- Updated:

- Published:

Canada’s iGaming market: mostly offshore

Provinces transitioning to an open market are set to solve a channelisation problem that monopoly regulation never did.

Alberta is getting ready to become the second of Canada’s ten provinces to open its iGaming market to private operators, following Ontario, which did so four years ago. Many brands already operating in Ontario have expressed interest in entering Alberta’s market.

Blask’s new report on the US and Canadian markets shows what they are competing for — Canada is the world’s third-largest iGaming market by CEB, and Ontario demonstrated that open competition pulls demand from offshore into licensed channels. Across the rest of the country, offshore operators still dominate.

This article draws on findings from Blask’s comprehensive report covering the US and Canadian iGaming markets — state-by-state and province-by-province breakdowns, offshore vs. domestic dynamics, brand rankings, and expert commentary.

The third-largest iGaming market in the world

Gambling regulation in Canada is provincial — each province sets its own rules. Most run a single government-backed platform as the only licensed online option. Offshore operators take the rest.

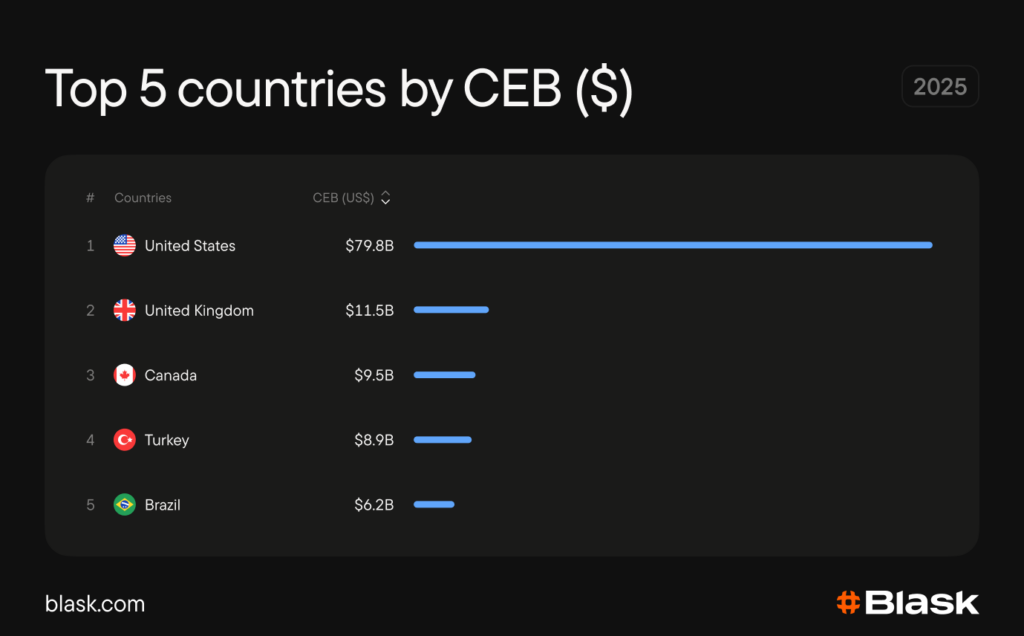

Canada’s total online gambling market reached approximately $9.5B in CEB in 2025, placing it third globally behind only the US and the UK, with the fastest year-on-year growth among the global top five.

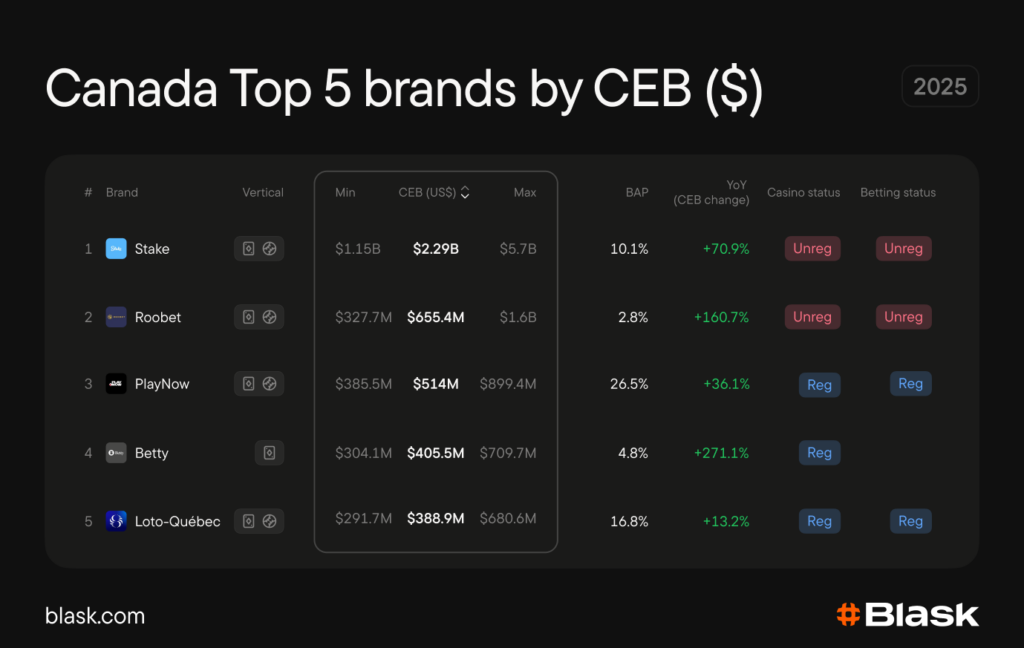

Offshore operators account for the majority of that volume — and the gap is widening. In 2025, offshore CEB grew 40%, against 23% for domestic brands. 230 brands compete for Canadian players. The top two by CEB are Stake and Roobet, both unregulated.

Regulation without competition

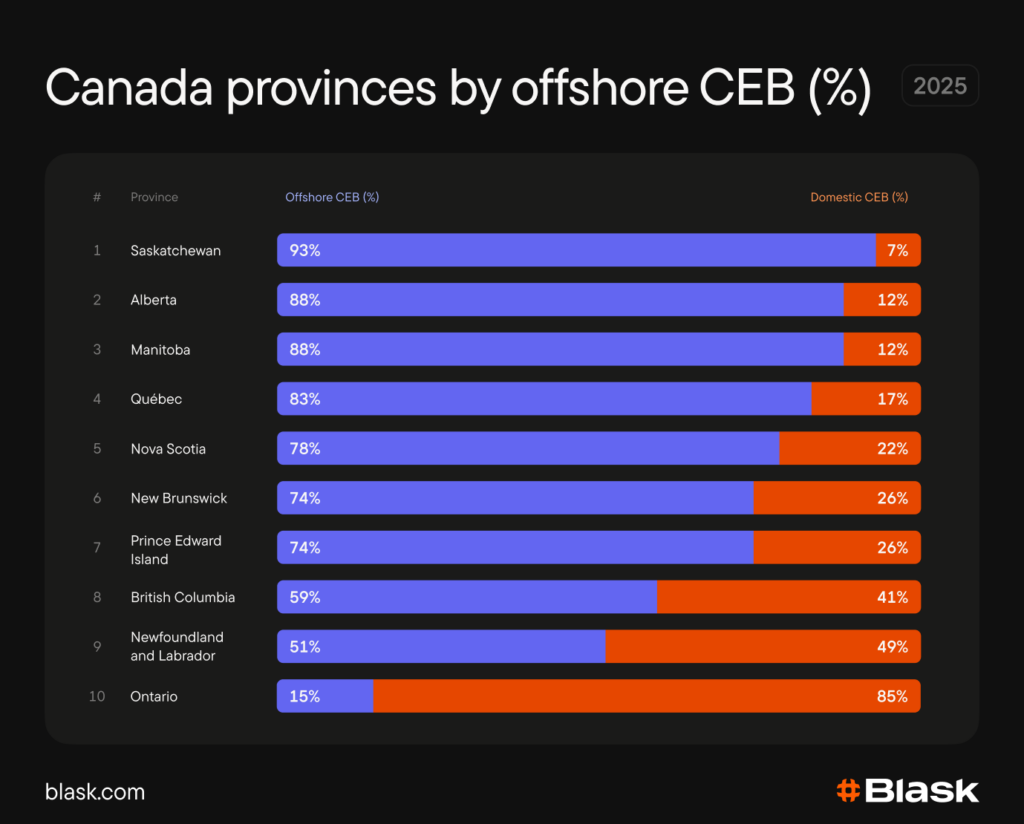

The offshore dominance is not a new problem and not one that regulation alone has solved. Québec has run its own licensed online casino — Espace-jeux, operated by Loto-Québec — since 2010. After all these years, offshore operators still capture 83% of the province’s iGaming market.

British Columbia has had its regulated platform, PlayNow, since 2004. Offshore brands still take the majority there too, at 59%.

The provincial data from Blask’s report shows that not a single province, except Ontario, has achieved any significant level of channelisation. Across monopoly provinces, licensed operators captured only around a quarter of the market on average in 2025.

Ontario’s example

In April 2022, Ontario became the first Canadian province to open its online gambling market to private operators. Licensed brands now capture approximately 85% of provincial demand — the highest regulated share in Canada.

The market opening was unusual — operators already serving players in the grey market were allowed to apply for licences through AGCO (Alcohol and Gaming Commission of Ontario), making the transition smoother. Existing player bases migrated to regulated platforms with minimal disruption.

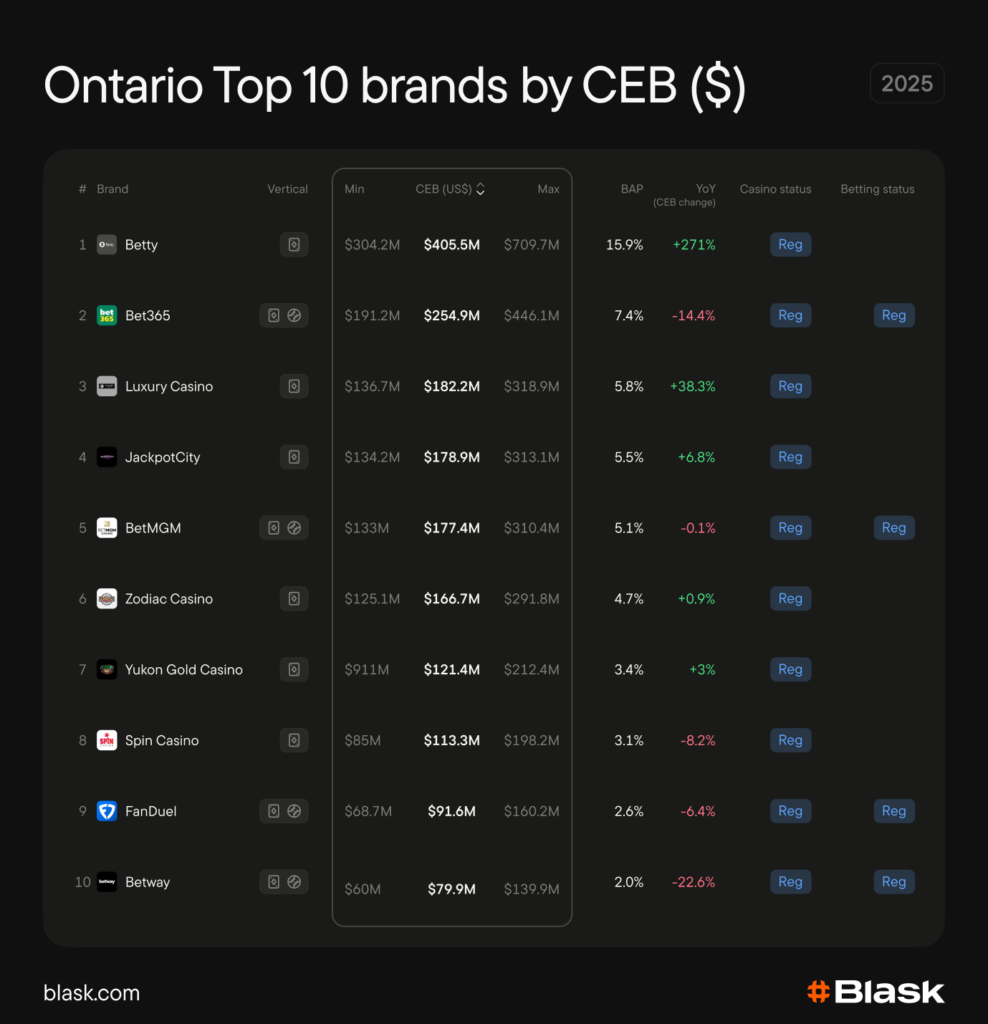

Ontario’s CEB in 2025 was $3.1B. Treated as a standalone country, it would rank 12th by CEB, between Japan and Germany. All top ten Ontario brands by CEB in 2025 were licensed, casino-only operators dominated the top of the table.

The number one of them is Betty – a brand initially built specifically for an audience that most iGaming operators had ignored: female casual slot players. Betty launched in Ontario in February 2023 with a slots-only, community-driven product deliberately designed around mobile gaming mechanics. By 2025 its player base had shifted to roughly 50/50 male-female and it posted 271% year-over-year CEB growth — the fastest in Ontario’s top ten. Betty, among other Ontario operators, has announced plans to enter Alberta when the market opens.

Alberta is next

According to Blask, Alberta’s monopoly operator, PlayAlberta, held only around 12% of the province’s CEB in 2025. Bill 48, passed in May 2025, created the legislative basis for an Ontario-style competitive model.

Although no launch date has been confirmed, registration for operators opened in January 2026, and brands are moving to secure customers before the market goes live.

Ontario showed that open competition can shift the onshore-offshore balance decisively. Alberta, with a market at approximately $1.8B by CEB in 2025, will be the second province to operate on a competitive licensing mode.

Bottom line

Canada is one of the world’s largest iGaming markets, but most of its volume goes to offshore operators despite years of provincial regulation. Ontario opened its market to private operators and channelisation followed. Alberta is set to be the next proof of concept.