Hungary is preparing to review its gambling regulation after a long period of state dominance. At the centre of attention is Szerencsejáték Zrt., the key state operator for lotteries and betting.

The government of Péter Magyar is preparing a review of Hungary’s gambling model. The first focus is the state operator Szerencsejáték Zrt., which controls the lottery market and holds a central position in land-based betting.

András Kármán has also initiated a review of state-owned companies, including Szerencsejáték. This adds the issue of financial transparency to the gambling reform: the question is not only about licences, but also about how the revenues of the state gambling operator were managed and whether the current model provides enough accountability.

Since 1 January 2023, operators have formally been allowed to apply for online sports betting licences, but the market has remained narrow. According to ICLG, online casino games can still only be offered by holders of land-based casino concessions, while the online sports betting regime continues to raise questions over its compatibility with EU law and national law.

TippmixPro anchors a highly concentrated market

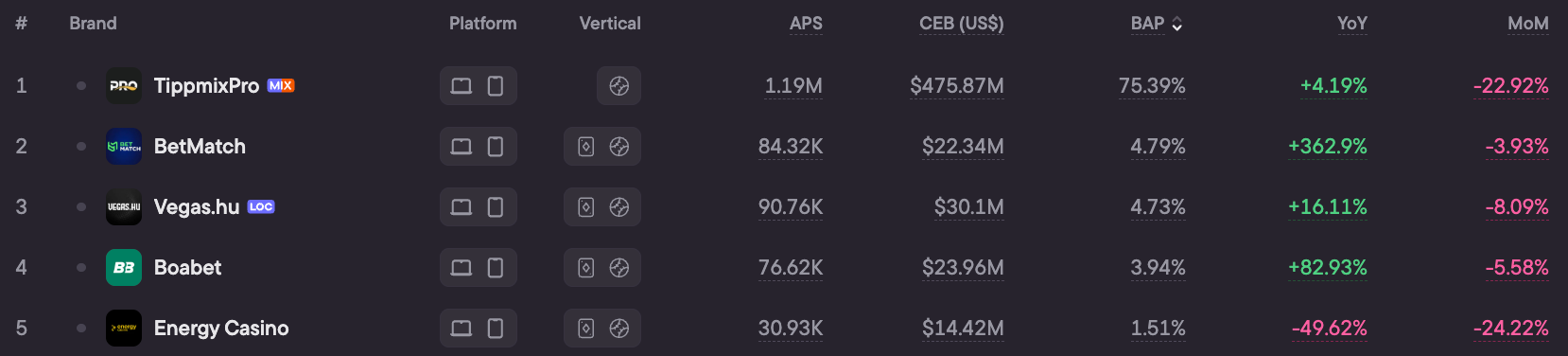

According to Blask data Hungary’s iGaming market remains highly concentrated around TippmixPro, which is linked to the state operator Szerencsejáték Zrt. The brand ranks first in the country by BAP — 75.39%. The state-linked brand still carries the main share of the market’s measured value, while the gap with the closest challenger brands remains wide.

BetMatch, the second-ranked brand, shows the fastest Blask Index growth in the upper part of the table at +362.9% YoY, but its CEB is only $22.3M, or around 4% of TippmixPro’s CEB.

Over the past 12 months, TippmixPro remained the clear leader in Hungary, holding more than three quarters of total BAP and the largest CEB in the market. The nearest challengers — BetMatch, Vegas.hu and Boabet — each stayed below 5% BAP, even as BetMatch posted the strongest Blask Index growth in the upper part of the ranking, up 362.9% YoY. The table below shows the scale of the gap: challenger brands are gaining visibility, but none has yet changed the market’s centre of gravity.

Therefore, the first limitation for any Hungary gambling reform is that the market cannot be treated as an empty field for new licences. Hungary inherits a state-centred leader, a small group of fast-growing challenger brands and a demand hierarchy in which tax and licensing changes will directly affect the largest source of measured value.

Offshore demand exposes the limits of Hungary’s closed model

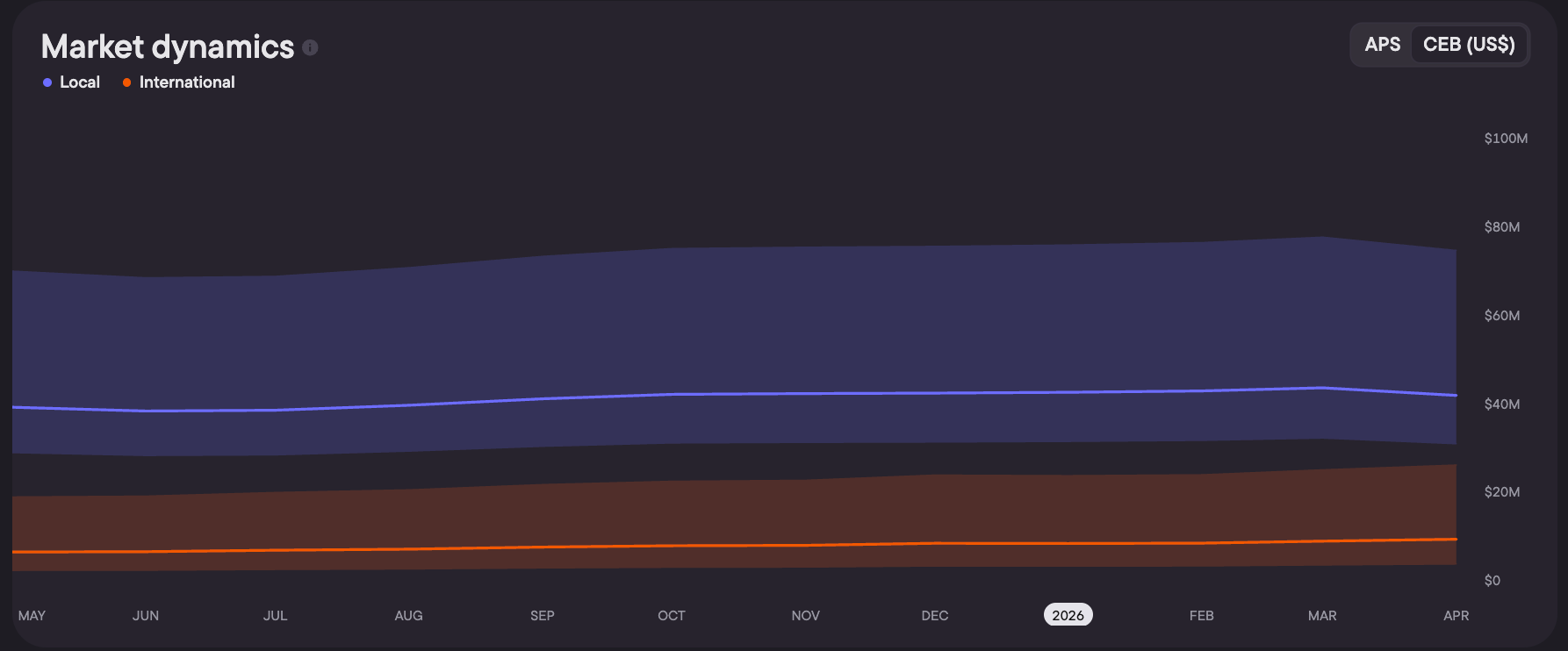

The second limitation for the future reform is the growth of offshore demand. Blask license split data shows that the licensed side of Hungary still controls most of the observed demand, but the direction is changing. In January 2025, offshore brands held 15% of Hungary’s Blask Index by BAP share. By April 2026, their share had increased to 23.6%.

The onshore segment still holds the majority of demand and measured market value. But the warning lies elsewhere: offshore brands are growing faster inside a closed model. The regulator can restrict entry, payment accounts and domains, but if users continue to search for offshore brands, part of the demand still remains outside the licensed channel.

Therefore, the potential reform will be assessed not only by the new licensing rules. The key question is whether Hungary can slow the growth of the offshore segment and move part of that demand into the regulated environment.

Channelization becomes the key test for Hungary

Hungary is not starting its reform from zero. The market already has a state-linked leader that holds the main share of measured CEB, a small group of challenger brands and an offshore segment that is gradually gaining share.

Therefore, the next law will be a test of channelization. If the review is limited to the governance of Szerencsejáték, the market is likely to remain concentrated, while offshore demand will continue to grow around the licensed system. If the new framework gives operators clear and workable access to the market, Hungary could become one of the key regulatory resets in Central European iGaming.

The main test of the reform is whether Hungary can combine clear licensing, protection of state revenues and lower offshore demand. Without this, channelization will remain the market’s weak point.