Despite years of state-by-state legalization and record revenues from licensed operators, approximately two-thirds of American online gambling spending flowed to offshore, unlicensed platforms in 2025, according to new research from Blask that quantifies, the full scope of both the regulated and unregulated U.S. gambling market.

The finding undercuts a common assumption in the industry: that legalization, once enacted, naturally migrates players to regulated alternatives. It does — but slowly, incompletely, and only under specific conditions.

In most of the United States, the offshore market is not shrinking. It is simply growing more slowly than the domestic segment.

Where no law exists, offshore wins by default

The numbers are stark.

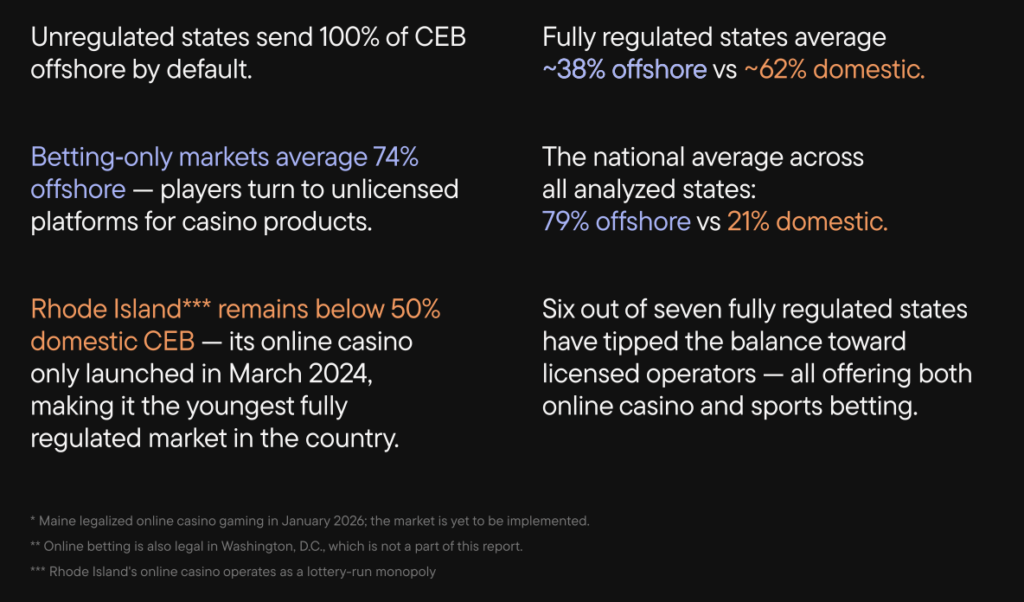

In states with no online gambling regulation, every dollar spent online goes to offshore operators. That is not a policy failure — it is a definitional outcome. Where no licensed option exists, all spending flows offshore by default. Legalization helps, but not as much as regulators tend to expect.

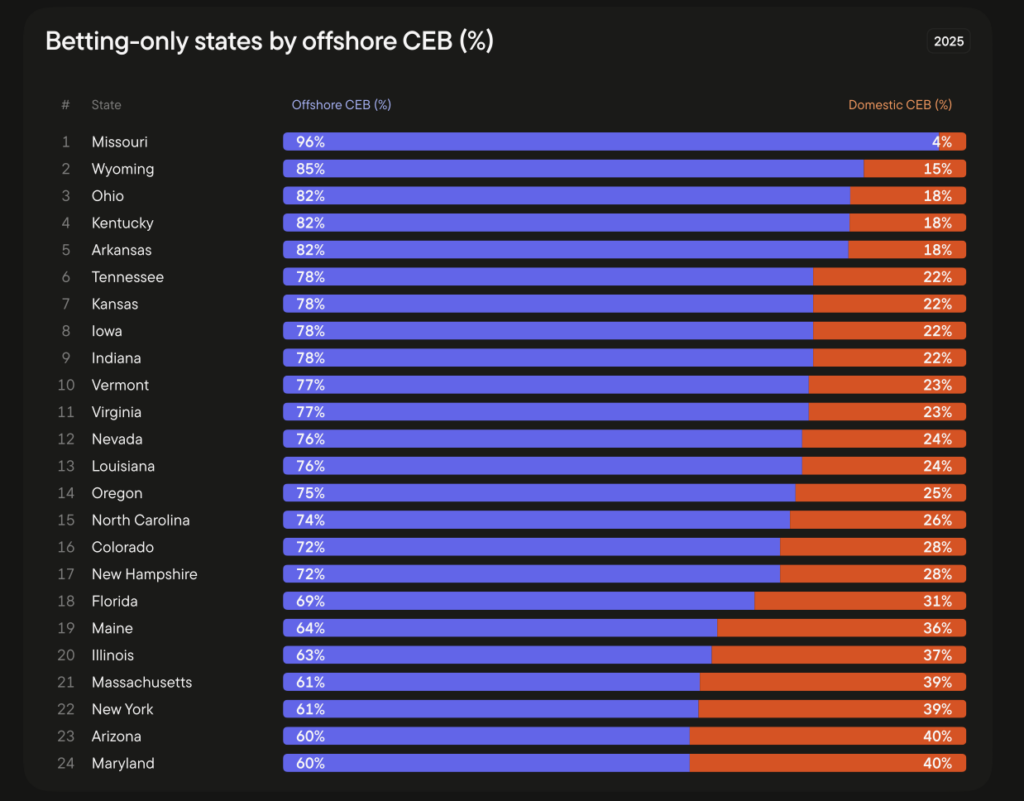

Twenty-four states have legalized sports betting but not online casino. That is currently the most common regulatory configuration in the country. In those states, the average offshore share is 74 percent. Players can bet on football or basketball through FanDuel or DraftKings.

But players who want slots, blackjack, or poker online have no licensed option. They go offshore.

The sports-betting-only ceiling

The Blask report tracks this pattern across all 24 sports-betting-only states. Just two — Maryland and Arizona — have achieved domestic CEB shares above 40 percent. The remaining 22 states capture less than two-fifths of their markets through licensed channels.

Missouri shows the extreme end. It launched mobile sports betting in December 2024, and 96 percent of its estimated $1 billion online gambling market flows offshore. Wyoming sits at 85 percent offshore. Ohio has had legal sports betting since January 2023 and still sits at 82 percent offshore.

The absence of online casino licensing sets a structural ceiling that sports betting alone cannot break through.

Full regulation helps, but doesn’t finish the job

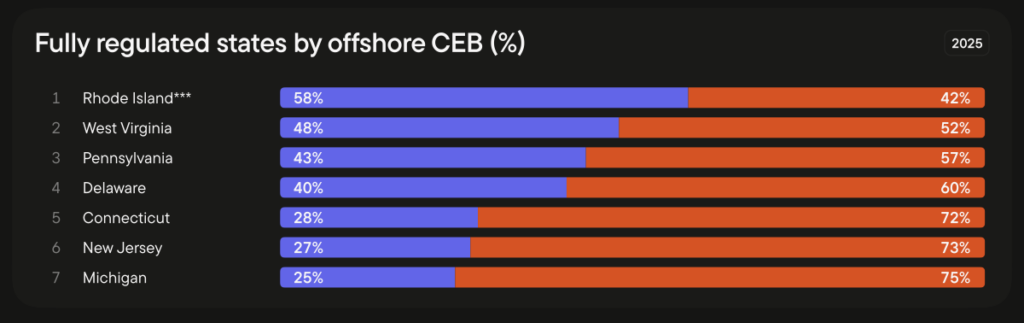

Only six states have achieved majority domestic market share: Michigan, New Jersey, Connecticut, Delaware, Pennsylvania, and West Virginia. All six offer both sports betting and online casino. Rhode Island added online casino only in March 2024 and sits just below 50 percent domestic.

Even in these fully regulated states, offshore platforms do not disappear. They shrink. Michigan leads the country at 75 percent domestic — but that means one in four Michigan gambling dollars still reaches an offshore operator.

Five years of full regulation, and the offshore market retains a quarter of the state.

Channelization is measured in decades, not months

Speed matters here. Michigan launched in January 2021 and now sits at 75 percent domestic after four years. New Jersey launched in November 2013 — twelve years ago — and sits at 73 percent. Rhode Island, the youngest market, is still below 50 percent after two years. The progression is slow, uneven, and does not follow a predictable curve.

The offshore segment grew 3 percent in 2025. The domestic segment grew 20.6 percent. Domestic growth outpaces offshore — but offshore still grew. The gap narrows. It does not close. Channelization works, but only on a timeline measured in years, often in decades.

Twenty-six states where gambling is already happening

Twenty-six states have not legalized any form of online gambling. In all of them, the gambling continues. It happens on offshore platforms that pay no state taxes, follow no state consumer protection rules, and face no state enforcement risk.

Three questions follow:

- Do state governments capture any revenue? No.

- Do players have consumer protections? No.

- Do operators follow responsible gambling standards? Not by state requirement.

In all three cases, unregulated states get nothing while offshore operators get the market.

Offshore is not passive — it adapts

The offshore market does not stand still as regulation advances. Bovada’s Brand Accumulated Power — Blask’s measure of a brand’s share of total search demand — declined in fully regulated states as domestic operators expanded. But Bovada responded by growing in unregulated markets. California, Texas, and Georgia each have no licensed competition. Bovada leads all three.

This adaptability matters. Offshore operators do not wait to lose market share. They shift their focus to the markets where licensed operators cannot follow. The top five offshore brands — Bovada, BetOnline, MyBookie, Betplay, and Rainbet — hold the majority of offshore CEB.

These are not gray-market curiosities. They run loyalty programs, marketing campaigns, and product operations that rival many licensed operators. The offshore market is organized, and it is not going away on its own.