Seven years after launch, licensed operators hold a majority of the market — but more than $2.4B in CEB still sits offshore.

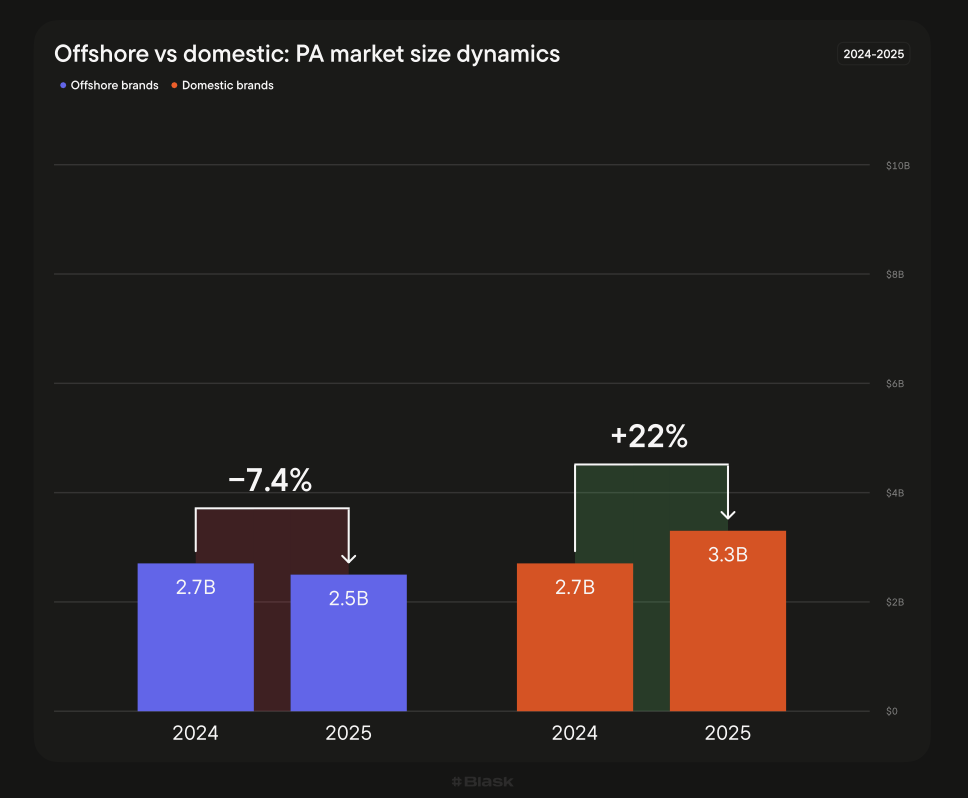

Pennsylvania launched its online gambling regulation in 2019, making it one of the earlier adopters of full-spectrum iGaming in the United States, and seven years later its licensed operators capture approximately 57% of the state’s$5.7B Competitor Earning Baseline online gambling market. A majority position achieved through sustained competitive investment by brands like FanDuel, DraftKings, and BetRivers, but one that still leaves more than $2.4B in state market value flowing offshore, according to new Blask data.

Pennsylvania’s seven-year trajectory, tracked comprehensively for the first time in the Blask report, illustrates both the promise and the pace limitations of gambling regulation.

The state ranks seventh globally by CEB — between Italy and Australia — and its domestic operators are growing consistently. But the offshore segment is not shrinking in absolute terms in most states; in Pennsylvania, it is now starting to decline, even as a substantial share of the market remains offshore and several billion dollars in potential tax base continue to sit with operators headquartered in Curaçao and Malta.

An early adopter of full-spectrum iGaming

Pennsylvania launched online casino and poker in July 2019 and online sports betting in May 2019, making it one of the first states to offer the full product suite.

Four out of the top five Pennsylvania operators hold local licenses, and the competitive market structure — with BetRivers, Rush Street Gaming’s Pennsylvania-focused brand, as a significant third player behind FanDuel and DraftKings — has driven sustained product investment.

The licensed leaders are still growing

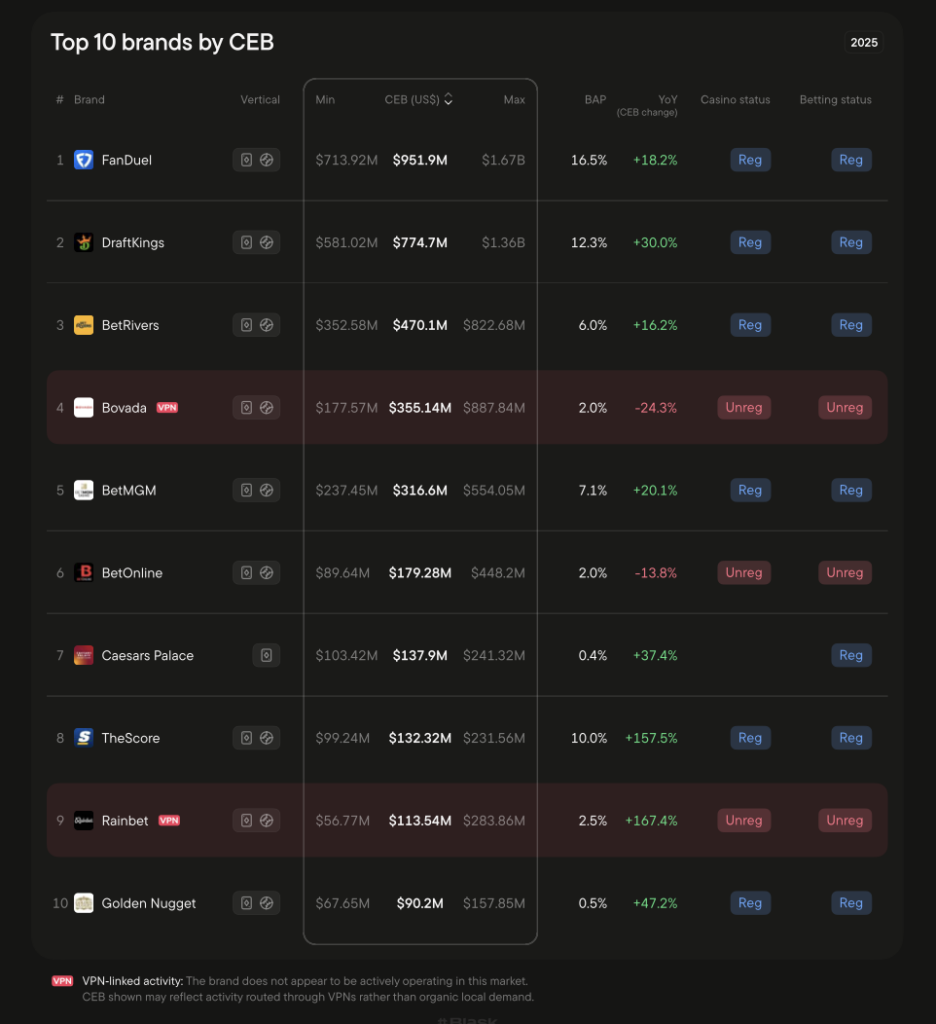

FanDuel leads Pennsylvania with an estimated $951.9M in CEB, growing 18.2% year over year. DraftKings grew 30% to reach $774.7M in CEB. BetRivers grew 16.2% to $470.1M in CEB. BetMGM grew 20.1%.

The licensed top four are all growing at double-digit rates in a state that has been regulated for seven years — a sign that the market is still expanding, not merely consolidating.

Offshore is finally starting to retreat

The offshore picture is more complex. Pennsylvania’s offshore CEB declined 7.4% year over year in 2025, making it one of a small number of states where offshore volume is actually shrinking.

That decline reflects the competitive maturation of the domestic market: operators that have had seven years to build loyalty infrastructure, Pennsylvania-specific promotions, and brand recognition are now more consistently retaining players who might otherwise drift to offshore alternatives.

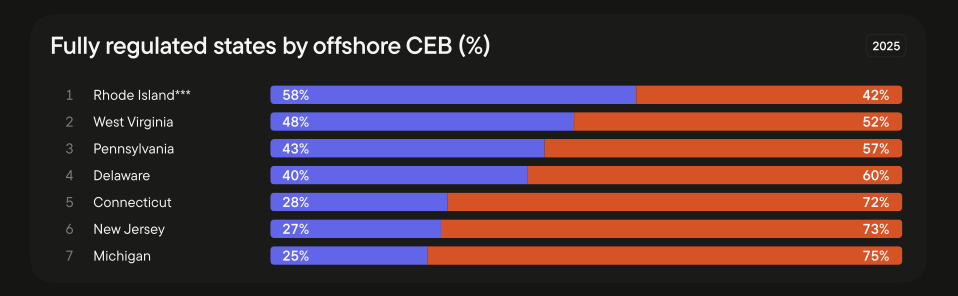

Still, 43% offshore remains a substantial share for a state with seven years of full regulation behind it.

For context, New Jersey — which launched online casino in 2013, six years before Pennsylvania — sits at 27% offshore in 2025. Pennsylvania’s trajectory suggests it may approach New Jersey’s level around 2030 or 2031, assuming continued competitive investment by domestic operators.

Some offshore brands are losing ground faster than others

The market’s composition shows several notable dynamics.

Bovada’s Pennsylvania CEB declined 24.3% in 2025 — a steeper drop than in most other states — reflecting the sustained competitive pressure from a fully developed domestic market. BetOnline also declined 13.8%. The offshore retreat in Pennsylvania is real and appears to be accelerating.

theScore posted the fastest growth in the top 10

theScore, formerly known as ESPN BET before a rebranding in late 2025, posted 157.5% YoY CEB growth in Pennsylvania — the strongest among any top-10 brand in the state.

The growth partly reflects brand confusion from the ESPN BET rebrand, which may have temporarily suppressed search demand before recovering under the new identity, but it also reflects genuine product investment in the Pennsylvania market.

The scale of the state’s gambling market reflects a combination of population, gambling culture, and the specific product mix that full regulation unlocks: Pennsylvania players engage actively with slots, live dealer games, poker, and sports betting, producing a total addressable market that rivals mid-sized European countries.