Finland just made official what the market already expected. Parliament approved the gambling reform bill, the licensing process has opened, and one of Western Europe’s last state monopolies is winding down. The competitive model is coming — the only question now is timing.

For the European iGaming industry, this is one of the largest regulatory openings of the year. Finnish players are set to gain access to a competitive licensed market for the first time — and the window for operators to establish position is already closing.

A $645M market that’s been half-open for years

Before the first new license is even issued, the Blask data tells a revealing story about where Finnish demand already lives.

In 2025, Finland’s online gambling market generated an estimated $645M in estimated revenue (CEB), with approximately 2.9M new customer acquisitions across the full brand landscape (APS). Veikkaus, the state monopoly, captured roughly half: $319M in CEB, 1.43M APS — a dominant but no longer unchallenged position.

The other half has been quietly going somewhere else.

Throughout 2025, offshore brands — those operating in Finland without a local license — captured between 40% and 43% of total market demand, as measured by Blask Index. In any given month, more than four in ten Finnish searches for gambling brands were directed at operators with no formal presence in the market.

That’s not a rounding error. That’s a structural signal: Finnish players have already made their preferences known. The reform formalizes a competitive reality that has existed in consumer behavior for years.

December 2024: the offshore spike

The months leading into 2025 are worth a closer look. For most of 2024, offshore demand ran at around 39–42% BAP — elevated but stable. Then it spiked.

By October and November 2024, offshore BAP climbed to 48%. In December 2024, offshore brands briefly overtook the onshore monopoly: 54.3% of total Finnish brand demand flowed to unlicensed operators — the first time in the data that offshore exceeded onshore. It settled back below 43% in January 2025, but the signal was clear.

The player base didn’t wait for the reform to arrive.

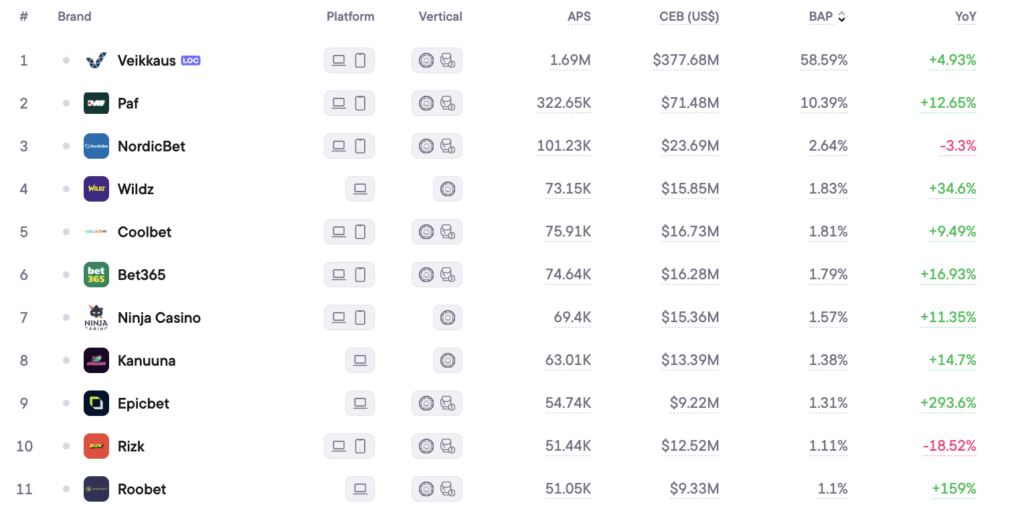

Who’s already winning the attention race

With 239 active brands tracked in the Finnish market, the pre-liberalization competitive landscape is already crowded — and already stratified.

The established players holding ground:

- Paf (#2): +12% YoY demand growth in 2025, $60.9M CEB — steady and gaining

- Bet365 (#6): +17% YoY, $16.3M CEB — consistent brand strength across borders

- NordicBet (#3): -3% YoY but still $23.7M CEB — still well-positioned regionally

The aggressive newcomers already in the top 25:

- Wildz (#4): +37.5% YoY — one of the fastest-growing established casino brands in Finland, $13.4M CEB

- Epicbet (#9): +398% YoY — launched in May 2024, went from near-zero to 43,000 estimated APS within 12 months

- Roobet (#11): +299% YoY — $7.8M CEB, crypto-native brand attracting heavy interest

- Pelikioski (#24): +1,25K% YoY — launched November 2024, broke into the top 25 in a single year

These are not small movements. Epicbet and Roobet both generated triple-digit YoY growth without a Finnish license, in a monopoly market. When a license becomes achievable, their head start in brand awareness becomes a material competitive advantage.

The brands losing ground before the starting gun:

- Casumo: -23.4% YoY

- Mr Green: -13.7% YoY

- Rizk: -13.6% YoY

- Betsafe: -8.0% YoY

Declining demand metrics ahead of a market opening are a warning sign. Operators entering a newly competitive market while their brand signals are trending down face a harder path than those who have been actively building Finnish audience share.

The baseline, set in data

Finland enters its liberalization era with a market that is larger than its regulated layer suggests. The ~$325M in annual revenue flowing to offshore operators is not lost to the market — it is the market, waiting to be formalized.

Blask Index data tracks the demand signal before a single new license is awarded. What it shows is an audience that has already voted: 239 brands are already competing for Finnish player attention, four of them with triple-digit YoY demand growth. The regulatory opening doesn’t create the competition. It just makes it official.