- Updated:

- Published:

33 licensed brands run New Jersey’s $5.7B gambling market. 300 others want in.

New Jersey tracks 334 online gambling brands operating within its borders. 33 of them hold a state license. The rest (301 offshore platforms) do not. Yet the licensed minority captures roughly 73% of what Blask estimates to be a $5.7 billion market, the highest domestic share of any fully regulated U.S. state.

The ratio is the product of twelve years and two regulatory launches: online casino in November 2013, sports betting in August 2018. No other state has run the experiment this long. The result is not a clean win for regulation — more than a quarter of all dollars wagered by New Jersey residents still flow to unlicensed operators.

But it is the strongest evidence available that channelization compounds over time, and that the alternative — partial regulation or none at all — leaves far more money offshore. The Blask data makes the case not through abstraction but through the specific, traceable behavior of 334 brands competing for the same players in the same state.

A country-sized market in a single state

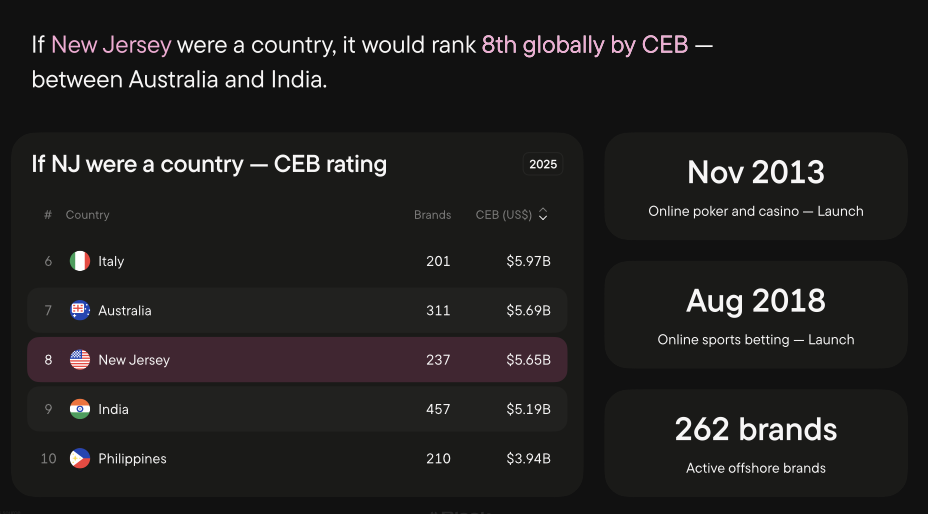

If New Jersey were a sovereign nation, its $5.65 billion in estimated online gambling activity would rank it eighth globally by CEB — between Australia ($5.69 billion, 311 brands) and India ($5.19 billion, 457 brands). The state houses 237 tracked brands. Among those, 262 operate offshore. The sheer density of competition in a single American state exceeds the brand counts of most national markets.

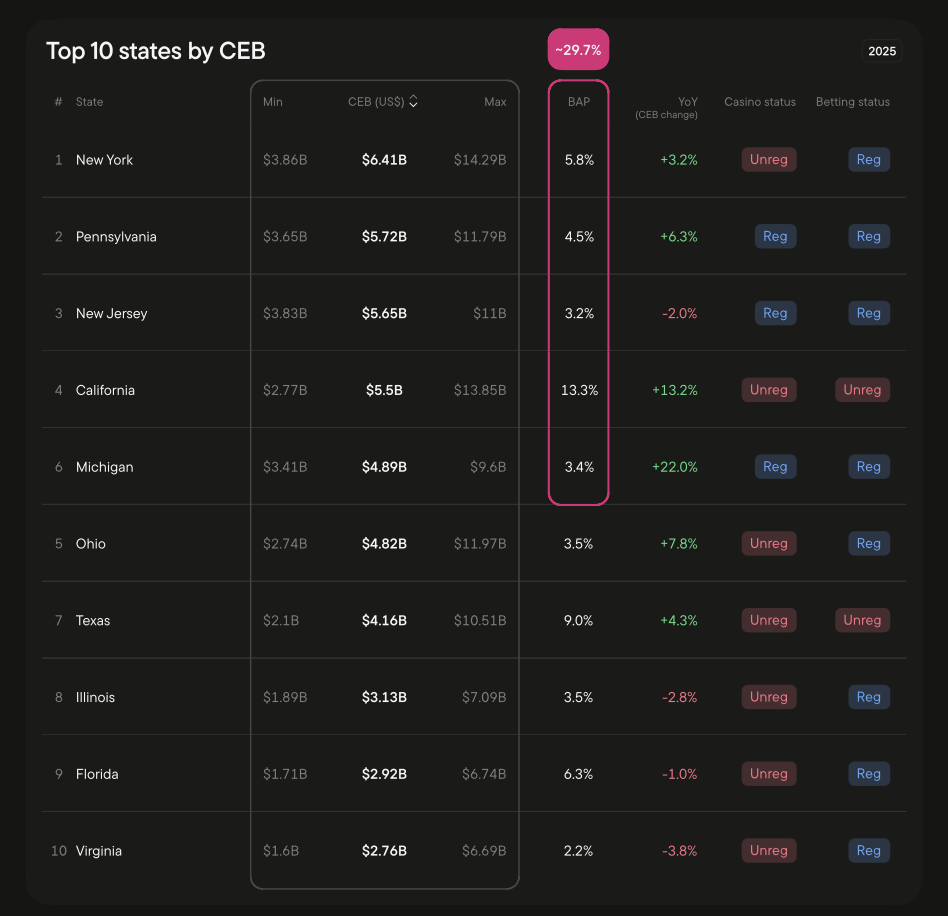

New Jersey is the third-largest U.S. state by total online gambling volume, trailing only New York ($6.41 billion) and Pennsylvania ($5.72 billion). But it is the only one of the three where both online casino and sports betting are fully regulated — a structural advantage that explains the domestic share gap.

New York, which licenses sports betting but not casino, channels roughly 39% domestically. Pennsylvania, which licenses both, channels approximately 55% but launched later. New Jersey, with twelve years of regulatory maturity, channels 73%.

The math is direct: full product licensing plus time equals channelization. Partial licensing does not.

The thirty-three

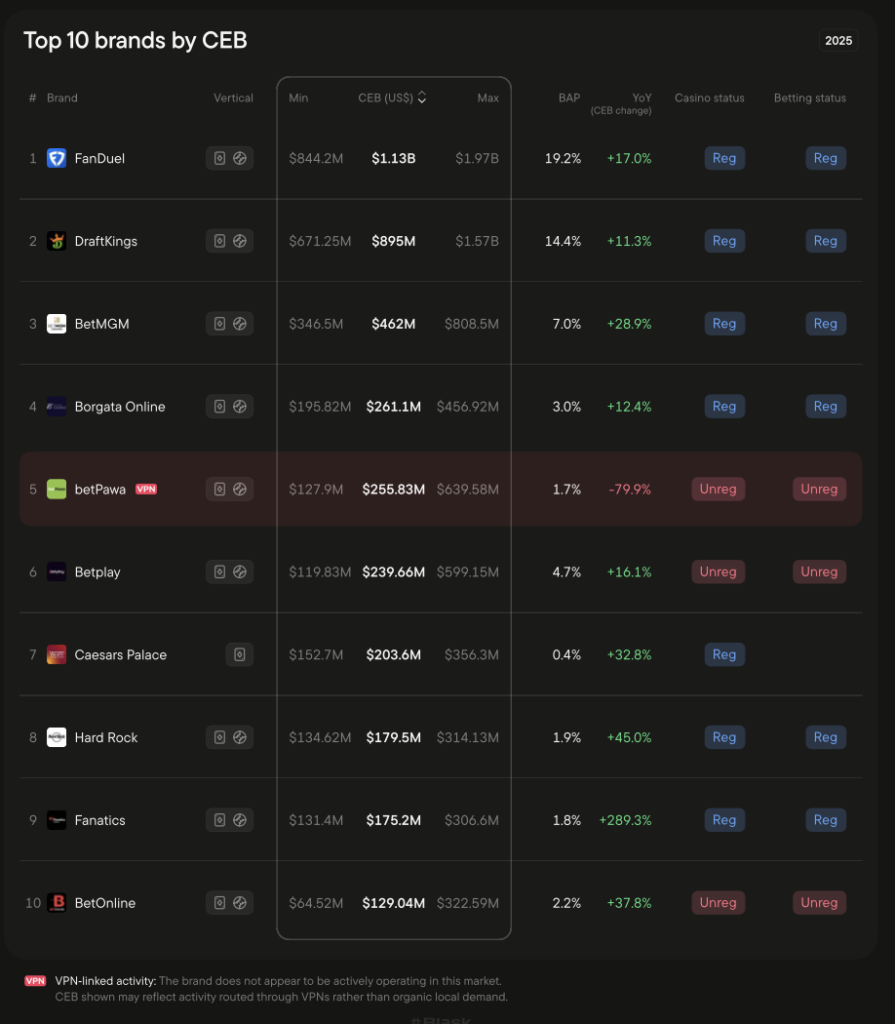

The licensed brands that dominate New Jersey are the same names that dominate American sports media, stadium signage, and broadcast advertising.

FanDuel leads with approximately $1.13 billion in CEB and 19.2% BAP, up 17% year-over-year. DraftKings follows at $895 million and 14.4% BAP, growing 11.3%. BetMGM, at $462 million, posted the strongest year-over-year growth among the top three — 29% — and holds licenses in both casino and betting.

Below the big three, the picture fragments. Borgata Online, the legacy Atlantic City brand now operating under the MGM umbrella, generates $261.1 million and holds 3% BAP. Caesars Palace sits at $203.6 million but commands only 0.4% of accumulated player attention — high revenue, low stickiness. Hard Rock, at $179.5 million, grew 45% YoY.

Then there is Fanatics. The sports merchandise company that entered online gambling generated $175.2 million in New Jersey CEB — and grew 289.3% YoY, the fastest expansion of any licensed brand in the state. The number is still small relative to FanDuel or DraftKings, but the trajectory is steep enough to shift the competitive balance within two to three years.

TheScore, the brand that absorbed ESPN BET after that sportsbook’s high-profile rebranding, holds $16.75 million in CEB but 5.89% in BAP. BetRivers generates $109.5 million. Bet365 holds $90.2 million.

All 33 licensed brands, by definition, pay New Jersey taxes, submit to state audits, and comply with responsible gambling frameworks. The 301 offshore brands do none of this.

The uninvited competition

The offshore contingent in New Jersey is not a collection of marginal operators. It includes betPawa, which Blask flags for VPN-linked activity and which recorded $255.83 million in CEB despite an apparent 79.9% YoY decline — a figure so large it suggests a correction in measurement methodology rather than an actual business collapse. Betplay, another unlicensed brand, generated $239.66 million and grew 16.1%. BetOnline, the oldest surviving offshore brand serving New Jersey, posted $129.04 million and grew 37.8%.

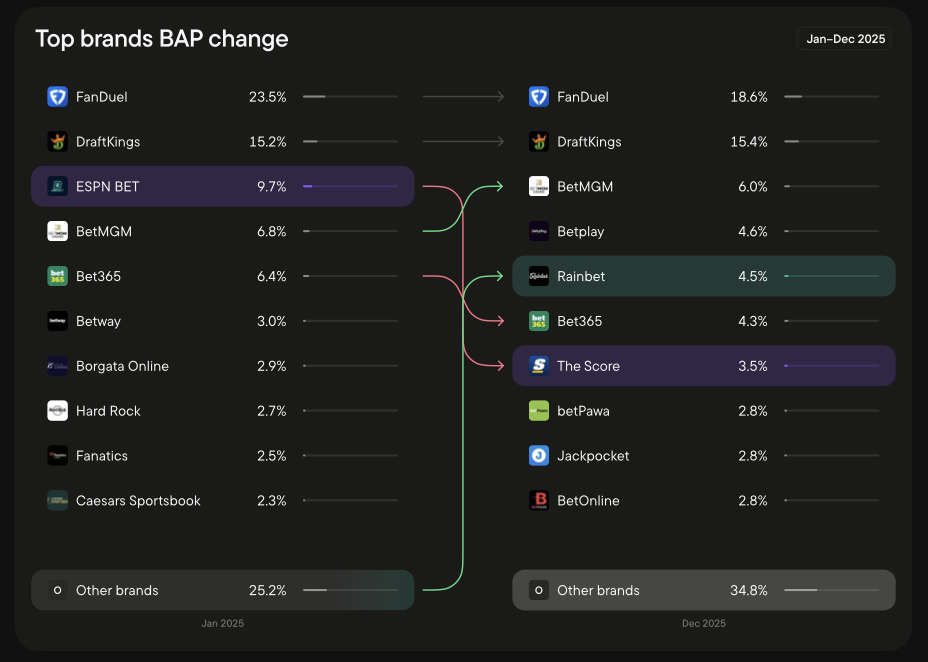

A notable development in 2025 was the emergence of Rainbet, an unregulated crypto-gambling platform that broke into New Jersey’s top five brands by BAP share — reaching 4.5% by December — despite not appearing to actively operate in the state. The brand does not hold a New Jersey license. Its rise coincided with the collapse of ESPN BET’s attention share: in January 2025, ESPN BET held 9.7% of New Jersey BAP. By December, ESPN BET no longer existed. TheScore, which replaced it, held 3.5%. The gap was filled not by another licensed operator but by an offshore crypto platform.

The competitive landscape shifted measurably over 2025. FanDuel’s BAP fell from 23.5% in January to 18.6% in December — still dominant, but loosening. The share of brands outside the top ten grew from 25.2% to 34.8%, a fragmentation pattern that suggests the long tail of offshore operators is collectively gaining ground even as individual licensed brands grow in revenue.

What New Jersey players actually want

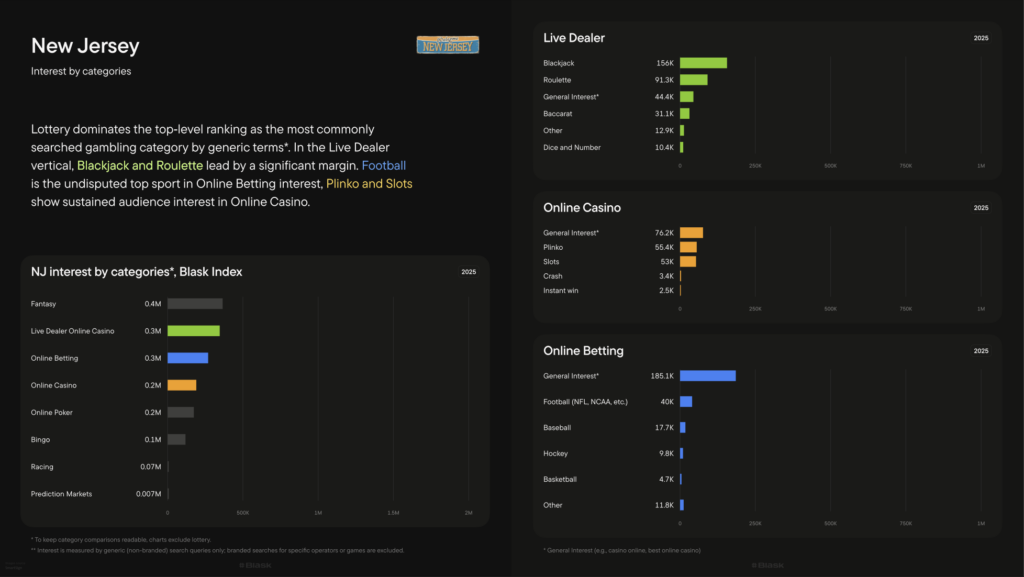

The Blask interest data for New Jersey reveals demand patterns that explain both the success of domestic operators and the persistence of offshore ones.

Fantasy sports generates the highest overall search interest in the state — 400 000 Blask Index units — a category entirely captured by licensed operators. Live dealer casino generates 300,000 units, with blackjack (156,000) and roulette (91,300) accounting for the majority. Online betting generates 300,000 units, dominated by general interest (185,100) and football (40,000). Online casino generates 200,000 units, with Plinko (55,400) and slots (53,000) as the leading specific interests. Online poker, once the product that launched New Jersey’s regulated market, generates 200,000 units.

The distribution matters because it reveals where offshore operators retain advantage. Plinko — a category that barely existed two years ago — generates more New Jersey search interest than slots. It is a product category driven almost entirely by offshore and crypto platforms. Crash games, another offshore-native product, generate 3,400 units. These are not categories where licensed New Jersey operators compete effectively.

The Offshore floor

The domestic growth numbers since 2024 are unambiguous. Licensed operators grew their combined CEB 17.1%. Offshore CEB declined 34.8% — the sharpest offshore decline of any state in the Blask analysis. The market is consolidating in favor of regulation.

But the remaining 27% that flows offshore is not a transitional figure. It is structural. It represents players who seek products not available domestically, platforms that accept payment methods licensed operators cannot offer, and a crypto-gambling ecosystem that operates outside the regulatory framework entirely. The rise of Rainbet and the persistence of betPawa suggest that the offshore floor in a fully regulated state is not shrinking toward zero — it is being rebuilt by a new generation of operators with new products and new payment rails.

For states considering legalization in 2026, the New Jersey data offers a specific benchmark: full regulation of both casino and sports betting, maintained over a decade, in a competitive multi-operator environment, can be expected to capture roughly 70% of total online gambling demand. The remaining 30% is not a failure of regulation. It is the cost of operating within a legal framework while competitors do not.

The lesson is that regulation succeeds — but on a timeline measured in decades, not legislative sessions.