SB 761 — Maryland’s online casino referendum vehicle — was pulled in March 2026. Blask data shows 290 brands were already active in the state before the bill ever reached a vote.

Maryland came close. For the second consecutive session, the state legislature advanced a bill that would have put online casino legalization to a public referendum. For the second time, it didn’t survive.

Senator Ron Watson, the bill’s own sponsor, withdrew SB 761 on March 13, citing the state’s $1.5B budget deficit and the political risk of a referendum at a time when tax revenue from existing gambling operations was already under pressure. The companion regulatory bill, SB 885, collapsed with it.

The debate, however, was almost beside the point. The market the bill would have regulated already exists.

What SB 761 would have done

Maryland’s existing casino framework gives six land-based operators — including MGM National Harbor and Caesars Baltimore — exclusive control over gaming licenses. SB 761 would have asked voters to amend the state constitution to allow those six casinos to offer mobile online gaming, with platforms like FanDuel and DraftKings leasing access to their licenses.

The bill never reached a vote. The Baltimore Sun editorial board noted that the state and the city were not aligned on the regulatory approach, adding friction to an already contested process. A poll conducted by Lake Research Partners for the National Association of Attorneys General in October 2025 found 71% of Maryland voters opposed iGaming legalization.

The state’s official rationale was fiscal: with a $1.5B budget gap and declining revenue from licensed sports betting, new gaming tax projections were speculative. The political calculus followed.

290 brands, one legislature

While legislators debated, operators moved. Blask tracks 290 active brands in Maryland across December 2025 through February 2026 — a figure that includes both licensed sportsbooks and offshore casino operators with no formal presence in the state.

What the Blask Index measures: Blask Index is an AI-enhanced demand signal built from search activity. It measures how much consumer interest iGaming brands generate in a market — a leading indicator of player behavior, not a lagging one from operator-reported financials. The total Blask Index for Maryland across this period stands at 322,051.

Estimated market revenue, measured by Competitive Earning Baseline (CEB), runs at an average of $496.2M ($293.4M–$1.1B range). CEB is Blask’s market-based revenue benchmark, built from brand strength and competitive dynamics rather than operator accounting. The spread in the range reflects the variance between conservative competitive assumptions and favorable ones across 290 active brands.

The maturity index for Maryland is 95 — the highest tier, indicating a market that operates like a fully developed one regardless of its formal regulatory status.

Licensed operators are losing. Offshore is not.

The divergence between licensed and unlicensed operators is where the data becomes pointed.

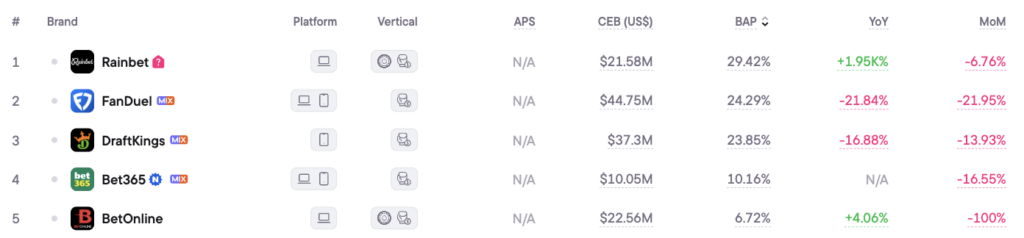

- FanDuel holds the top position in Maryland by Brand Accumulated Power (BAP) — Blask’s measure of a brand’s share of total market demand. Its CEB of $69.1M ($51.9M–$121M range). But demand is falling: FanDuel is down 21.84% year over year.

- DraftKings at rank two tells a similar story. APS of 3,315 (2,485–5,800 range), CEB of $56.7M ($42.6M–$99.3M range), and a YoY decline of 16.88%.

- BetMGM, at rank six, is down 38.47% year over year.

Across licensed operators, the average YoY change is –38.9%.

Now look at Rainbet. Blask flags the brand as non-domestic in Maryland — it does not appear to actively accept players from the state.

The demand is entirely player-driven: Maryland users are finding Rainbet on their own. That organic inbound search interest has grown +1,950.28% YoY. Rainbet now holds the largest BAP share in the state at 29.42%, ahead of FanDuel (24.29%) and DraftKings (23.85%). The CEB figure — $21.6M — reflects what the brand could capture if it operated in Maryland directly.

| Brand | Type | BAP | CEB (avg) | YoY |

|---|---|---|---|---|

| Rainbet | Offshore (non-domestic) | 29.42% | $21.6M* | +1,950.28% |

| FanDuel | Licensed sportsbook | 24.29% | $44.8M | –21.84% |

| DraftKings | Licensed sportsbook | 23.85% | $37.3M | –16.88% |

| Bet365 | Licensed sportsbook | 10.16% | $10.1M | n/a (new) |

| BetOnline | Offshore | 6.72% | $22.6M | +4.06% |

| BetMGM | Licensed sportsbook | — | $12.7M | –38.47% |

CEB for Rainbet reflects estimated capture potential, not active revenue — Blask non-domestic flag applies. BAP and CEB are Blask benchmarks based on market positioning and behavioral data.

The offshore average YoY across tracked brands: +290.9%. The licensed operator average: –38.9%.

This isn’t a story about offshore operators taking share from a healthy licensed market. The licensed market was already contracting. Offshore demand grew into the gap — driven by players actively seeking out casino products that licensed Maryland operators can’t legally provide. Rainbet doesn’t even need to target the state: the players come anyway.

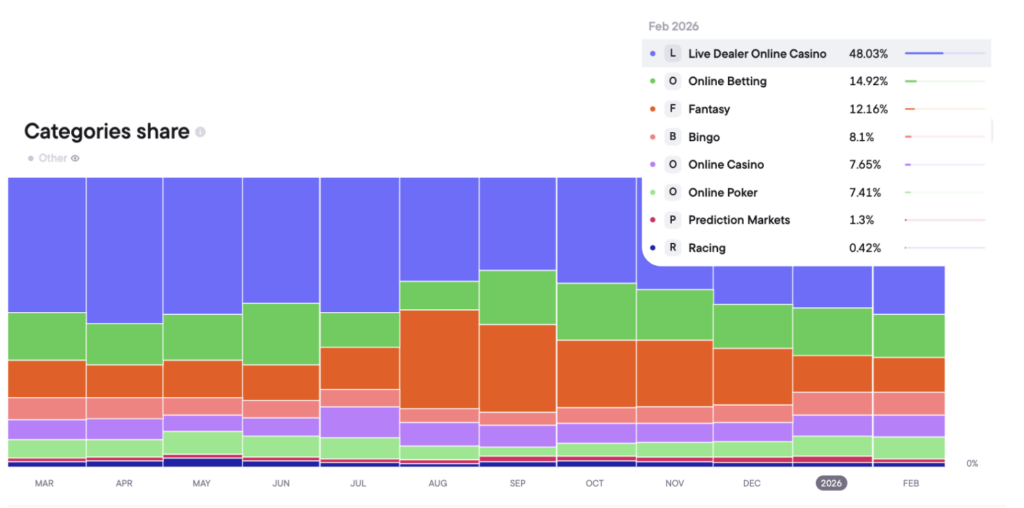

Casino demand is more than 3.5× the betting category

Maryland’s six licensed casinos hold a legal monopoly on physical gaming, but they cannot operate online. That creates a structural opening: all casino demand in Maryland has to go somewhere, and right now it goes offshore.

Blask’s category data for February 2026 shows Online Casino and Live Dealer combined generating more than 3.5× the demand of Online Betting. Lottery, driven by the state’s own platforms, dominates overall search volume — but when you isolate the categories that licensed sportsbooks compete for, betting is a fraction of the casino market.

SB 761 would have given licensed operators access to that casino demand for the first time. Without it, that demand continues to flow to operators like Rainbet, BetOnline, and others operating without a Maryland license.

The numbers from official state data make the opportunity cost concrete. Maryland’s February 2026 sports wagering handle reached $515.6M, up 8.4% year over year — driven by the NFL playoffs. But revenue came in at $51.1M, down 15%. The state collected taxes on a declining share of a growing handle.

Baltimore is fighting a different battle

While Annapolis debated online casino licensing, Baltimore sued six sweepstakes casino operators in March 2026: VGW (Chumba Casino, LuckyLand Slots), Stake.us, McLuck, Pulsz, High5Casino, and Fortune Coins. The city’s argument: these platforms use dual-currency mechanics to offer real-money gambling under the cover of “free play” promotions, in violation of Maryland law.

The lawsuit targets a segment that Blask data doesn’t fully capture — sweepstakes operators are harder to track than branded casino platforms. But the legal action signals where Baltimore’s concerns sit: not with sports betting, which is taxed and regulated, but with casino-style products that operate in legal grey zones.

The city and state are now pursuing parallel tracks. Baltimore is litigating against unlicensed operators. Annapolis failed to create the licensing framework that would have given consumers and operators a legal alternative.

What comes next

Maryland’s 2026 session ended without an iGaming bill. The 2027 session opens in January.

By that point, the market will have another year of offshore growth behind it. Rainbet, BetOnline, and whoever enters next will have accumulated more brand recognition, more player relationships, and more behavioral data that licensed operators cannot match from the inside.

The maturity index of 95 means Maryland already behaves like a developed iGaming market. What legalization would change is who captures the revenue — and who pays tax on it.

The state’s own budget documents have projected $1.3B in potential iGaming tax revenue over a multi-year horizon. For now, that money flows to offshore operators, out of Maryland’s fiscal reach.

The legislature will have to decide whether that outcome is preferable to the political risk of putting the question to voters.