UK and Spain both broke gambling revenue records in 2025. Harm demand and offshore migration are accelerating at the same time.

Two of Europe’s most regulated gambling markets had a strong 2025 by almost every measure operators and regulators care to publish. Then there are the measures that get less attention.

Blask tracks demand across 335 active brands in the UK and 112 in Spain. The data confirms the headline numbers. It also shows what sits underneath them.

The headline numbers are real

The UK gambling market generated an estimated $11.5B in Competitive Earning Baseline (CEB) across all regulated brands in 2025, with an Acquisition Power Score (APS) of nearly 20 million new customers per year ($8.4B–$20.9B CEB range; 14.7M–35.3M APS range).

CEB is Blask’s market-based revenue benchmark, built from brand demand signals and competitive positioning rather than operator-reported figures. APS measures how many new customers a market’s brands collectively acquire, based on external search and behavioral signals. Both are ranges because competitive conditions, seasonal swings, and campaign timing all shift outcomes.

In Spain, Blask’s total CEB for 2025 reached €1.76B — almost exactly matching the record €1.7B GGR that DGOJ reported in March 2026, a 17% year-on-year increase.

Both markets are large, maturing, and producing record numbers. Neither looks like a regulatory failure on revenue metrics.

What the UK market grew alongside its revenue

The UK regulated market grew roughly 3.6% in acquisition terms in 2025. Over the same period, demand for gambling harm support grew +112% year-on-year, according to Blask data tracking GamCare-related demand signals. Harm outpaced market growth by a factor of 31.

The GamCare National Gambling Helpline recorded 130,000+ calls and online contacts in the April 2024–March 2025 reporting year — a record. GamCare and PayPlan jointly reported in March 2026 that gambling-related debt cases hit their highest levels on record.

This is not a story about a market that failed to develop responsible gambling infrastructure. The UK has the world’s deepest regulatory stack: deposit triggers, financial vulnerability data sharing (mandatory since February 2025), and online slot stake limits of £5 per spin (£2 for under-25s) that came into force on April 9, 2025. The UKGC moved from disclosure-based tools to format interventions, which is the logical conclusion when information-first approaches hit their ceiling.

And yet harm demand is growing faster than the market itself.

Affordability checks: what the UKGC data shows

Affordability checks have been the most contentious piece of UKGC’s reform agenda. The Commission confirmed in March 2026 they will not launch in May as originally planned. Trade bodies pushed back hard. Racing Post reported in March 2026 that major operators are distancing themselves from horseracing specifically because of the compliance friction.

The framing of the debate matters. The checks have two tiers: automated frictionless screening at lower thresholds, and enhanced checks requiring bank statements at higher thresholds. Wealth documentation determines which tier a player lands in. The UKGC’s own pilot reported a 95% frictionless rate — the system worked smoothly for most players.

What UKGC’s separate dataset revealed is harder to dismiss. Between June and September 2024, operators restricted 4.31% of accounts, mostly through maximum stake limits. Accounts closed for commercial reasons represented another 2.23%. The Commission’s own analysis found that restricted accounts were more profitable than unrestricted ones — operators were limiting winners, not managing risk.

The checks critics argue that in regulated GB, a heavily addicted player is increasingly a liability: source-of-funds investigations, forced voids, refund exposure, regulatory sanctions. The frictionless system helped operators shed those accounts cleanly. Recreational players got flagged at low thresholds. High-stakes players with income documentation sailed through.

The discrimination argument runs the opposite direction to how it’s usually framed.

Spain: 14 years of regulation, still 23% offshore

Spain moved faster than most. DGOJ launched the online licensing framework in 2011, among the first in Europe. The regulated market has grown every year since, reaching record €1.76B CEB in 2025 by Blask’s measure.

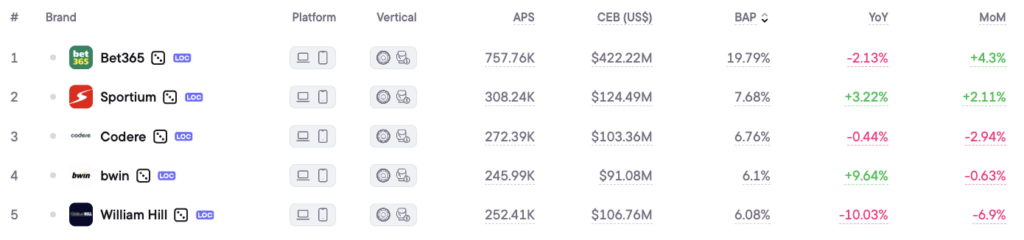

Bet365 holds the #1 position in Spain by APS (749K new customers per year, average), but the brand’s demand fell –8.25% year-on-year — the dominant operator losing share in a growing market. Luckia, a domestic operator ranked #6, grew +34.57% over the same period. The competitive structure is shifting.

What isn’t shifting is offshore leakage. A November 2025 study by Augusta Abogados estimated 23.4% of Spanish online players access unregulated operators. Gambling Insider reported in March 2026 that share is still rising into 2026.

DGOJ’s own figures tell the same story at a tighter methodology. The regulator tracks offshore through card and electronic payment flows — no survey bias, no GGR estimation.

That measure put offshore at 3.5% of total deposits three years ago. By 2025, it reached 6.2%. At the same rate, Spain crosses 11% by 2029, which is precisely the window covered by the Safe Gambling Programme 2026–2030 the DGOJ launched in March 2026.

Three methodologies, one label

The Spanish case surfaces a measurement problem that applies across every regulated market.

Three different approaches produce three different offshore estimates:

- 6.5% (DGOJ’s GGR-share estimate)

- 6.2% (payment deposit tracking)

- 23.4% (player self-report).

All three call the same thing “offshore.” All three are defensible. None of them is wrong.

The 23.4% figure measures how many players accessed unregulated operators at any point during the period — a behavioral signal. The 6.2% deposit figure measures actual capital flows to offshore operators — a financial signal. The 6.5% GGR estimate compares offshore revenue to licensed market revenue — a competitive sizing signal.

fair – deposit tracking is actually your strictest measure

— Max Tesla (@allsetmax) March 27, 2026

no survey bias, no GGR estimation, card movements only

3.5% -> 6.2% on the tightest methodology you have, three years…

at that rate ~11% by 2029

Spain's safe gambling programme 2026-2030 launched last week

Each methodology answers a different regulatory question. The one a regulator chooses to publish says something about which question they’ve decided to prioritize.

What Blask data adds to the picture

Blask tracks demand for harm-adjacent services as part of its behavioral demand signals. In the UK, that means tracking search activity around GamCare, GambleAware, debt counseling services, and related terms alongside operator demand.

The 112% growth in harm-related demand, against 3.6% market growth, doesn’t mean the UK regulated market is producing more problem gamblers per player. The market has also gotten better at surfacing those players through mandatory interaction data and affordability tooling introduced since 2023 — some of the growth in helpline contacts reflects improved identification, not a worsening baseline.

But the gap is large enough that both explanations coexist: better identification AND worsening exposure. The data can’t distinguish between them. What it can do is make the gap visible in real time, before it shows up in annual survey results.

In Spain, Blask’s 112 active brands in a market producing €1.76B CEB suggests a competitive density that creates pressure to acquire users through channels outside the licensed funnel. Spain’s advertising restrictions and 2020 bonus ban cut new regulated account openings by more than half — the 3.5% to 6.2% offshore deposit trend is one consequence of that pressure finding an exit.

The intervention logic

The UKGC’s move from disclosure to format intervention marks a shift in how the regulator understands the problem. Disclosure assumes rational agency is intact. Format intervention assumes it isn’t.

The research base for that shift is strong. Gambling event frequency is one of the strongest predictors of harm, operating independently of whether the player knows the odds. A player can know the house edge and still get conditioned by the spin rate. The UKGC spent 20 years building disclosure-first tools. The 130,000+ GamCare contacts in 2024–25 are a performance review of that approach.

Format restrictions change the product architecture, which is where the behavioral conditioning loop actually lives. The UKGC’s own assessment of game design confirmed that session length is a primary driver of harm exposure. Near-miss frequency increases play duration and spend independently of win expectation. The UKGC’s online slots stake limit guidance is the product of that evidence base — a format restriction, not a disclosure requirement.

Spain’s Safe Gambling Programme 2026–2030 targets youth protection, AI-based risk tools, and operator collaboration frameworks. Whether it addresses product architecture directly will determine whether the offshore trend line bends by 2029, or keeps compounding.

Conclusion

Revenue records are lagging indicators. They measure what happened after players made decisions inside a product environment. Harm demand signals and offshore migration rates are leading indicators. They measure what’s driving those decisions, and where some of those players are going instead.

The UK and Spain both have records on both sides of the ledger. The regulated market is growing. So is the evidence that its core consumer protection mandate is under pressure.

Blask Index data makes both sides of that ledger visible in real time, across 335 brands in the UK and 112 in Spain, before it consolidates into annual filings. For operators and regulators who want to track the gap between revenue performance and harm signals, that’s the data layer that matters.