- Updated:

- Published:

The regulatory firewall: How Polymarket navigates the CFTC to capture the US market

Prediction markets growth and CFTC regulation

The explosive rise of prediction markets has fundamentally altered how people engage with uncertainty. What began as a niche corner of the internet has rapidly transformed into a mainstream financial phenomenon. Yet, as this sector grows, it is triggering a complex regulatory showdown. At the center of this battle sits Polymarket.

The platform is currently testing the absolute limits of federal oversight.

Observers and industry insiders are actively questioning the current framework. Jessica Welman, a prominent industry voice, recently posed a critical question. If the Commodity Futures Trading Commission (CFTC) views the offshore version of Polymarket as a bad actor, why can the platform still offer regulated event contracts in the United States?

The answer lies in a sophisticated corporate restructuring. It reveals a fascinating loophole in how federal agencies regulate emerging financial platforms compared to traditional gambling operators.

The “unsuitable affiliate” dilemma

To understand Polymarket’s current US strategy, one must look at traditional casino regulation. In established gaming jurisdictions like Nevada, regulators heavily enforce the concept of “unsuitable affiliates.”

Under Nevada Gaming Regulation 3.080, a company cannot simply spin off a new entity to secure a license if its parent company or offshore affiliate operates illegally. The taint of the offshore entity infects the domestic application.

However, the CFTC does not regulate casinos. They regulate derivatives and commodities.

In November 2025, Polymarket officially returned to the US market. They achieved this not by seeking forgiveness, but by acquiring QCX LLC and QC Clearing LLC. This strategic acquisition allowed them to create Polymarket US. This new entity is structurally and legally separate from the global offshore platform. It operates as a CFTC-registered Designated Contract Market (DCM) under a strict “intermediated” model. US users must trade through regulated Futures Commission Merchants (FCMs) and undergo full Know Your Customer (KYC) compliance.

Through this legal firewall, Polymarket successfully separated the “offshore bad actor” from the “US licensed exchange.” They effectively bypassed the suitability concerns that would instantly disqualify them in a traditional gaming jurisdiction.

The market reality: A consolidating duopoly

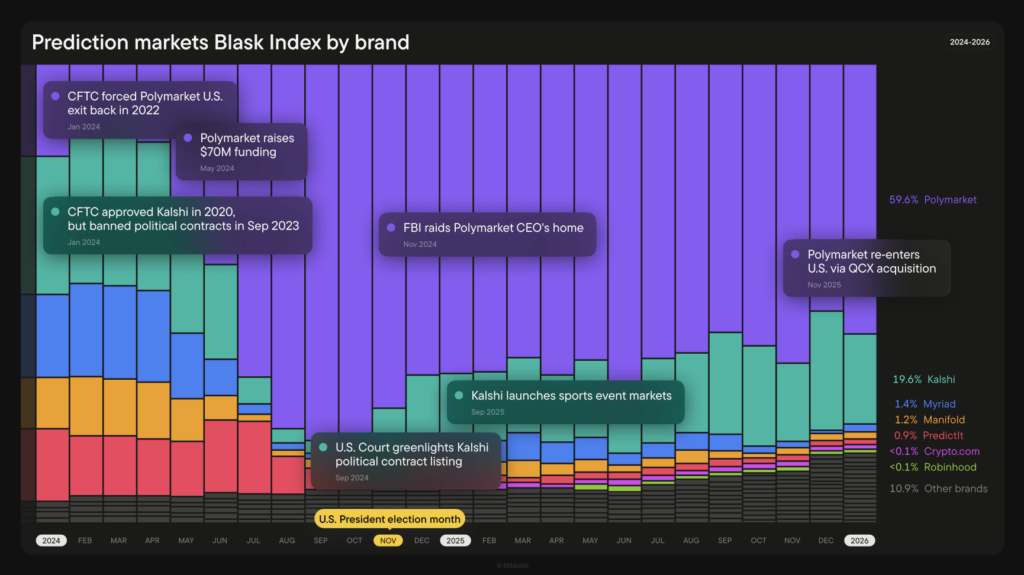

The urgency for Polymarket to secure a US foothold is entirely justified by the underlying data. According to Blask’s analytical report, “USA and Canada iGaming landscape 2025”, prediction markets became the absolute breakout vertical of the year.

After peaking during the 2024 US presidential election cycle, the category did not fade into obscurity. Instead, the vertical saw a staggering 256% growth in the Blask Index from January to December 2025. This massive surge was largely catalyzed by platforms expanding beyond political events into sports prediction markets.

The competitive landscape is rapidly consolidating.

Despite 10 new brands entering the space in 2025, the market is essentially a fierce duopoly between Polymarket and its CFTC-regulated rival, Kalshi. Polymarket maintained a dominant 59.6% share of the category’s Brand’s Accumulated Power (BAP) throughout the year. Kalshi followed with a highly respectable 19.6%.

This intense concentration of market attention leaves very little room for smaller competitors. The long tail of the market is visibly shrinking. For Polymarket, capturing the massive Competitive Earning Baseline (CEB) potential within the US required a bold legal maneuver. The QCX acquisition provided exactly that.

The CFTC opens the rulebook

The regulatory friction surrounding prediction markets is reaching a critical boiling point. The CFTC is keenly aware of the structural workarounds platforms are utilizing.

On March 12, 2026, the agency finally issued Staff Advisory Letter No. 26-08. This document represents the agency’s first dedicated guidance specifically targeting prediction market listing standards.

Simultaneously, the CFTC issued an Advance Notice of Proposed Rulemaking (ANPRM). This opened a 45-day public comment window to figure out how to properly regulate this booming sector. The CFTC insists that it retains primary enforcement jurisdiction over event contracts under the Commodity Exchange Act (CEA). This stance has already sparked legal battles. For example, Kalshi recently fought off attempts by Ohio gaming regulators to apply state gaming laws to federal event contracts.

The foundational question remains unanswered. Will the CFTC ultimately adopt a regulatory stance similar to state casino boards? Will they eventually penalize US entities for the behavior of their offshore affiliates?

Conclusion: A precarious legal strategy

Polymarket’s approach is undeniably brilliant from a corporate structuring perspective. By acquiring existing, clean entities to act as their domestic shield, they secured access to the world’s most lucrative market. They successfully capitalized on the 256% growth wave sweeping through the industry.

However, this strategy rests on a precarious foundation. The rules governing prediction markets are literally being written right now. The CFTC’s recent advisory letter indicates that the era of regulatory ambiguity is rapidly closing.

For now, the legal firewall holds. Polymarket US and offshore Polymarket remain two different legal persons. Yet, as the lines between financial trading and event wagering continue to blur, federal regulators may soon realize that a firewall is useless if the same brand commands the attention on both sides of the divide. The coming months will determine whether this innovative legal strategy becomes the industry standard or a cautionary tale.