When Parliament outlawed real-money gaming last August, consumer demand didn’t disappear. It migrated — to the offshore operators the law could never reach.

On August 21, 2025, India’s Parliament passed the Promotion and Regulation of Online Gaming Act. Three days later, President Droupadi Murmu signed it. The country had just made real-money gaming illegal for 450 million players — one of the most sweeping prohibitions in the history of digital entertainment.

Dream11, India’s largest fantasy sports platform, shut down its cash operations and asked users to withdraw their balances. Mobile Premier League suspended paid contests. PokerBaazi and Rummy Circle wound down their real-money formats. Thousands of engineers, marketers, and customer-service workers lost their jobs. Investors marked down billions.

What the law could not do was make people stop wanting to gamble.

The numbers the government did not anticipate

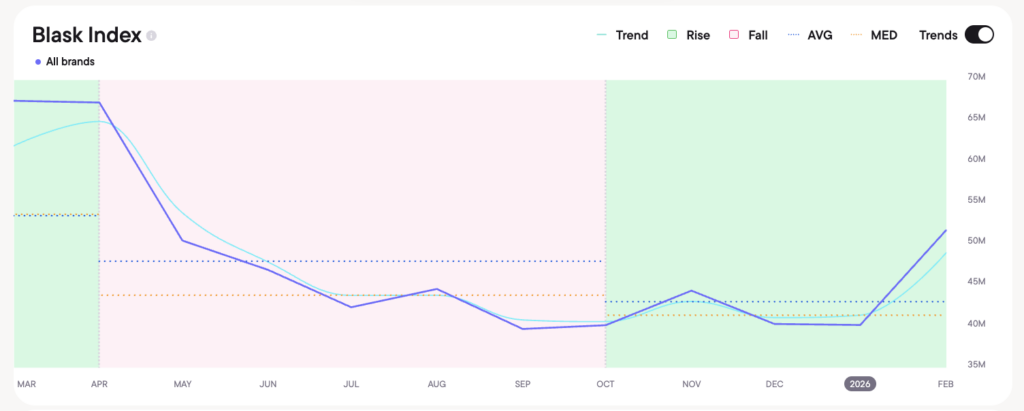

India’s aggregate iGaming Blask Index actually rose 5.3 percent in August 2025, the month the ban took effect.

| Month | Blask Index | Change MoM | Active Brands |

|---|---|---|---|

| March 2025 | 67M | — | 382 |

| April 2025 | 67M | −0.3% | 388 |

| May 2025 | 50,M | −25.0% | 392 |

| June 2025 | 47M | −7.1% | 390 |

| July 2025 | 42M | −9.7% | 421 |

| August 2025 (PROG Act signed) | 45M | +5.3% | 428 |

| September 2025 | 40M | −10.9% | 434 |

| October 2025 | 40M | +1.2% | 440 |

| November 2025 | 44M | +10.5% | 439 |

| December 2025 | 40M | −9.1% | 441 |

| January 2026 | 40M | −0.3% | 445 |

| February 2026 (pre-IPL) | 52M | +28.7% | 442 |

By January 2026, 445 offshore brands were actively competing for Indian players. That is 63 more than were active in March of the same year, before the law passed.

The market did not shrink. It reorganized.

A law that created a windfall for its targets

The PROG Act was written to protect Indian consumers. Its drafters cited addiction, financial ruin, and money laundering. Technology Minister Ashwini Vaishnaw said real-money gaming platforms “exploit users with false promises of profit.”

What the law actually accomplished was the elimination of India’s regulated, tax-paying, domestically accountable gaming operators — and the enrichment of the offshore platforms it had no jurisdiction over.

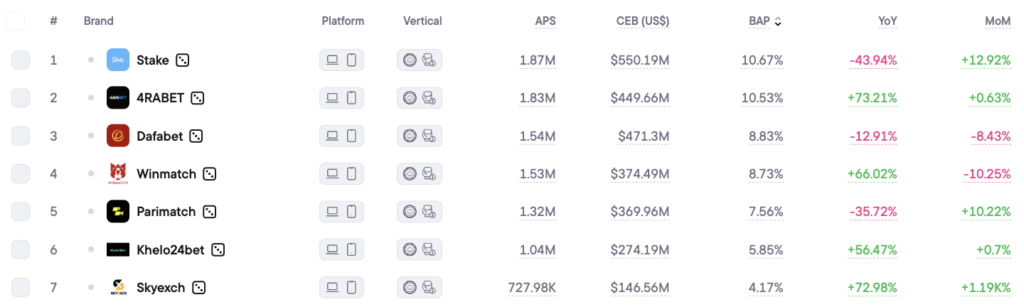

4RABET, a Curaçao-licensed operator with no Indian address and no Indian gaming license, finished the 12-month period ending February 2026 as the top brand in the country by consumer demand. It acquired an estimated 1.83M new Indian customers during that period, generating an estimated $450M in revenue. Its YoY growth was 73%.

Winmatch, another offshore operator, grew 66% YoY. Skyexch, an exchange-style betting platform, posted a 1,187% MoM demand surge in February 2026.

None of them pay Indian taxes. None of them are subject to Indian consumer protection law.

The offshore surge, measured

A CUTS International survey of 1,000 Delhi NCR residents, conducted in the months after the ban, found that offshore gambling usage rose from 68.3% of respondents to 82%. Daily engagement intensity — the share of users logging in every day — jumped from 3.4 percent to 42.3%.

Players were not deterred. They adapted. Telegram channels and WhatsApp groups replaced app stores as the distribution channels of choice. VPNs, already widely used in India, handled access. Encrypted payment rails processed deposits.

“It pushes fan engagement away from regulated Indian platforms into unregulated offshore spaces,” said Jaya Chahar, founder and chief executive of JCDC Sports, shortly after the ban took effect. “Which defeats the very intent of consumer protection.”

The enforcement mechanism, for its part, has still not been formally activated. Parliament moved fast. The Online Gaming Authority of India, the body tasked with actual oversight, has made no operational progress since its mandate was established.

Cricket, not policy, drives this market

Understanding India’s iGaming demand requires understanding one sport.

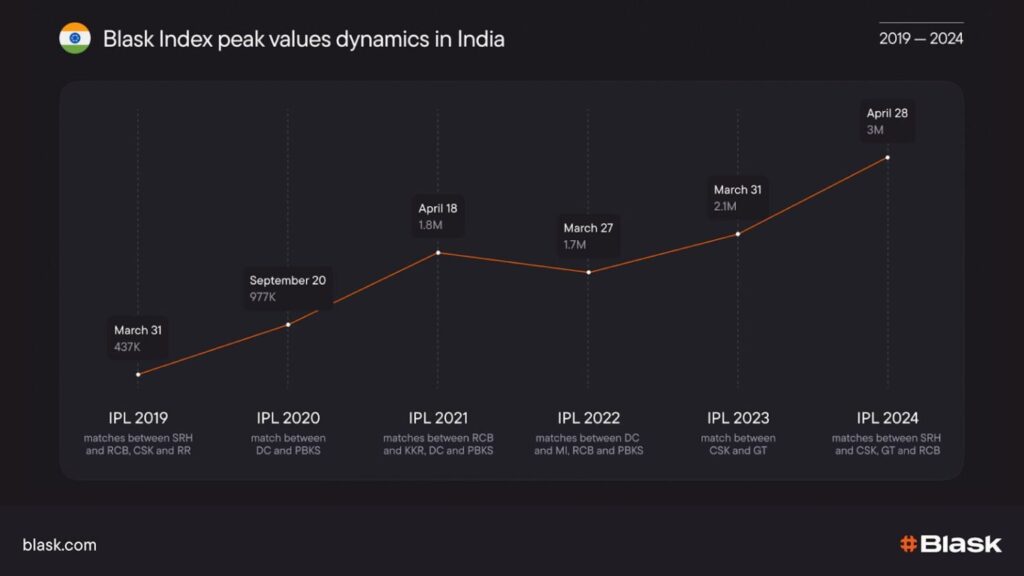

India’s Blask Index peaked at 67.5M in March 2025 — not because operators launched aggressive campaigns, but because the Indian Premier League began. IPL 2025 drew more than one billion viewers across television and digital broadcasts, with total watch time exceeding 840B minutes.

When the IPL group stage ended in May, the Blask Index fell 25% in a single month. By July it had dropped 37% from its March peak. The PROG Act, signed six weeks later, was less disruptive to aggregate demand than the end of a cricket tournament.

By February 2026, the index had recovered to 51.7M — a 29% monthly jump. IPL 2026, scheduled to begin in late March, had expanded to 84 matches over 67 days. Offshore operators were already running pre-season acquisition campaigns. Skyexch’s demand spike was not an anomaly. It was a marketing calendar.

Read also: IPL and Indian iGaming: an 18x growth story that repeats every spring

What the industry lost, and who gained

The domestic losses were real and severe. India’s real-money gaming sector had entered 2025 as a $3.7B ecosystem, employing more than 200 000 people across technology, payments, media, and content. The sector had been one of the few consumer internet segments where India produced globally significant platforms.

The government valued the broader online gaming market at ₹23,200 crore ($2.7 billion) for 2024, according to data published by the Press Information Bureau in February 2026 — noting it had outpaced India’s entire filmed entertainment industry in revenue. Projections through 2027 showed continued growth. Those projections now exclude real-money gaming.

Companies pivoted. Dream Sports, Dream11’s parent, began exploring free-to-play formats, esports, and global SaaS opportunities. Mobile Premier League shifted toward casual gaming. Nazara Technologies restructured. The pivot options, industry observers noted, are structurally smaller businesses.

The offshore operators needed no pivot. They had always been in the grey.

The market India cannot regulate away

Twelve months of Blask Index tell a consistent story. India’s total estimated iGaming acquisition across the March 2025–February 2026 period was 19.3M new customers (APS metric). Estimated combined revenue across all active brands reached $5.2B (CEB metric). Neither figure reflects a market in retreat.

The PROG Act succeeded in one sense: it ended the legal domestic real-money gaming industry. In another sense, the one that matters for consumer protection, it achieved the opposite of its intent. The players who had used licensed, KYC-verified, dispute-resolution-accessible Indian platforms moved to operators that verify nothing and answer to no one in New Delhi.

India is not the first country to discover this. The United Kingdom learned it in the 1990s with its initial offshore restrictions. Germany has spent years trying to contain a market that consistently exceeded its regulatory boundary. The pattern holds: prohibit the legal, and the illegal inherits the demand.

What comes next

IPL 2026 will be the first full cricket season since the ban. For offshore operators, it represents the most concentrated consumer acquisition opportunity in the Indian calendar — now without a single regulated domestic competitor.

4RABET, Stake, Dafabet, and at least 440 other brands are positioned for it. Their combined marketing spend, while not publicly disclosed, is visible in the demand data: February 2026 registered the sharpest single-month increase in the entire 12-month period.

The Online Gaming Authority of India has yet to take its first operational step. The enforcement notification that would activate the PROG Act’s criminal penalties — fines of up to ₹21 crore and three years in prison — has not been issued.

India banned an industry. The industry moved offshore, grew larger, and started preparing for cricket season.