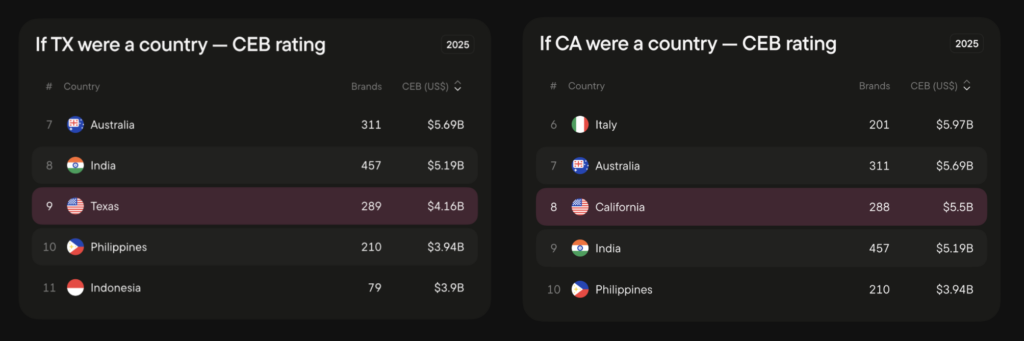

California and Texas, the two most populous states in the United States, together represent an estimated $9.7 billion in online gambling activity — all of it flowing to offshore, unlicensed operators and none of it generating state tax revenue or consumer protection.

The figures reframe the political stalemate over gambling legalization in both states not as a regulatory question but as a fiscal one. Every year the legislatures of California and Texas fail to act, their residents continue to fund an offshore gambling industry headquartered primarily in Curaçao and Antigua while the states collect nothing.

Two markets, zero rules

California’s estimated online gambling market reached $5.5 billion in 2025. That would rank it eighth globally — between Australia and India. Texas reached $4.2 billion. That would rank it ninth, between India and the Philippines. Together, the two states generate more gambling activity than all of Canada’s licensed operators combined.

Neither state permits online casino gambling.

Texas bans virtually all commercial gambling. California has spent a decade failing to pass workable legislation. Its most recent attempt, Proposition 27, would have legalized online sports betting. Voters rejected it in 2022. The margin was 83 percent against.

Who profits from the void

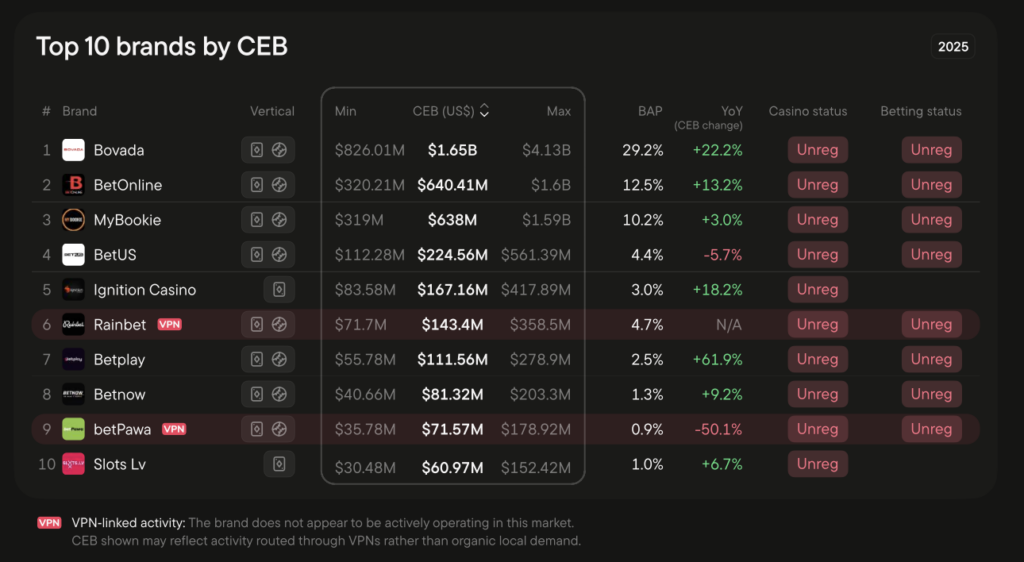

In California, Bovada commands an estimated $1.65 billion in Competitive Earning Baseline — roughly 29 percent of the state market. BetOnline accounts for 12.5 percent, or about $640 million. MyBookie captures 10 percent. The top ten brands in California are all offshore. Not one licensed operator appears in the rankings.

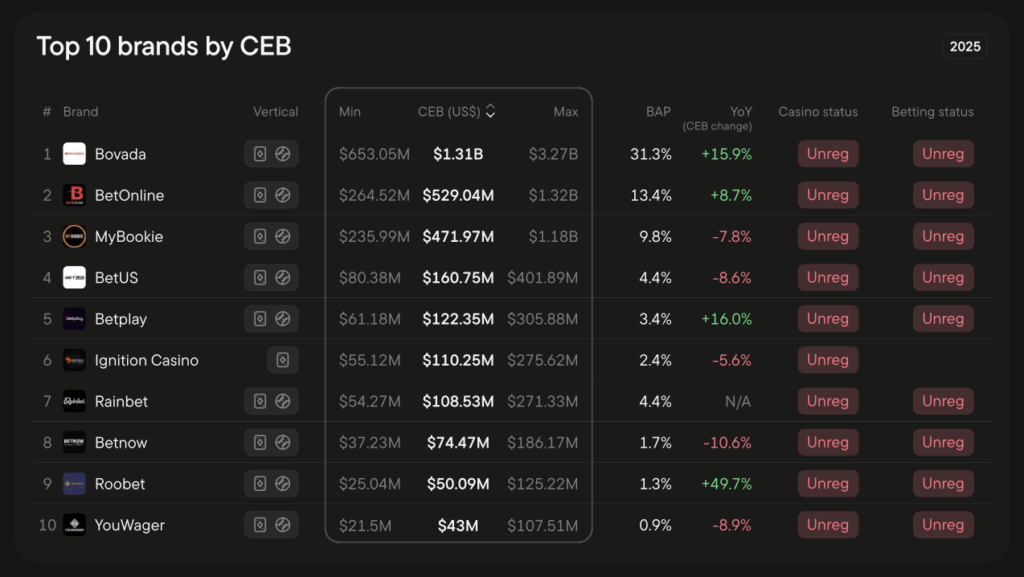

Texas is more concentrated. Bovada holds 31 percent of the state market, with an estimated $1.31 billion in CEB. BetOnline and MyBookie together add another 23 percent. In December 2025, those three brands alone captured more than half of all gambling demand in a state of 30 million people.

Why nothing has changed

The political obstacles differ by state, but both are durable.

Texas legislators meet only in odd-numbered years. The evangelical wing of the state’s dominant party has blocked gambling expansion for decades. “The Texas legislature does not meet in even-numbered years,” said Chris Altruda, senior analyst at Third Planet Media. “Consensus in California borders on impossible, especially with the mobile question.”

California’s problem is structural. Federally recognized tribes hold exclusive rights to operate slot-machine-style games under compacts negotiated with the state. Many tribes oppose online casino legalization. They fear it would cut into their land-based revenue. Commercial operators argue any tribal-only framework is unconstitutional. Neither side yields. The result is a decade of legislative paralysis.

Texas has no tribal gaming to complicate the picture. Its opposition comes from social and religious conservatives. The outcome is the same: no movement.

The cost, in numbers

Both markets keep growing despite the absence of regulation. California’s estimated CEB rose 13.2 percent year-over-year in 2025. Texas grew 4.3 percent. Offshore operators captured all of it.

A comparison makes the fiscal cost concrete. Michigan has roughly one-quarter of California’s population. It generated $4.9 billion in online gambling activity in 2025. About 75 percent flowed to licensed operators. At a 20 to 25 percent effective tax rate on gross gaming revenue, that translates to roughly $750 million in annual state tax revenue. California, four times larger, generates zero.

Offshore operators have no obligation to verify player ages. They do not check for problem gambling indicators. They do not maintain segregated player funds. They pay no taxes on their earnings. The market in both states runs entirely outside any consumer protection framework.

What the Blask data makes visible — perhaps for the first time with real precision — is the full scale of what California and Texas forfeit every year, and exactly who collects it instead.