- Updated:

- Published:

Germany iGaming market 2026: $3B, 347 brands, and a regulatory war nobody is winning

Germany’s iGaming market in 2026 is, depending on who you ask, either a success story or a cautionary tale. The GGL — the country’s gambling regulator — published a study in March 2026 confirming that 77% of online gambling activity now flows through licensed operators. Ronald Benter, GGL CEO, called the results “confirmation of a fact-based regulatory approach.” The licensed operators who compete against offshore sites without deposit limits, without spin caps, and without five-second mandatory delays between bets had a somewhat different reaction.

Both of these things are true simultaneously.

Here’s what the Germany iGaming market actually looks like in 2026 — measured, not estimated.

Germany iGaming market size in 2026

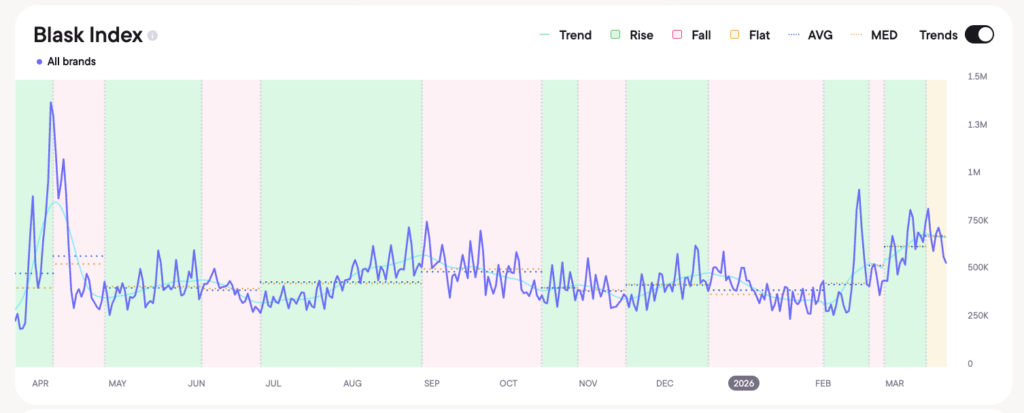

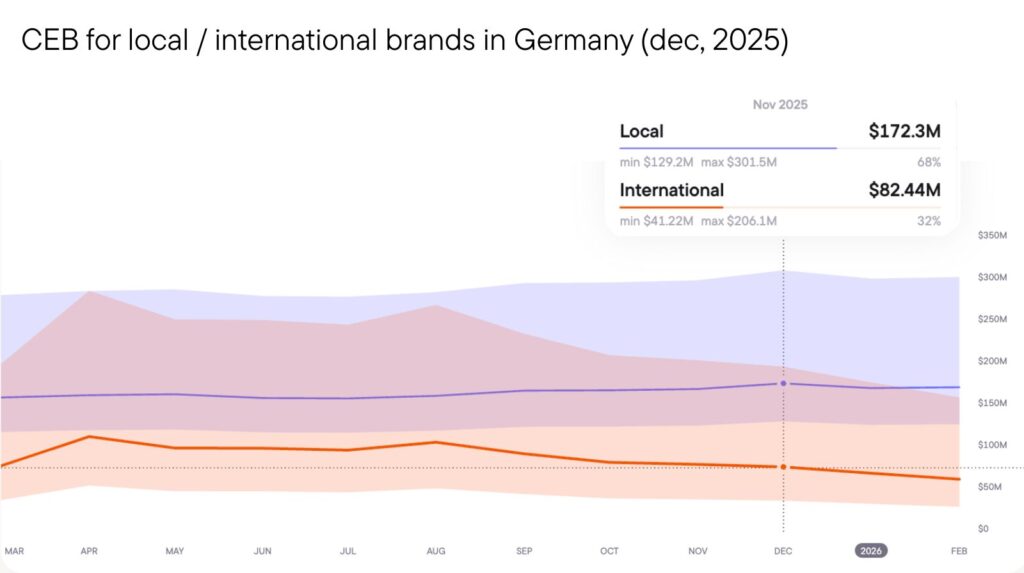

The Germany iGaming market generated an estimated $3.03B in competitive earning baseline (CEB) across 2025, with 8.38M active player acquisitions (APS) over the year. The total Blask Index — a demand-based signal derived from Google search behavior — reached 196M for the period, across 347 active brands competing for German players.

For context, Germany is one of the largest online gambling markets in Europe by absolute demand. The €14.4 billion gross gaming revenue figure for 2024 (online and land-based combined) positions it alongside the UK as a top-tier European market. The online segment specifically — where the regulatory tension is sharpest — accounts for the majority of growth.

The total market is not growing uniformly. The licensed segment is gaining volume. The offshore segment had a catastrophic surge in early 2025 and has since partially retreated. The story of Germany’s iGaming market in 2026 is largely the story of that swing.

Top iGaming brands in Germany (2025 full year)

According to Blask data for 2025, the Germany market is led by Tipico — the domestic champion that has held the #1 position since the GlüStV framework went live. What’s more interesting is what sits below it.

| Rank | Brand | CEB (2025) | YoY Growth | Note |

|---|---|---|---|---|

| 1 | Tipico | $562M | +2.6% | Domestic leader since 2008 |

| 2 | NV Casino | $347M | N/A | Offshore; launched Nov 2024 |

| 3 | Bet365 | $223M | +22.2% | Global, licensed in DE |

| 4 | Vulkan Vegas | $97M | +719.5% | Offshore; massive YoY |

| 5 | Verde Casino | $159M | N/A | Offshore; launched Feb 2025 |

| 6 | Merkur | $163M | +1.5% | Established German brand |

| 7 | Lotto24 | $135M | –4.4% | Licensed lottery operator |

| 8 | bwin | $108M | –8.4% | Declining established brand |

| 9 | Betano | $57M | +63.0% | Strong growth, fully licensed |

| 10 | Wunderino | $61M | +9.4% | Casino specialist |

A few things stand out.

- NV Casino is the second-largest brand in Germany. It launched in November 2024. It operates without a German license. It captured that position in under 13 months. The GGL cited Stake.com and WooCasino as frequently-mentioned unlicensed platforms — NV Casino is not even in that list from their study, which means the study’s survey data was already outdated relative to the actual demand picture.

- Vulkan Vegas is up 719.5% year-over-year. To be clear about what that number means: a brand that registered negligible demand in 2024 is now generating $97M in estimated annual revenue in Germany. It is offshore. It offers standard European casino stakes — nothing close to the €1/spin limit the GlüStV imposes on licensed operators.

- Betano is the one licensed success story in the growth column — +63% YoY on a fully licensed product, which suggests that product quality and brand investment can move numbers inside the regulated framework. More on why this matters later.

- Sportwetten.de deserves a mention: +699.97% MoM growth as of the latest data, a number that reflects either a tracking anomaly or a genuinely significant acquisition push. Worth watching in Q1 2026.

The 2025 offshore explosion — and why it happened

It’s 2025, and a single unlicensed offshore operator broke the German market’s channelization in one quarter. The offshore BAP (Brand’s Accumulated Power), i.e., demand share, ran at 18–25% throughout all of 2024. Then:

- November 2024: NV Casino launches in Germany, unregulated.

- January 2025: Offshore BAP reaches 29.5%.

- February 2025: 34.8%.

- March 2025: Germany’s Federal Administrative Court rules that IP blocking of illegal gambling sites is not legally mandated under the GlüStV 2021 — stripping the GGL of its primary enforcement tool.

- April 2025: Offshore BAP peaks at 61.9% — offshore demand exceeds licensed demand for the first time.

Time is a flat circle.

The April 2025 offshore peak is the most important data point in Germany’s recent iGaming history. It is a direct consequence of two simultaneous events: an unlicensed operator launching an unrestricted product into a market where the licensed alternative is constrained by €1 spin limits and monthly deposit caps, and the GGL losing the legal ability to block that operator’s domain.

From April 2025, the numbers started recovering:

- September 2025: offshore BAP falls to 31.2% — Bundesliga and Champions League return, licensed sports betting recovers sharply.

- October–November: 32.1% to 29.4%.

- December 2025: offshore BAP at 29.4% — the best Germany produced in the second half.

That recovery matters. It also leaves offshore at nearly 30% of branded demand in the best-performing month of the year.

The channelization data war

Well, depends what you mean by “channelized.”

The GGL’s March 2026 study says 77.03% of the market is regulated. The study was conducted by Blockchain Research Lab based on a 2,000-person survey and behavioral tracking methodology. GGL CEO Ronald Benter described the black market share as 22.97%, with the black market’s GGR reaching €547 million in 2024 — a 17% increase from €466 million in 2023.

A 17% increase in black market revenue while claiming channelization success is an interesting framing, if we are being honest.

The Handelsblatt Research Institute put the black market share at over 50% overall, reaching 70–80% for virtual slots specifically. A Hessian Fiscal Court estimate from 2024 put the virtual slots black market at over 80%. The DOCV (German Online Casino Association) and DSWV (German Sports Betting Association) issued a joint statement in March 2026 calling attention to “declining tax revenues and a growing black market.”

Blask’s branded CEB data for H2 2025 showed offshore demand averaging 35% of the total branded market — and this is the floor, measuring only operators with a measurable Blask-tracked digital presence. Unbranded, informal, and VPN-accessed offshore activity is additional.

Three methodologies, three answers. None of them is measuring the same thing. The GGL is measuring survey-reported behavior. Blask is measuring branded demand signals. Handelsblatt is measuring GGR flows. All three can be approximately correct within their own scope. The dispute is about what constitutes “the market.”

What unites all three methodologies: the black market is not declining in absolute terms. It is growing. The dispute is only about how large it already is.

The product restriction paradox

Germany’s GlüStV 2021 imposed a set of player protection measures that are, by design, the most restrictive online gambling framework in Europe:

- €1 maximum stake per spin on online slots

- 5-second mandatory interval between spins

- €1,000 monthly deposit cap across all licensed platforms (via a centralized monitoring system)

- No simultaneous multi-game play

- Strict advertising restrictions on licensed operators

These rules were designed to prevent harm. The €1 stake limit reduces loss velocity. The deposit cap prevents overspending. In theory, the design is coherent.

In practice, it makes the licensed German casino product structurally uncompetitive against every offshore alternative that exists. A recreational player who plays €5–10 stakes on online slots — the overwhelming majority of the player base — has no licensed option in Germany. Their only path to that product is offshore. The restriction intended to protect the 5–10% of players at risk of problem gambling has functionally excluded the other 90% from the licensed market.

The German industry associations have been saying this since 2021. Pretending like the data doesn’t confirm it at this point is wild.

The GGL is, to its credit, now examining this in the context of the 2026 GlüStV evaluation. Reform proposals under active discussion include relaxing the €1 spin limit, reconsidering the €1,000 monthly cap, and adjusting game speed restrictions. Operators including bet365, Tipico, and Entain-owned brands have consistently made the case that current product restrictions drive more harm than they prevent, by routing recreational players into unregulated environments with zero consumer protection.

The evaluation was initiated in 2025 and is expected to produce results by end-2026.

Check the real-time Germany gambling market overview, updated every month.

What the GlüStV 2026 Review Means for the Market

The 2026 review is not a rebrand. It is a formal scientific and legal evaluation of whether the 2021 framework achieved its objectives — specifically, whether channelization into the licensed market has been sufficient, whether player protection measures are proportionate, and whether the regulatory framework is commercially viable for licensed operators.

The ISA-Guide’s independent analysis of the review scope noted that approximately 38 licensed companies were active across sports betting and virtual slot games as of end-2025. The online casino segment (table games, roulette, blackjack) remains fragmented due to state-specific jurisdiction and licensing delays. The evaluation will specifically examine whether game certification timelines — described by operators as “often taking many months” — are suppressing innovation in the licensed market.

Three areas where regulatory change is most likely:

1. Stake limits. The €1 cap is the GlüStV’s most contested provision. Every independent study showing high offshore casino demand points to the same cause. Reform is not guaranteed, but it is being formally evaluated for the first time since 2021.

2. Deposit caps. The €1,000 monthly limit was designed as a universal player protection measure. The GGL’s own data shows that operators can apply for higher limits for a small percentage of verified users. The evaluation will assess whether the cap’s uniform application serves its stated purpose or simply sets the floor for offshore migration.

3. Enforcement mechanisms. After the March 2025 Federal Administrative Court ruling eliminated IP blocking, the GGL pivoted to host-based enforcement — targeting domain operators, payment service providers, and affiliates. By Q4 2025, over 930 domains had been actioned, 30+ payment blocking orders issued, and cease-and-desist orders sent to affiliates with fines up to €50,000. This scaled enforcement infrastructure moved the offshore number from April’s 61.9% to December’s 29.4% — a meaningful improvement. The question is whether the next phase requires legal strengthening, potentially via amendments to the GlüStV itself.

Competitive landscape: who’s winning in Germany

- The domestic establishment is holding, not growing. Tipico at +2.6% YoY and Merkur at +1.5% YoY are stable, but in a market that is structurally expanding, stable market share means losing ground relative to the total opportunity. Lotto24 (–4.4%) and bwin (–8.4%) are in active decline — the established European brands that relied on sports betting dominance are facing compression.

- The offshore disruptors are the growth story. NV Casino at #2, Vulkan Vegas at #4 with +719% YoY, Verde Casino entering at #5 in February 2025 — these are operators that either entered the German market without a license or operate in the regulatory gray zone. The top 5 brands by CEB in 2025 include two offshore-launched operators that did not exist in the German market twelve months earlier.

- The licensed growth plays are real. Betano (+63% YoY), NEO.bet (+55% YoY), and Lowen Play (+83.6% YoY) demonstrate that licensed operators can grow aggressively inside the GlüStV framework. These are brands investing in product, acquisition, and brand positioning in a constrained environment — and capturing incremental market share from declining incumbents like bwin.

- The newcomers to watch: Sportwetten.de’s extraordinary MoM growth spike and Stargames (+32.2% YoY) suggest that sports betting-focused and casino-focused licensed operators still have room to grow, particularly as the Bundesliga and Champions League calendar drives seasonal demand back to licensed platforms.

Germany iGaming Market 2026: bottom line

Germany’s iGaming market is large, contested, and at a regulatory inflection point. The $3 billion branded CEB figure represents the demand that analytics can track — the full market, including unbranded offshore and informal channels, is materially larger.

The offshore share fell from April 2025’s catastrophic 61.9% to December 2025’s 29.4% — a genuine recovery, driven by sports seasonality, scaled enforcement, and payment blocking. That recovery is real. A 30% offshore floor in the best month of the year (while licensed operators operate under a €1 spin limit) is also real.

The GlüStV 2026 evaluation will determine whether Germany’s regulatory framework evolves toward a product that can actually compete with the offshore market, or whether the current design continues to route the recreational casino player base offshore as a structural feature rather than an exception.

Tipico has held the market leadership position since 2008. NV Casino became the second-largest brand in the country in 13 months without a German license. That gap tells you everything you need to know about the current state of the Germany iGaming market in 2026.

The marathon, as the GGL puts it, continues.