- Updated:

- Published:

March Madness betting 2026: which sportsbooks actually won the attention race

Blask Index data tracks how the NCAA Tournament moved consumer demand across U.S. sportsbooks — and what the numbers say about which operators are still growing.

The American Gaming Association estimates $3.3 billion in legal wagers will be placed on the 2026 NCAA men’s tournament. That’s 6% above the prior year and 54% above three years ago. Some analysts push higher: Matthew Bakowicz, former head of DraftKings sportsbook operations at Foxwoods, projects a record $4.5 billion, with H2 Gaming Capital forecasting $4 billion from legal sportsbooks alone.

Handle counts dollars. It doesn’t tell you whose app 68 million Americans opened first.

Blask Index data for the U.S. market, tracking consumer search demand across all registered iGaming brands, shows a tournament that worked for some operators and didn’t for others. The divergence is now large enough to be structural, not statistical noise.

What Blask Index measures

Blask Index is an AI-enhanced demand signal derived from search activity across iGaming brands. It measures behavioral interest before it converts to deposits or wagers — searches, brand queries, account-related activity. In the U.S. market, where operators don’t disclose real-time acquisition figures, it’s the most current cross-brand view of who is actually capturing player attention. Annual figures represent the trailing 12-month Blask Index total; month figures represent accumulated index for the calendar month.

DraftKings: the tournament is working

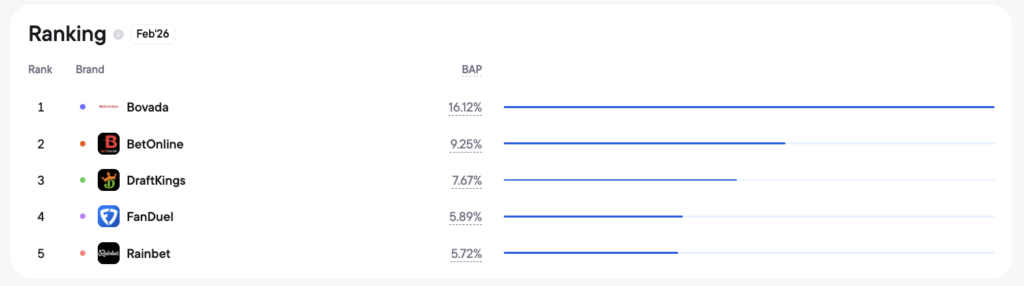

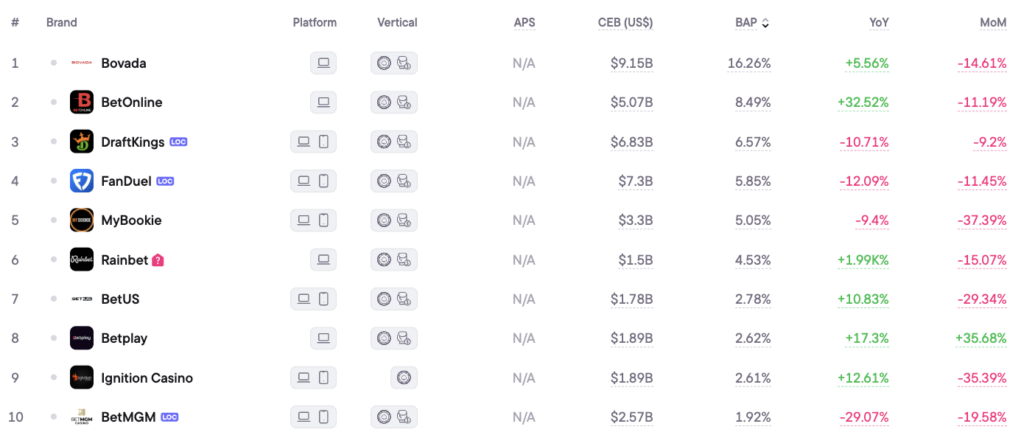

DraftKings enters March ranked third in U.S. iGaming consumer demand overall — behind Bovada and BetOnline, both offshore operators. Among state-licensed sportsbooks, it leads the market.

Its annual Blask Index stands at 6,985,483, down 15.2% year-over-year from 8,239,139. The direction is negative. But March tells a different story.

DraftKings’ Blask Index for March 2026 stands at 629,826 — 8% above its monthly average of 582,000 implied by the trailing annual figure. The tournament is pulling its March performance above trend.

On March 19, the first full day of First Round play, its daily index spiked to 26,18K from a pre-tournament baseline of roughly 19,900 — a 30% single-day lift that held through the opening weekend.

Bakowicz estimates March Madness produces a 45–60% jump in weekday handle and as much as a 200–250% spike on weekends. The Blask gain is more modest — demand doesn’t scale linearly with handle — but the direction confirms the same pattern: attention concentrates around the tournament and stays elevated across 67 games.

Pricing is part of the story. A Citizens analysis of First Round lines on March 19 found DraftKings offered the lowest average vig at 4.57%, just ahead of FanDuel at 4.64%. Tighter margins compress short-term revenue but attract sharper bettors. For a brand competing on attention share, the tradeoff appears to be paying off.

FanDuel: below its own trend in March

FanDuel sits at rank 4 in the U.S. by Blask Index: 6,124,957 annual, down 18.5% year-over-year from 7,514,065. Its March 2026 figure stands at 483,559 — 5.3% below its monthly average of 510,413.

The tournament gave FanDuel a daily spike too: 21,06K on March 19 against a pre-tournament baseline of roughly 16,100. But the monthly total still came in below trend, which means the First Round bump wasn’t large enough to offset weaker surrounding weeks.

One year ago, FanDuel led DraftKings in monthly Blask demand. That relationship has reversed. DraftKings’ March figure (629,826) is now 30% above FanDuel’s (483,559). The gap is widening, and the tournament isn’t closing it.

On pricing, FanDuel posted a vig of 4.64% on First Round openers — marginally higher than DraftKings. Whether that contributed to the attention gap is unclear from the data alone. What the data does show is that the two brands that once traded roughly equal consumer attention in the U.S. are now on diverging trajectories.

BetMGM: spending isn’t moving the needle

BetMGM’s numbers require the least interpretation. Its annual Blask Index has contracted 35.4% year-over-year — from 3,071,419 to 1,983,828. Its March figure of 136,166 is 17.6% below its own monthly average of 165,319. The tournament, for BetMGM, is not a recovery event.

The brand offered up to $1,500 in bonus bets over ten days during the tournament window. That promotional spend isn’t showing up in search demand. Operators write checks; Blask Index tracks whether bettors respond.

BetMGM ranks 10th in the U.S. by Blask Index. Caesars Sportsbook has seen an even steeper decline — its annual Blask Index dropped 52.9% year-over-year, from 865,687 to 407,945. The regulated tier below DraftKings and FanDuel is contracting fast, and March Madness is not arresting that contraction for the brands experiencing it most acutely.

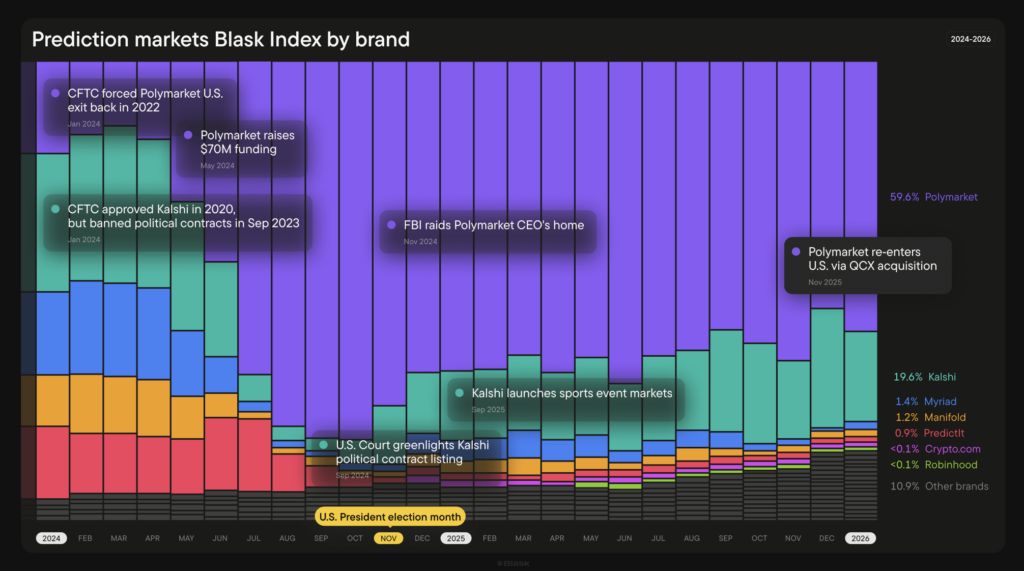

Prediction markets: $5.9 billion in one week

The most consequential development surrounding the 2026 tournament isn’t inside the regulated sportsbook tier. It’s outside it.

Kalshi and Polymarket — CFTC-regulated prediction market platforms operating outside state gambling frameworks — recorded $5.94 billion in combined notional volume in the week of March 16–22, the highest combined weekly total on record. Kalshi alone posted $3.4 billion, breaking its previous weekly record of $2.93 billion.

Before the first round tipped off, Kalshi had already cleared $60 million in championship futures trading. It launched a $1 billion bracket contest on March 19, the day the First Round opened.

Blask Index reflects the same trend in consumer attention terms. Kalshi’s annual Blask Index in the U.S. stands at 10,716,851 — up 76% year-over-year. Its March figure is 2,122,819. For comparison, DraftKings’ annual index is 6,985,483 and its March figure is 629,826.

These are different product categories. Prediction markets use exchange mechanics rather than spread lines. Their regulatory structure differs — CFTC jurisdiction rather than state gaming commissions. They serve partially different user profiles. But the attention competition is real: the same Americans searching for DraftKings are also searching for Kalshi, and Kalshi is growing faster.

Polymarket holds the largest Blask Index in the prediction markets segment at 33,351,161 annual — but it’s down 26.4% year-over-year. Kalshi, growing at 76%, is closing the gap.

The regulatory picture is escalating. A federal judge in Nevada remanded the state’s enforcement case against Kalshi back to state court, clearing the way for state regulators to pursue an injunction.

Senators Adam Schiff and John Curtis introduced bipartisan legislation — the Prediction Markets Are Gambling Act — that would ban CFTC-regulated platforms from listing sports and casino-style contracts. Kalshi responded by implementing new insider trading restrictions; Schiff and Curtis called them insufficient. Whether the bill advances is uncertain. The attention-market competition it’s trying to address is already underway.

DraftKings wins round one of the trademark dispute

The 2026 tournament arrived with litigation attached to its largest regulated sponsor.

On March 20, the NCAA filed suit in Indiana federal court seeking to block DraftKings from using “March Madness,” “Final Four,” “Elite Eight,” and “Sweet Sixteen” in connection with its gambling products. The NCAA argued that DraftKings’ use implied institutional endorsement of betting and undermined its longstanding opposition to sports wagering.

On March 26, Judge Tanya Walton Pratt denied the NCAA’s motion for a temporary restraining order. The court acknowledged the NCAA had made “a strong trademark infringement case” but found no showing of irreparable harm. Preliminary and permanent injunction claims remain pending.

DraftKings has used the terms openly since 2021, arguing they have become descriptive phrases embedded in the cultural lexicon — used by broadcasters, journalists, and fans independent of any gambling association.

The position the NCAA finds itself in is genuinely awkward. Its tournament generates an estimated $3.3 billion in legal wagers and draws 68 million Americans into legal betting participation. The institutional opposition to gambling is running directly against the commercial scale of the event that opposition surrounds.

What the data says

Three conclusions from March 2026 Blask data:

- The tournament still works as a demand catalyst for the right operators.

DraftKings’ March Blask Index of 629,826 is 8% above its own monthly average implied by the trailing annual figure. That’s the tournament doing what it’s supposed to do: pulling demand above trend when it matters most. - Not all regulated operators benefit equally.

FanDuel is 5% below its monthly trend in March. BetMGM is 17.6% below trend. The annual declines — –18.5% for FanDuel, –35.4% for BetMGM — are not being interrupted by the tournament. They’re accelerating in relative terms. - Prediction markets are now a measurable competitor for player attention.

Kalshi’s annual Blask Index growth of 76% and its $3.4 billion weekly volume record during the tournament are not marginal figures. They represent a platform that has grown its U.S. consumer search footprint to levels rivaling DraftKings — while the licensed sportsbook tier continues contracting.

March Madness remains the biggest event on the U.S. sports betting calendar. The question each year isn’t whether Americans will bet. It’s which brands they search for, which platforms capture that demand, and whether the licensed operators are the primary beneficiaries. The 2026 data suggests that last assumption deserves scrutiny.