Skip to main content

Blog

Knowledge base

Changelog

Quick search...

⌘K

/

Blog

Knowledge base

Changelog

Blask Blog

Featured

Inside Blask’s lobby-position engine: pinpointing every game, every day

June 19, 2025

Leading the Shift: Ushering in APS & CEB for a New Era of Brand Performance

January 19, 2025

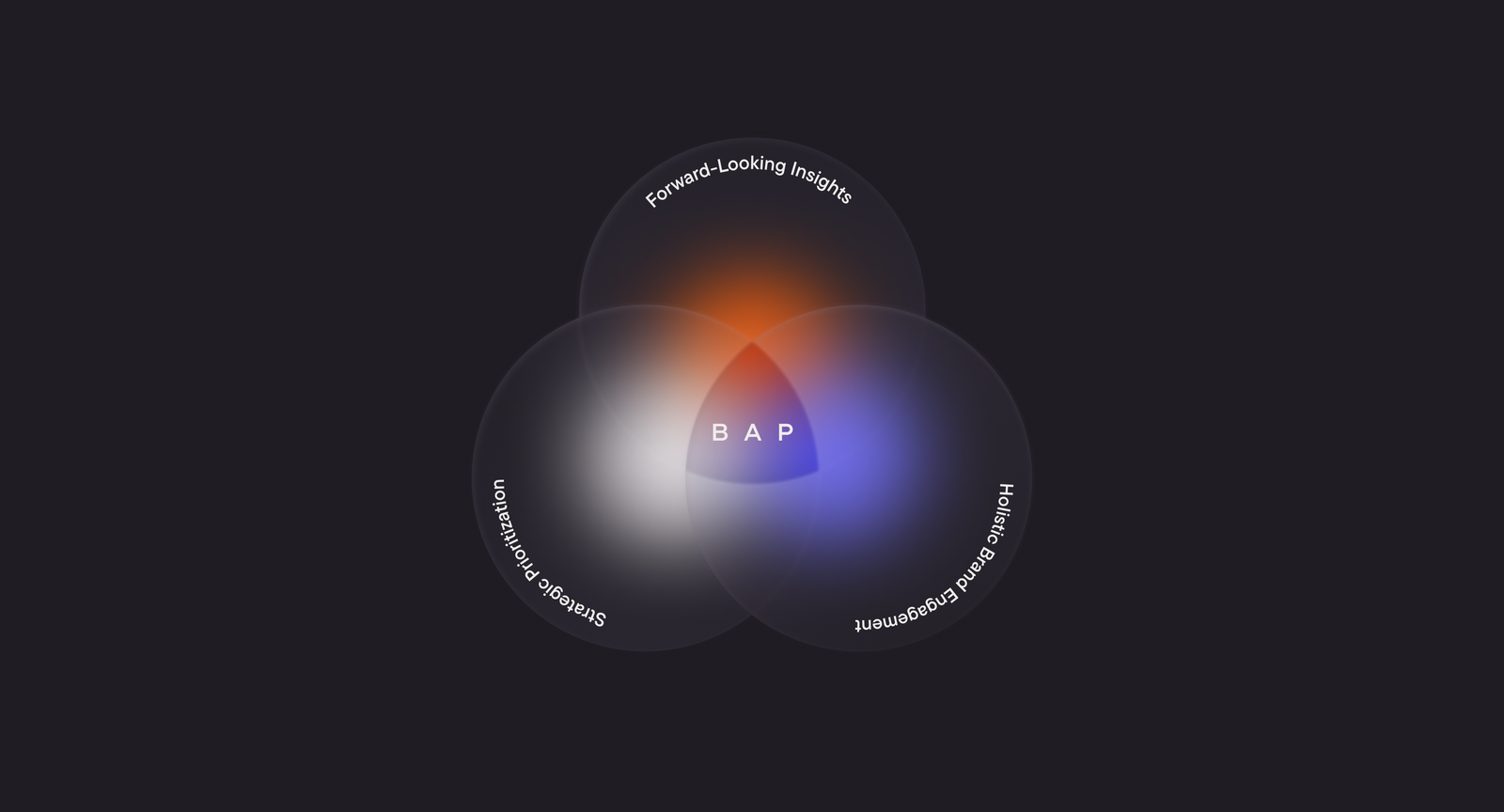

BAP is All You Need: Transitioning from Market Share to Brand’s Accumulated Power

January 19, 2025

What is Blask and how to use it to navigate through iGaming industry

August 30, 2024

Latest

Quick tour: the Game view in Blask Games

June 22, 2025

Quick tour: the “Countries” view in Blask Games

June 22, 2025

—

blog

30+ ways Blask Games empowers iGaming professionals

June 19, 2025

How does Blask calculate player interest for every casino game?

June 19, 2025

Inside Blask’s lobby-position engine: pinpointing every game, every day

June 19, 2025

Blask expands coverage to 57 countries and 2519 brands

May 16, 2025

How do iGaming affiliates use Blask?

May 15, 2025

Driving affiliate network growth with Blask analytics — the Makeberry journey

April 30, 2025

How do iGaming operators use Blask?

April 22, 2025

What's new in Blask? March 2025

April 02, 2025

How Blask filters mirror sites when searching for iGaming brands

March 26, 2025

Blask nominated for the Asia Gaming Awards 2025!

March 17, 2025

Blask shortlisted for GamingTECH Awards 2025

March 12, 2025

What's new in Blask? February 2025

March 07, 2025

Blask shortlisted for SPiCE South Asia 2025 Award in Innovation of the Year category

March 02, 2025

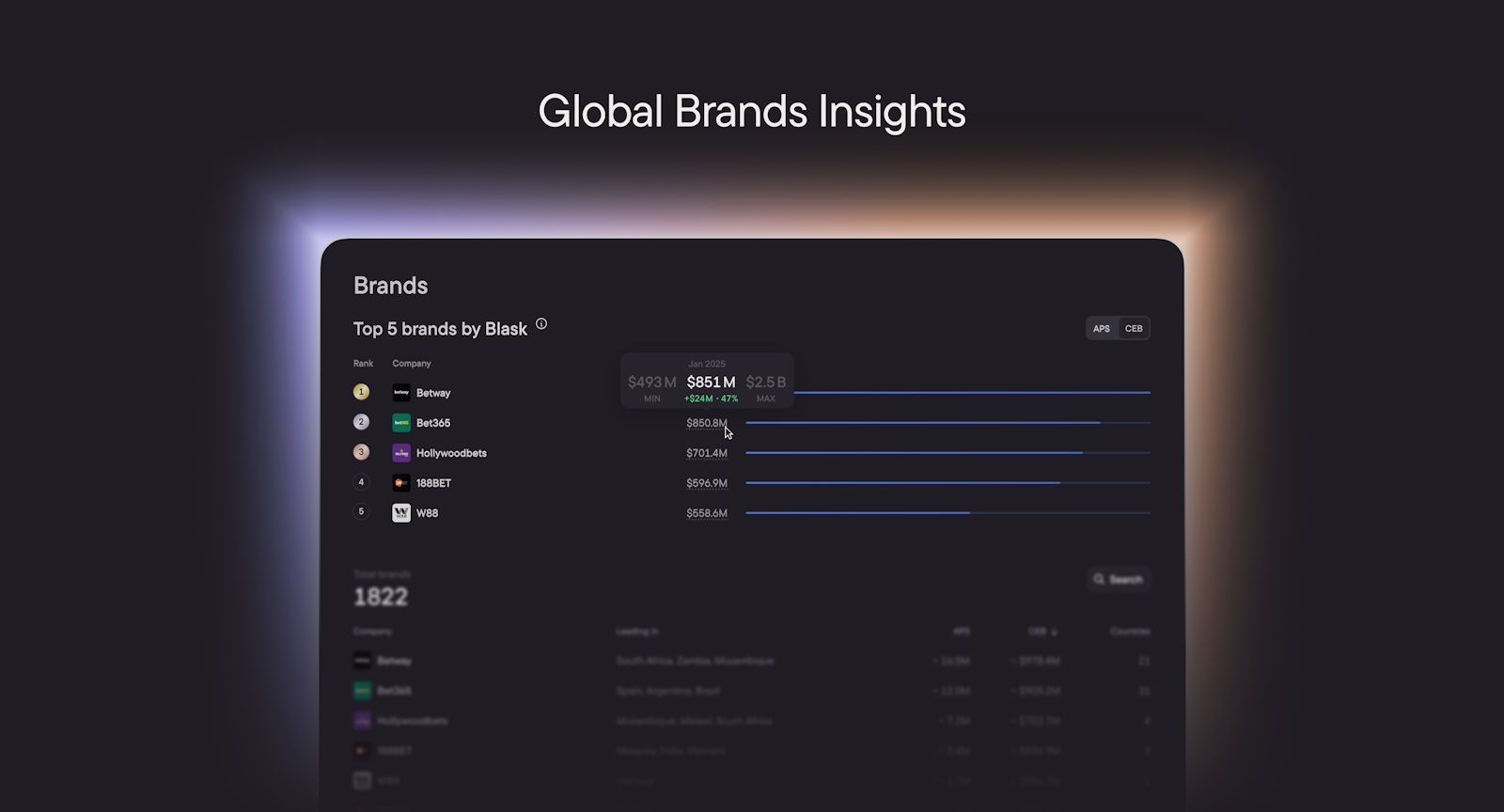

Top 10 iGaming Brands in the world — January 2025

February 24, 2025

Get the most out of the Global Brands page

February 20, 2025

Blask introduces the Brands page featuring a table of all global iGaming brands

February 19, 2025

Blask’s “All Brands” dashboard helps betPawa brand achieve record APS in Africa

February 18, 2025

Blask iGaming digest on Brazil — January 2025

February 10, 2025

What's new in Blask? January 2025

February 03, 2025

Blask introduces local and international brand segmentation for regulated markets

February 01, 2025

Blask's path to a novel metrics breakdown framework for local and international iGaming brands

January 23, 2025

Leading the Shift: Ushering in APS & CEB for a New Era of Brand Performance

January 19, 2025

BAP is All You Need: Transitioning from Market Share to Brand’s Accumulated Power

January 19, 2025

Premier Bet uses Blask to elevate brand health tracking in Sub-Saharan Africa

January 13, 2025

How Latin American players approach iGaming differently

January 08, 2025

The defining events that shaped iGaming in 2024

December 30, 2024

Blask unveils the fastest-growing iGaming markets of 2024

December 26, 2024

How to explore iGaming market dynamics and brand insights with the Blask’s Market Overview page

December 18, 2024

Load more