India’s Supreme Court upheld 28% tax on the full face value of online real-money gaming bets. The decision turns the tax dispute into a retrospective claim against a market that has already been pushed outside the legal perimeter.

On May 27, 2026, India’s Supreme Court upheld 28% GST (Goods and Services Tax) on the full nominal value of bets placed on online platforms, including fantasy sports, rummy, poker, and casino-style games. The tax applies to the full stake amount, not to gross gaming revenue (GGR) or platform fees.

The court rejected the “games of skill” argument for GST purposes. It treated the use of money on an uncertain outcome as taxable, regardless of how the game is classified. Platforms were not considered intermediaries, meaning buy-ins and prize pools could not be deducted from the tax base.

The ruling applies retrospectively, including the period before India changed its GST regime on October 1, 2023. It also restored a $2.5B tax notice against Gameskraft. Across the sector, base tax demands are estimated at about $13.4B, with total exposure potentially reaching $30B after interest and penalties.

The decision came after India’s real-money online gaming ban entered into force on May 1, 2026. That shifts the angle: the state is not only taxing turnover instead of operator revenue, but also trying to collect retrospective tax from a market that no longer has a legal operating model.

A legal bill for an illegal market

GGR reflects the operator’s actual revenue after player winnings while face value is the full betting turnover before payouts. A 28% GST on face value can therefore exceed the revenue operators actually kept.

In regulated markets such as the UK and parts of the EU, gambling tax is usually tied to GGR or net win. India chose a turnover-based tax base. After the ban on real-money online gaming, that tax base now sits awkwardly against a market the government has effectively removed from the legal economy.

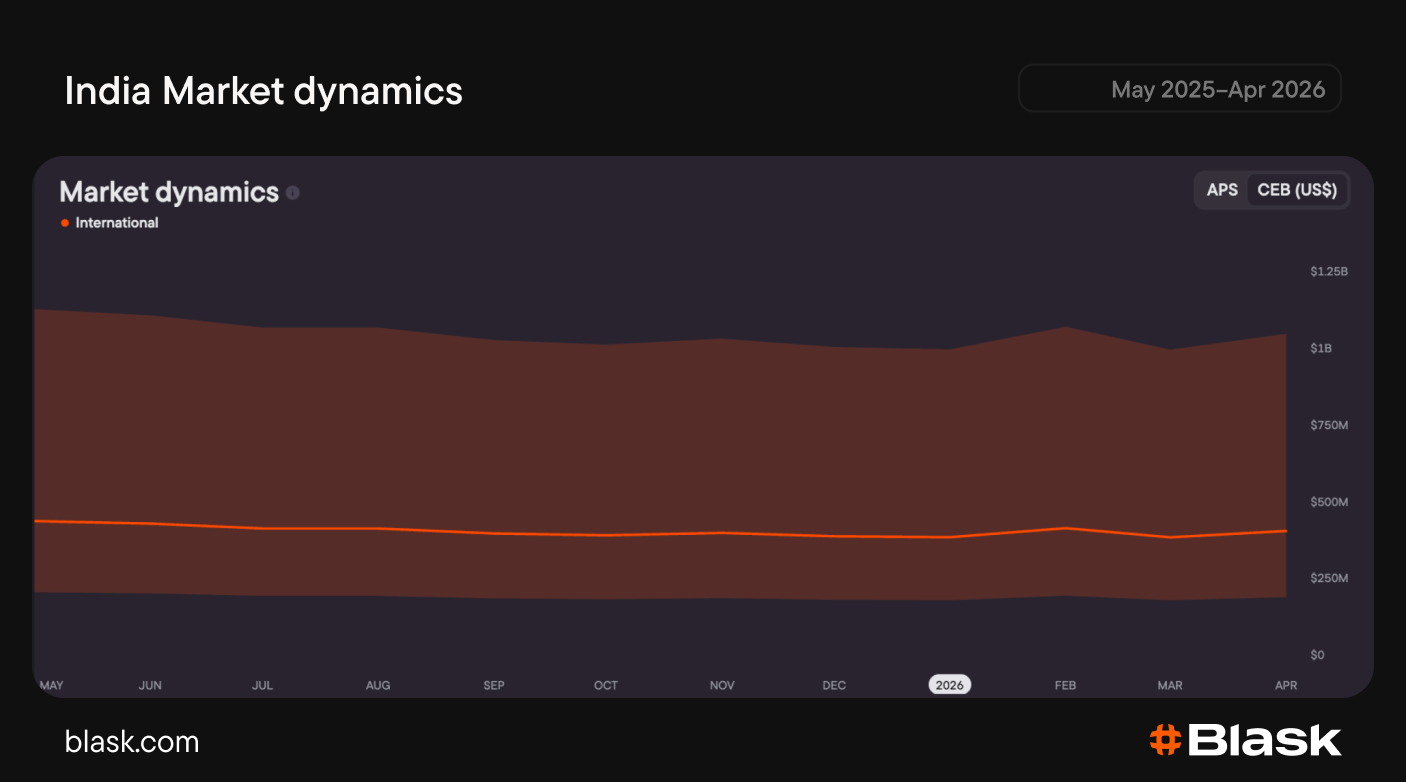

Blask data shows India’s online gambling market still had around $11.5B in CEB. But the tax claims are larger than that baseline: about $13.4B in base GST alone, before interest and penalties. With total exposure potentially reaching $30B, the retrospective bill is roughly 2–3 times larger than the projected market revenue baseline.

A structural break, not a margin hit

India is trying to collect tax from a market it has already made illegal. The Supreme Court ruling confirms that the tax base is not operator margin, but total betting volume. The retrospective element makes the pressure sharper: platforms may face liabilities from the period before the current regime, even though real-money online gaming no longer has a viable legal path in the country.

For operators, the ruling goes beyond a margin adjustment because it changes the basic economics of the market: real-money gaming is banned going forward, while past activity can now be taxed retrospectively on total betting volume rather than actual revenue. Search demand may still exist, but the model around it has been broken from both sides: the market is banned going forward, while past activity is being taxed retrospectively on turnover.