The operator holds naming rights to AFCON 2025, a CAF partnership stretching back to 2019, and active registrations in 57 African markets. By actual player demand, it generates less Blask Index than a single-market operator in Mali.

When Senegal lifted the AFCON trophy in Rabat in February 2026, 1xBet’s branding was everywhere — on the perimeter boards, in the broadcast package, in the post-match press conference backdrop. The operator has been an official partner of the Confederation of African Football since 2019, supporting more than 35 tournaments across the continent in that time. The 2025 edition, held in Morocco, was the most commercially successful in CAF history: revenues up over 90%, sponsorship count rising from nine partners in 2021 to 23 in 2025, with CAF attributing the surge in part to 1xBet’s continued involvement.

By the standard metrics of brand investment in African football, 1xBet is the continent’s most committed betting operator.

By the metric that measures what players actually do, it ranked tenth in Q4 2025 — behind a brand that operates in a single country.

The Numbers Behind the Ranking

The figure comes from a cross-continental operator ranking published by Blask in partnership with Find More Africa, which ranked the continent’s 20 largest gambling brands by total Blask Index across Q4 2025 (October through December). The Blask Index measures the volume of market interest attributed to a brand across geographies — built from behavioral signals, normalized across time, and independent of operator-reported revenue.

1xBet’s Q4 Blask Index across all 57 African markets was 18,976,210 — a +14.44% gain quarter-over-quarter, and a number that would represent healthy absolute performance in most regional contexts.

The problem is context.

betPawa, operating in 27 markets, generated a Blask Index of 260,681,877 in the same period. Betway, present in 43 markets, posted 234,141,288. bet223 — a single-market operator in Mali — generated 19,190,884. By that measure, bet223 outperforms 1xBet across 57 countries with the activity of a single market.

The ratio between betPawa and 1xBet is not marginal. It is approximately 13.7 to one.

The Top 20 African gambling operators: a list of the largest cross-African brands, ranked by their total Blask Index for Q4 2025 (October–December).

| № | Brand name | Number of countries | Blask Index in Q4 | Blask Index in Q3 | QoQ |

| 1 | betPawa | 27 | 260 681 877 | 205 730 752 | 26,71 % |

| 2 | Betway | 43 | 234 141 288 | 178 281 178 | 31,33 % |

| 3 | SportyBet | 19 | 73 597 588 | 56 977 401 | 29,16 % |

| 4 | Hollywoodbets | 7 | 64 767 735 | 59 027 276 | 9,72 % |

| 5 | Betika | 17 | 46 581 118 | 40 176 010 | 15,94 % |

| 6 | Bet9ja | 3 | 41 523 822 | 37 014 255 | 12,18 % |

| 7 | Premier Bet | 27 | 34 652 958 | 30 913 764 | 12,09 % |

| 8 | Elephant Bet | 6 | 29 277 440 | 27 236 197 | 7,49 % |

| 9 | bet223 | 1 | 19 190 884 | 13 941 451 | 37,65 % |

| 10 | 1xBet | 57 | 18 976 210 | 16 581 154 | 14,44 % |

Egypt Is Doing the Work. Sub-Saharan Africa Isn’t.

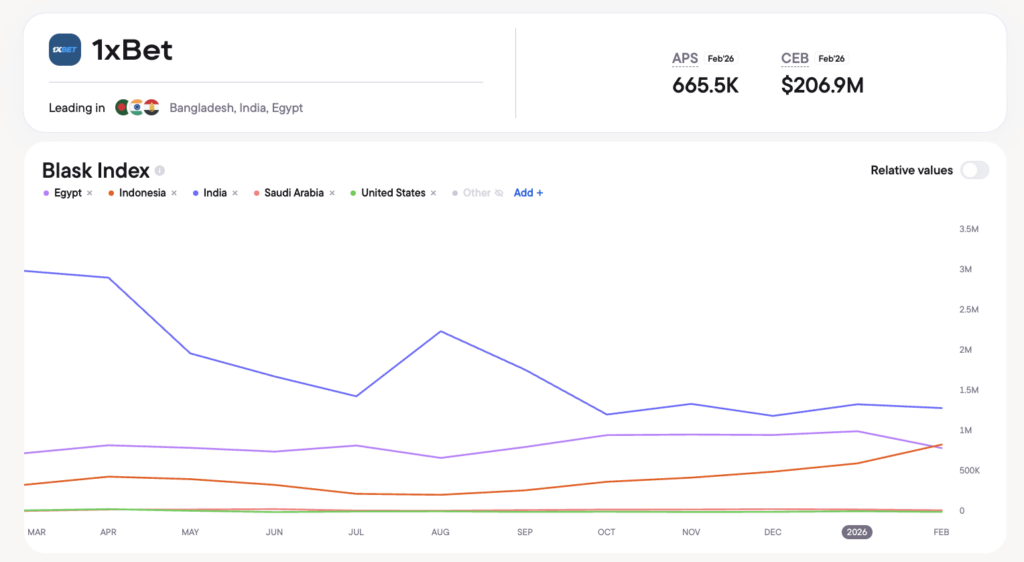

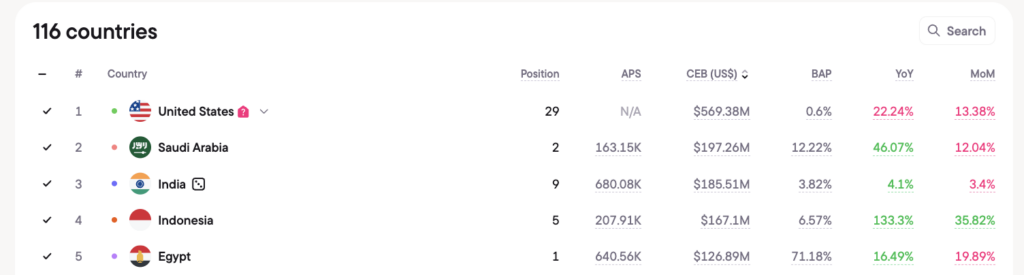

Understanding why the disparity exists requires separating 1xBet’s Africa presence from its Africa performance. Blask data for February 2026 shows 1xBet’s global Competitive Earning Baseline at $206.9M across 116 countries, with an Acquisition Power Score of 665.5K.

Within its top markets by CEB are the Saudi Arabia ($197.26M, +46.07% YoY), India ($185.51M, +4.1% YoY), Indonesia ($167.1M, +133.3% YoY), and Egypt ($126.89M, +16.49% YoY). The brand’s own global dashboard identifies its leading geographies as Bangladesh, India, and Egypt.

Africa’s largest iGaming economies — Nigeria, South Africa, Kenya, Tanzania — do not appear in 1xBet’s global top five. Egypt is its only African market with sufficient player demand to register at that level, and Egypt’s market structure is closer to MENA than to sub-Saharan Africa in terms of competitive dynamics and product behavior.

This means 1xBet’s 57-market African footprint is generating demand that is heavily concentrated in one country and dispersed thinly across the rest. Wide is not the same as deep.

A Regulatory Map With Gaps

1xBet’s sub-Saharan footprint has also not been uniformly stable.

In Ivory Coast, the platform was deactivated in March 2024 following a government decree that prohibited the operation of concession-linked games by any entity other than the National Lottery of Côte d’Ivoire (LONACI). The shutdown affected operators who had been running under third-party licensing agreements, and LONACI publicly directed players to redirect to authorized alternatives.

In Liberia, 1xBet entered the market through a licensed entity operating as LipayBet, then rebranded to its global identity — triggering a regulatory dispute with the National Lottery Authority over the scope of the original license and its applicability to online casino operations.

In Kenya, the most commercially developed sports betting market in East Africa, April 2025 brought a sweeping regulatory action: the BCLB blocked 58 unlicensed betting sites, halted Safaricom payment integrations for non-compliant operators, and imposed a 30-day blanket ban on gambling advertising across all media formats. Kenya subsequently enacted its Gambling Control Act 2025, the most comprehensive regulatory update in the country’s history. The operational environment for offshore-structured brands with local front-ends has become materially more difficult.

Ethiopia suspended 22 operator licenses in November 2025, citing non-compliance with financial reporting requirements and suspected concealment of earnings exceeding Br100 billion. The sweep reached executives and affiliated individuals across multiple cities.

None of these events individually define 1xBet’s African trajectory. Collectively, they illustrate why the headline market count — 57 countries — is an imprecise proxy for actual operational depth.

What betPawa Built Instead

The operator that sits at the top of Blask’s Q4 2025 Africa ranking took a different approach.

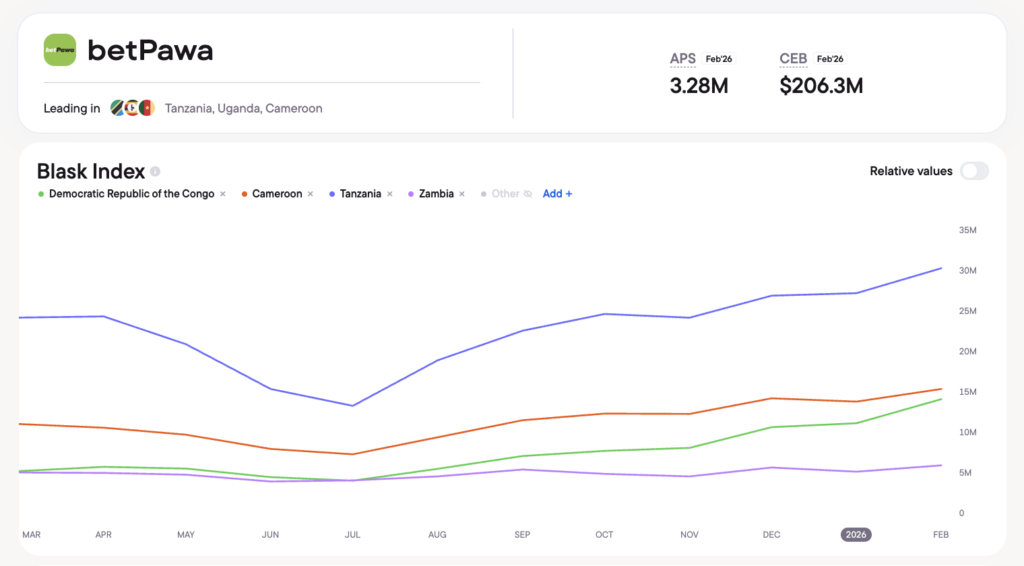

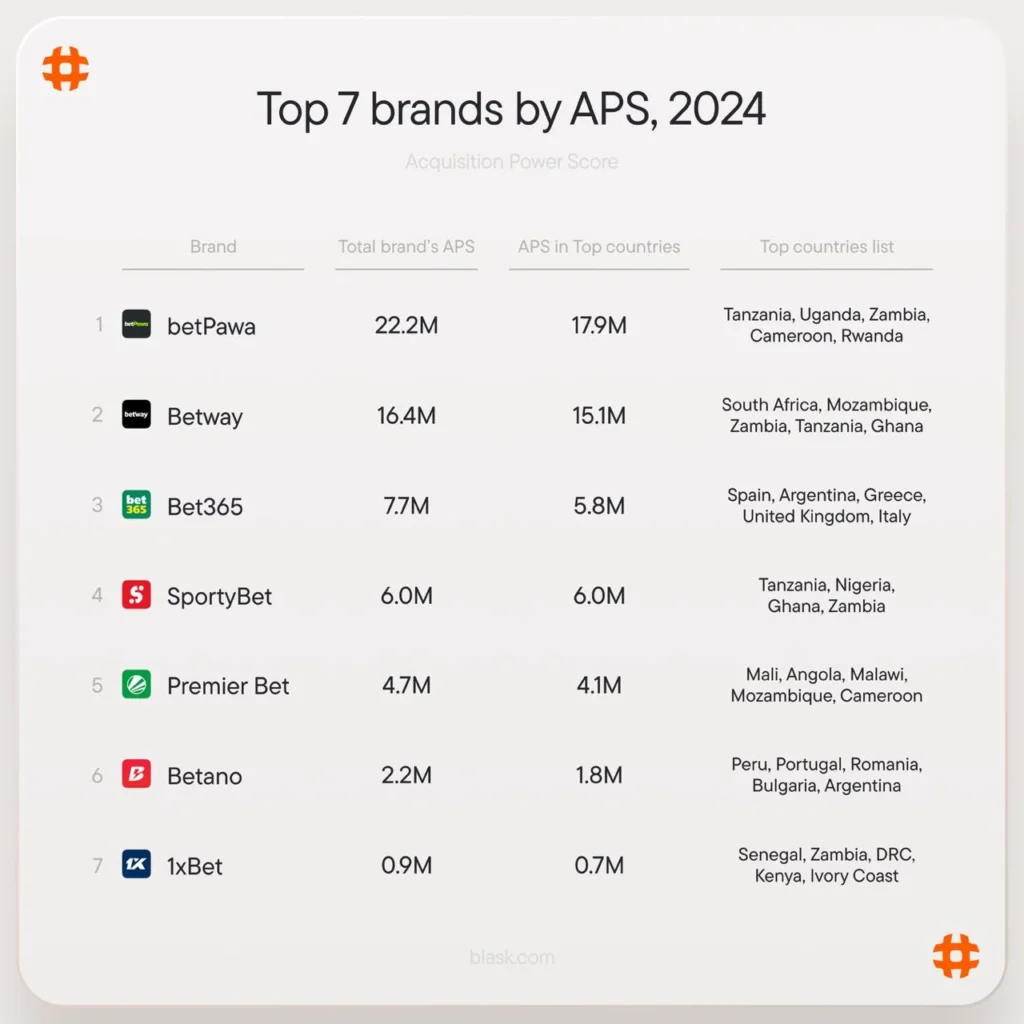

betPawa generated $75 million in annual revenue and serves over 10 million users across 27 markets. Its $1 minimum stake and mobile-first architecture — designed specifically for low-bandwidth, prepaid-SIM environments common in West and Central Africa — built it into the default betting reference in markets where the addressable audience is still connecting to the internet for the first time.

According to Blask’s 2024 regulated markets study, betPawa’s Acquisition Power Score reached 22.24 million — the highest of any iGaming brand globally across regulated markets.

The entire figure comes from African markets. “Africa’s explosive mobile internet growth has propelled our brand,” said Kresten Buch, Chairman of pawaTech, citing the company’s 10-year history on the continent as the foundation for its current position.

betPawa does not hold CAF naming rights. It does not run fan zones at AFCON. Its Blask Index in Q4 2025 is 13.7 times higher than 1xBet’s.

The comparison is not about which model is superior in a general sense. It is about what gets measured. Sponsorship spend and market count measure investment. Blask Index measures outcome.

The Sponsorship Paradox

1xBet’s CAF relationship is commercially rational from a brand-building perspective. The AFCON 2025 delivered 121 goals across 52 matches, a packed stadium final, and a historic revenue record for CAF — the number of sponsors grew from nine in 2021 to 23 in 2025. The tournament provides 1xBet with exposure in every African broadcast market simultaneously, which is harder to achieve through individual country-level marketing programs.

But brand exposure and brand habit are different things. A player who sees 1xBet branding on the AFCON perimeter boards in Rabat and then places their next bet on betPawa — because betPawa is faster to load, accepts a smaller minimum stake, and pays out through M-Pesa in 15 seconds — represents exactly the gap the Blask data is measuring.

In February 2026, Simon Westbury, 1xBet’s Strategic Advisor, told Yogonet that the company’s approach is to “engage, look to the future, and work with the industry” as it navigates regional regulatory complexity. The statement signals a company in active positioning mode — aware that the operational model that built its global footprint requires adaptation in markets where local licensing, local payment rails, and local product architecture are increasingly non-negotiable.

What the Data Measures

The Blask Index does not measure revenue, self-reported GGR, or marketing budget. It measures the degree to which a brand has become a genuine player habit — the volume of market interest generated over time, normalized across geographies.

By that measure, Africa’s most distributed operator is not Africa’s most embedded operator. A brand can sponsor the continent’s biggest football tournament and still rank behind a company that has never appeared on a CAF perimeter board.

The market is not rewarding presence. It is rewarding depth.

Blask Index data referenced in this article covers African markets tracked by Blask as of Q4 2025. Global CEB and APS figures reflect February 2026 Blask platform data. The full Q4 2025 Africa operator ranking was produced by Blask in partnership with Find More Africa.