iGaming market weekly report | July 13–19, 2026

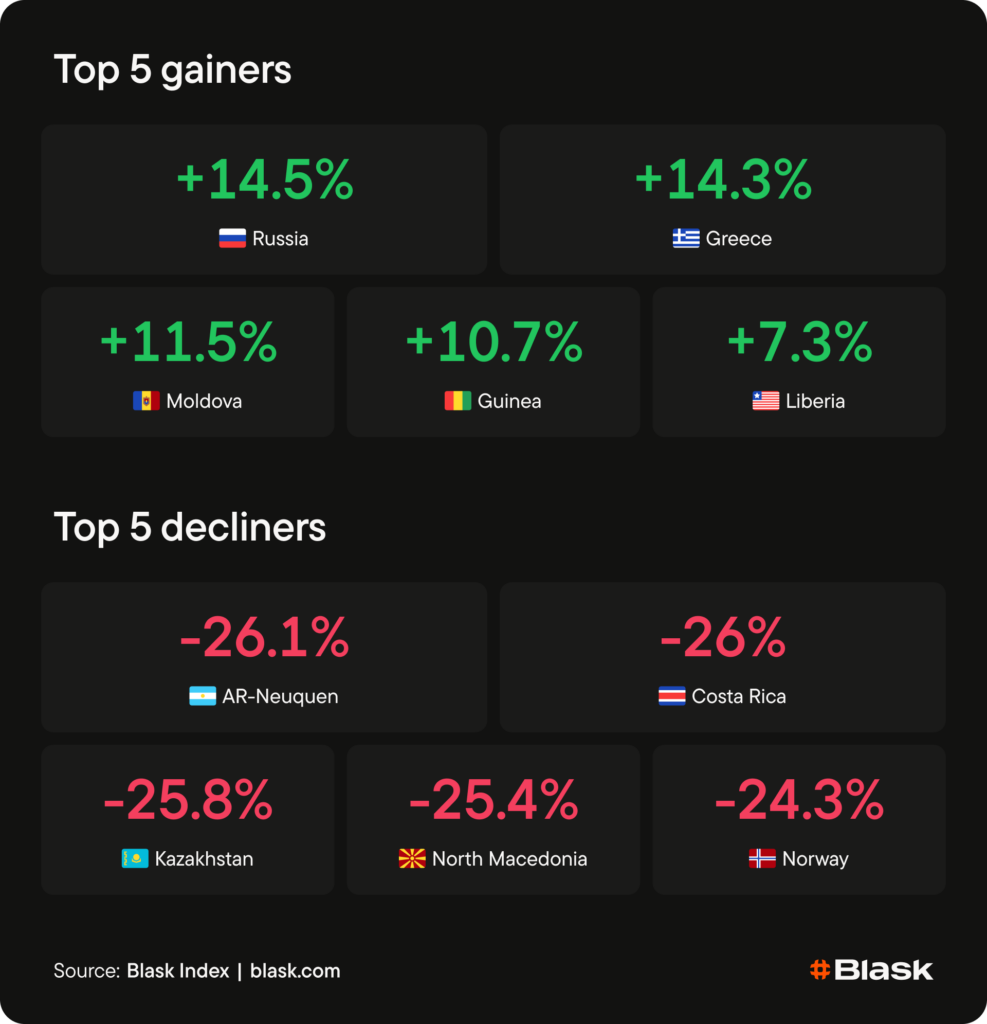

Domestic football calendars and mid-single-digit African momentum defined the upside, while exited World Cup sides, new statute days, and payment-rail friction set the downside. Russia (+14.5%) and Greece (+14.3%) led the gainers on Super Cup and Super League / EEEP catalysts. Moldova (+11.5%) bounced without a clear hook, and Guinea (+10.7%) plus Liberia (+7.3%) rounded […]

Domestic football calendars and mid-single-digit African momentum defined the upside, while exited World Cup sides, new statute days, and payment-rail friction set the downside.

Russia (+14.5%) and Greece (+14.3%) led the gainers on Super Cup and Super League / EEEP catalysts. Moldova (+11.5%) bounced without a clear hook, and Guinea (+10.7%) plus Liberia (+7.3%) rounded out the board on AFCON-qualifier and national-team news.

Norway’s –24.3% was a clean event hangover after the England exit. North Macedonia (–25.4%), Kazakhstan (–25.8%), and Costa-Rica (–26%), and Neuquén’s –26.1% carried active suppression without reason.

| Interesting that Argentina and Spain — two World Cup finalists — didn’t appear in the top gainers. The logic tells that there should be a huge spike, but, surprisingly, they didn’t demonstrate a large growth. |

Top gainers

Russia +14.5%

Domestic football supplied the hook: Zenit St. Petersburg and Spartak Moscow contested the Russian Super Cup on July 18 in Nizhny Novgorod, finishing 1–1 before Zenit won 4–2 on penalties. The derby-grade final lifted Index momentum. Russia is a new entrant versus the prior week’s leaderboard.

Greece +14.3%

After the prior week’s –20.7% decline, Greece mean-reverted as two mid-week catalysts landed together. The first catalyst is the Stoiximan Super League 2026–27 fixture draw, posted on July 16. The second catalyst is the Hellenic Gaming Commission’s annual report the same week, which put 2025 GGR at roughly €3.07B with remote play at 38.8%.

Moldova +11.5%

Moldova enters the gainers list as a new name versus the prior week’s top 10. The 2026–27 Moldovan Liga opened on June 27 and continued through early July, but no discrete in-window fixture or policy shock stands out as the driver.

Guinea +10.7%

There was no trigger during the reporting window.

Liberia +7.3%

The same situation — no trigger found during the reporting window.

Top decliners

AR-Neuquén –26.1%

No province-specific regulatory shock or sports hook explains the print.

Costa Rica –26.0%

Costa Rica did not qualify for the 2026 World Cup, and also no clear country-specific trigger dated inside the reporting week surfaced.

Kazakhstan –25.8%

No clear in-window catalyst has been found.

North Macedonia –25.4%

Classic mean-reversion plus policy: after the prior week’s +17.0% surge, Index compressed as the updated Law on Games of Chance entered force on July 14, bringing giveaway permits, advertising limits, and the 500-metre school-distance rule into effect.

Norway –24.3%

Event hangover after a historic World Cup run: Norway stunned Brazil in the round of 16 on July 5, then fell 1–2 after extra time to England in the quarter-finals on July 11. These events took place before the reporting window, and there was no replacement fixture. As a result, Blask Index dropped.

Market spotlight: drift without a trigger

One of the brightest things of this week is that several countries posted a decline without clear in-window catalysts. Neuquén (Argentinian province) led the downside board at –26.1% even as Argentina advanced through the World Cup semi-final and into the July 19 final.

Costa Rica followed at –26.0%, its second consecutive top-decliner appearance after the prior week’s –25.5%, still without a dated sports or enforcement hook inside the reporting window.

Kazakhstan’s –25.8% sits in the same bucket: banks’ multi-month payment blocks and the Unified Betting Accounting System are the structural backdrop, but no fresh statute, raid, or fixture dated to July 13–19 explains this week’s specific print.

The last week of the FIFA World Cup meant fewer matchups. It led to the decline in bettors’ activity. This pattern is especially bright in small countries.

Regional snapshot

Europe

The region split between explained and unexplained prints. Russia (+14.5%), Greece (+14.3%), and Moldova (+11.5%) led the upside on the Super Cup, Super League / EEEP, and a technical bounce. North Macedonia’s –25.4% and Norway’s –24.3% were cleanly classified as law-day suppression and World Cup hangover. Azerbaijan’s –24.1% extended the eastern-European soft patch after a prior-week +12.3% appearance.

Asia-Pacific

No market from the region made the top-five gainers board. Kazakhstan’s –25.8% was the headline APAC move — and one of the week’s clearest drift prints, with no fresh in-window catalyst. Malaysia’s –21.8% reversed the prior week’s +24.5% surge and reads as mean-reversion rather than a new enforcement shock.

Africa

Guinea (+10.7%) and Liberia (+7.3%) held the regional upside on national-team news (CAF venue request; cancelled US friendly). The downside remained heavier: Morocco –24.1% and Angola –23.4% led continental compression without a single shared sports narrative tying the African decline board together.

Next week watchlist

Argentina / Spain — post-final mean-reversion

The July 19 World Cup final closes the tournament. Expect Index give-back in Argentina and Spain early in the July 20–26 window as event gravity expires without a replacement fixture of equal scale.

Drift markets — rebound watch

Neuquén (–26.1%), Costa Rica (–26.0%), and Kazakhstan (–25.8%) all compressed without a clear in-window catalyst. Markets that fall hard with no visible trigger often snap back sharply the following week.

North Macedonia — law-day follow-through

After the July 14 Law on Games of Chance entered force and Index fell –25.4%, the next print shows whether suppression deepens under enforcement or whether the prior spike’s hangover has already done most of the damage.

Methodology note

Blask Index tracks real-time iGaming player interest via AI-analyzed Google search data, updated hourly and filtered to remove low-intent noise (scams, complaints). WoW% measures momentum: positive indicates growing attention; negative indicates declining attention.