The vertical that grew 256% in 2025 is now fighting for the right to exist in its fastest-growing states.

Arizona became the first U.S. state to file criminal charges against a prediction market operator when it charged Kalshi with running an illegal gambling business in March 2026 — a move that arrived just weeks after a Nevada court temporarily blocked the company’s sports markets from operating in the state.

Two states. Two legal actions. One week apart. Prediction markets, the breakout vertical of 2025, are now under coordinated regulatory pressure at exactly the moment they were building their most durable momentum.

The question at the center of all of it is definitional: where does a sportsbook end and a financial market begin? The answer, it turns out, depends heavily on who is asking.

Three fronts, one fight

The Arizona charges follow Kalshi’s expansion into sports event contracts — a move the company made in September 2025 following a federal court victory that allowed it to list political contracts. Arizona prosecutors argue the sports markets cross the line into gambling under state law. Kalshi, which is regulated by the Commodity Futures Trading Commission as a Designated Contract Market, maintains it operates under federal oversight and is therefore exempt from state gambling statutes.

That jurisdictional argument — federal preemption versus state authority — is precisely what makes this case consequential beyond Arizona. If courts rule that CFTC-regulated event contracts can be prosecuted under state gambling laws, the entire regulatory foundation that prediction markets built their expansion on becomes unstable.

Nevada’s action, while framed as temporary, adds pressure from a different angle. The state’s gaming regulators did not file criminal charges — they obtained a court order blocking Kalshi’s sports markets while the legal question is resolved.

Nevada, unlike Arizona, has a mature sports betting industry to protect, and regulators there have been explicit that they view prediction market sports products as competing directly with licensed sportsbooks.

Federal discourse has sharpened in parallel. Legislators and regulators have spent the better part of 2026 debating whether event contracts require a separate regulatory framework, and whether the CFTC’s jurisdiction is sufficient or whether state gaming authorities need concurrent oversight powers.

The vertical that built its momentum too fast

What makes the timing significant is how recently prediction markets crossed from niche instrument to mainstream vertical.

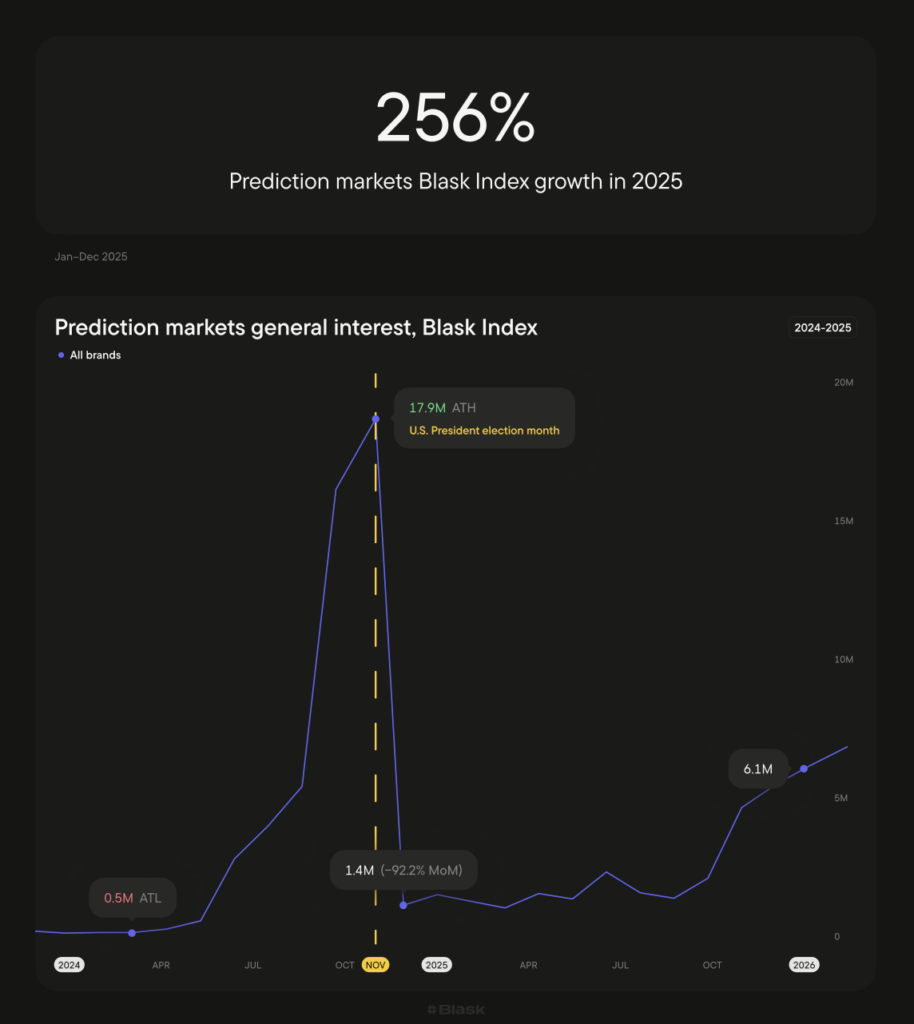

According to Blask data, the prediction markets category posted Blask Index growth of 256% from January to December 2025 — the sharpest annual rise of any tracked vertical in the U.S. market.

The category had peaked even earlier: in November 2024, during the U.S. presidential election, it reached an all-time high Blask Index of 17.9 million. When the election ended, interest collapsed by more than 92% MoM, falling to 1.4 million in December 2024. What happened next was more important than the collapse itself — the category rebuilt. By late 2025, interest had climbed back to 6.1 million and was trending upward, no longer reliant on a four-year political cycle.

That recovery was driven by Kalshi’s entry into sports event markets — which is now the exact product under legal attack in Arizona and Nevada.

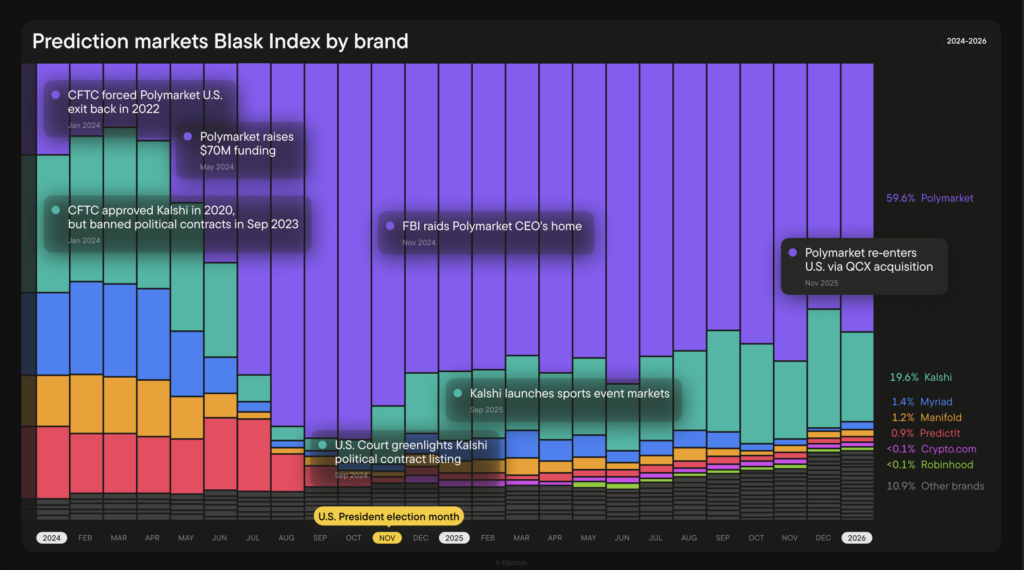

The market has consolidated sharply around two players. Polymarket holds 59.6% of prediction market demand by Blask Index; Kalshi holds 19.6%. Ten new brands entered the category in 2025, but the long tail shrank rather than expanded.

By early 2026, at least 17 platforms were actively operating and roughly 20 more were in various stages of launch — several seeking CFTC approval as Designated Contract Markets. The vertical was attracting capital and regulatory filings simultaneously.

The State-Level Context Blask Data Reveals

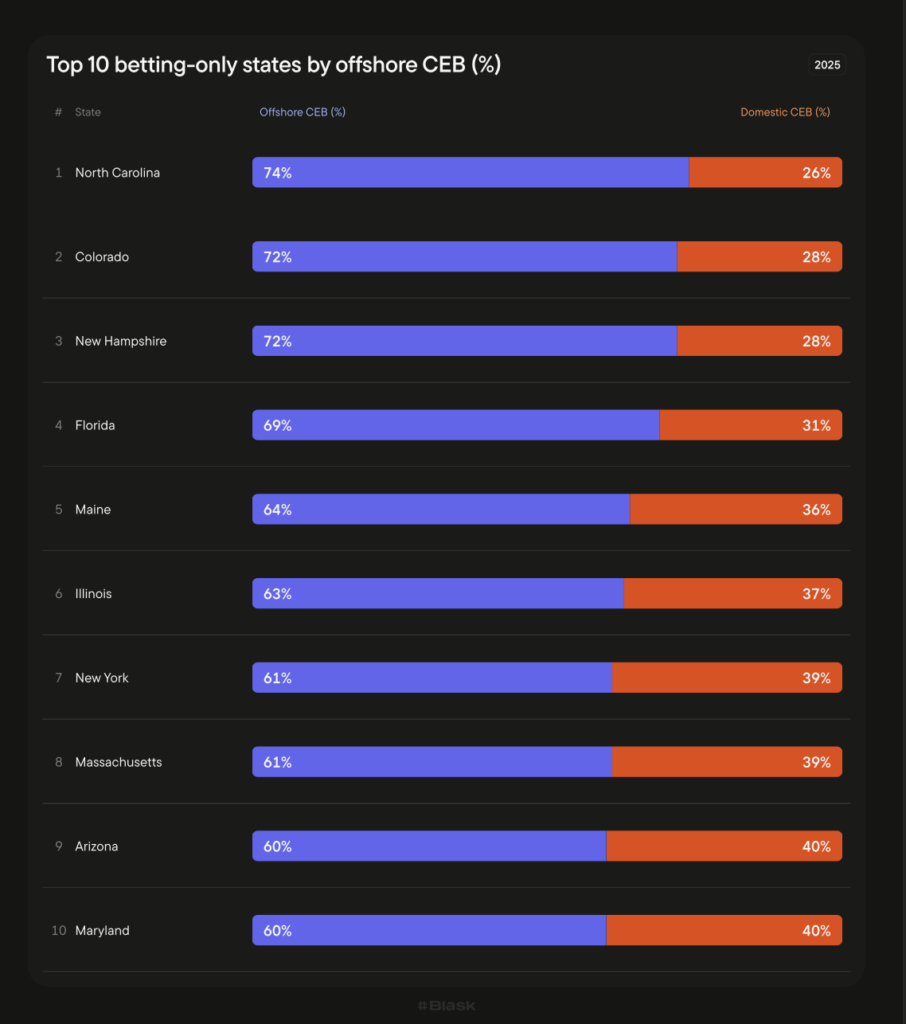

Arizona and Nevada are not random choices in this story. They have legalized sports betting but not online casino gambling and they sit in a specific structural position in the U.S. market that makes prediction markets particularly threatening to their licensed sportsbook operators.

Arizona has 60% offshore CEB — meaning 60 cents of every dollar spent on online gambling in the state flows to unregulated or unlicensed operators. Nevada sits at 76% offshore. In betting-only states as a category, the average offshore share is 74%.

These states have already ceded the majority of gambling revenue to platforms outside their regulatory reach. A new category of event-contract products — federally regulated but operating outside state licensing frameworks — compounds that structural problem. Their sportsbook operators, licensed and taxed, compete against platforms that carry neither obligation.

That is the political economy behind the legal action. The criminal charges in Arizona are not purely about consumer protection. They reflect a licensed industry’s existential interest in maintaining a competitive boundary.

What happens to the duopoly

The immediate question for Polymarket and Kalshi is whether their current operating model survives contact with the state-level legal system.

Kalshi’s CFTC license has been its primary regulatory shield — the argument that federal oversight supersedes state gambling law. That argument has not yet been tested in a criminal prosecution context. If it fails, Kalshi would need to either withdraw from states that challenge it or negotiate state-level licensing frameworks that do not yet exist for this product category.

Polymarket’s position is structurally different. The company was forced out of the U.S. market by the CFTC in 2022, re-entered through an acquisition in November 2025, and currently holds the largest share of prediction market demand at 59.6% of category Blask Index.

Its re-entry is recent enough that it has not yet accumulated the regulatory track record that Kalshi has — which cuts both ways.

While prediction markets are currently being stress-tested in sports, their underlying mechanism — pricing probability in real time — extends far beyond it. Sport may be the entry point, but the broader opportunity lies anywhere uncertainty exists.

Will Martin CEO of VANT

Whether courts agree that pricing probability constitutes a financial instrument rather than a wager will determine how that opportunity unfolds.

A structural test, not a temporary setback

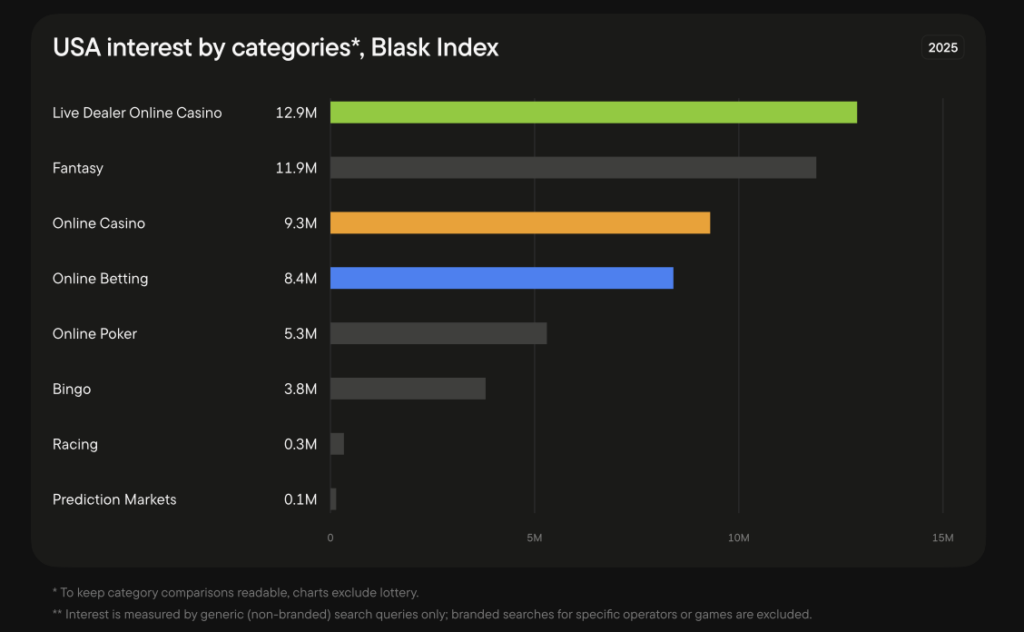

The iGaming industry has watched prediction markets grow from a curiosity — a category with 0.1 million in generic search interest across the entire U.S. market in 2025, compared to 8.4 million for Online Betting and 9.3 million for Online Casino — into the vertical with the steepest growth trajectory of any tracked category.

The regulatory pressure now arriving is proportional to that growth. States do not file criminal charges against platforms that have negligible market impact. Arizona and Nevada are acting precisely because Kalshi’s sports markets have become visible enough, and threatening enough, to demand a response.

“There is a lot of litigation ongoing and it will take time for the dust to settle — so there is a clear opportunity for the regulated space to begin to adopt some of these innovations.”

Evan Fisher COO of Sparket

The category has proven that durable demand exists beyond electoral cycles. The legal system is now determining whether the current operators get to capture it.