–$336M range).

Then the escalation hit.

In the week immediately following February 28, Qatar’s Blask Index declined –23.2% against the preceding week. The following week, the drop deepened to –28.1%. The signal didn’t reverse — it widened. That’s a 4.9 percentage point deterioration in seven days.

Two patterns stand out. First, the decline isn’t explained by a sports calendar gap — there was no equivalent pause in February 2025. Second, the number of active brands in Qatar fell from 111 to 91 between full-year 2025 and Q1 2026, suggesting operators pulled back or reduced visibility in a volatile environment.

UAE: the $261M market on pause

The UAE entered 2026 as one of the most closely watched iGaming markets in the world. A new federal gaming regulator — the General Commercial Gaming Regulatory Authority (GCGRA) — had been established under a 2023 federal decree, and international operators were moving into position ahead of a formal licensing framework. Demand was growing at over 50% year-on-year as recently as February 2026. Blask put Q1 2026 CEB at $261M ($131M–$653M range), up from $210M in the same period last year.

That trajectory stalled when drone strikes hit UAE territory.

The UAE registered a –25.5% decline in Blask Index demand in the post-conflict measurement window. The concern wasn’t hypothetical: Wynn Resorts and MGM both publicly acknowledged monitoring their multibillion-dollar UAE resort projects amid ongoing military activity. One operator temporarily suspended operations before resuming in mid-March.

Consumer demand tends to contract faster than operator infrastructure adjusts. The UAE’s –25.5% decline represents players stepping back from discretionary activity during a period of uncertainty — not a permanent structural change, but a measurable behavioral response to macro risk.

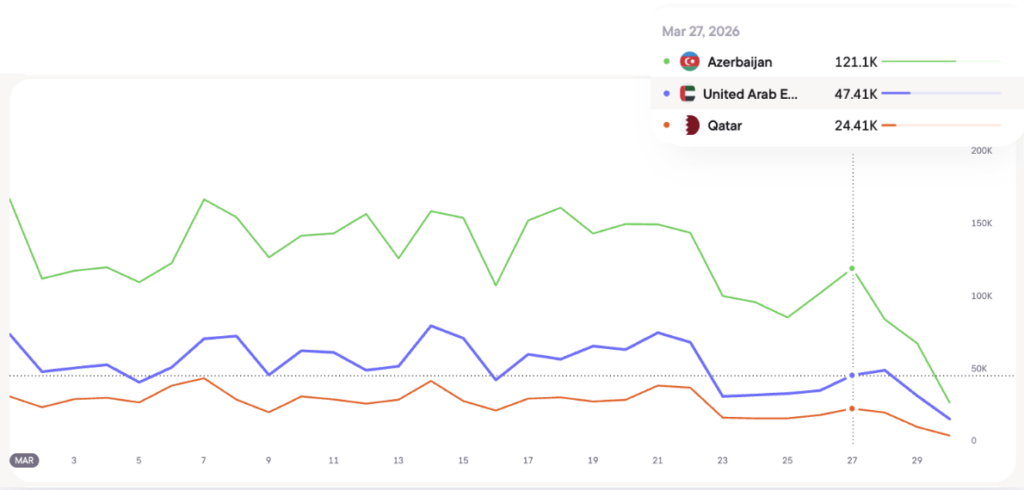

Azerbaijan: the spillover signal

Azerbaijan sits outside the Gulf but inside the radius of geopolitical contagion. It shares a 700km border with the conflict zone, has a population with significant cultural and ethnic ties to the region, and is directly implicated in the broader dynamics. Foreign Policy described the conflict as spilling beyond the Middle East to Azerbaijan as early as March 5.

The Blask data reflects this. Azerbaijan’s iGaming market is substantially larger than Qatar’s — the country logged 34 million in total Blask Index demand across 2025, with Misli, Mostbet, and eTopaz dominating.

Q1 2026 Blask Index came in at 7.3 million, tracking well above the Q1 2025 level of 7.0 million. But within that period, March 2026 brand-level data shows individual operators logging year-on-year declines of –11%, –85%, and –7% respectively — early indicators of the same demand compression visible in Qatar and the UAE.

CEB for Azerbaijan Q1 2026 was $112M ($67M–$247M range), down from $149M in Q1 2025 — a –25% year-on-year contraction in revenue capacity that tracks with the broader regional pattern.

The spillover thesis: when a major conflict reaches a country’s immediate geopolitical neighborhood, player behavior tightens before operators have time to react. Azerbaijan’s March data is two-to-three weeks behind the Gulf pattern. If it follows the trajectory, further compression is likely.

What this means for operators

Three observations from the data:

- Blask Index captures macro, not just sports. The common assumption is that iGaming demand is driven by a sports calendar and a regulatory environment. The Gulf data shows a third driver: geopolitical stability. When consumers face genuine uncertainty about physical safety and economic conditions, discretionary search activity — including iGaming — contracts. Blask Index picks this up at the market level before it shows up in revenue.

- The signal deepens, not recovers, in the short term. Qatar’s week-on-week decline went from –23.2% to –28.1%. This matters for operators managing acquisition spend: reducing activity in a down market makes sense, but the window between the first drop and the bottom is short.

- Spillover travels fast. Azerbaijan’s early data shows the same pattern emerging two to three weeks after the Gulf signal. Operators with cross-regional exposure — particularly those active in markets adjacent to the conflict zone — should treat the Gulf data as a leading indicator, not an isolated event.

The Middle East conflict is a macro event. The Blask Index is treating it as one.