- Updated:

- Published:

80% of US iGaming brands are offshore. The biggest one is Bovada

Bovada conquered the US, and became by far the largest iGaming brand in the world. But it is now starting to give ground under regulatory pressure.

Blask’s new report reveals that despite years of state-level legalisation, the US iGaming market is still dominated by offshore operators. 80% of brands serving US players and three of the top five by CEB (Competitive Earning Baseline, a projected revenue calculated by Blask) operate without any US licence. The largest of them is Bovada.

Pressure from regulators limited Bovada’s growth in states with regulation, but it continued to expand in unregulated states. And onshore brands are not always the ones who benefit from Bovada’s retreat.

This article draws on findings from Blask’s comprehensive report covering the US and Canadian iGaming markets — state-by-state and province-by-province breakdowns, offshore vs. domestic dynamics, brand rankings, and expert commentary.

The split: what the Blask report shows

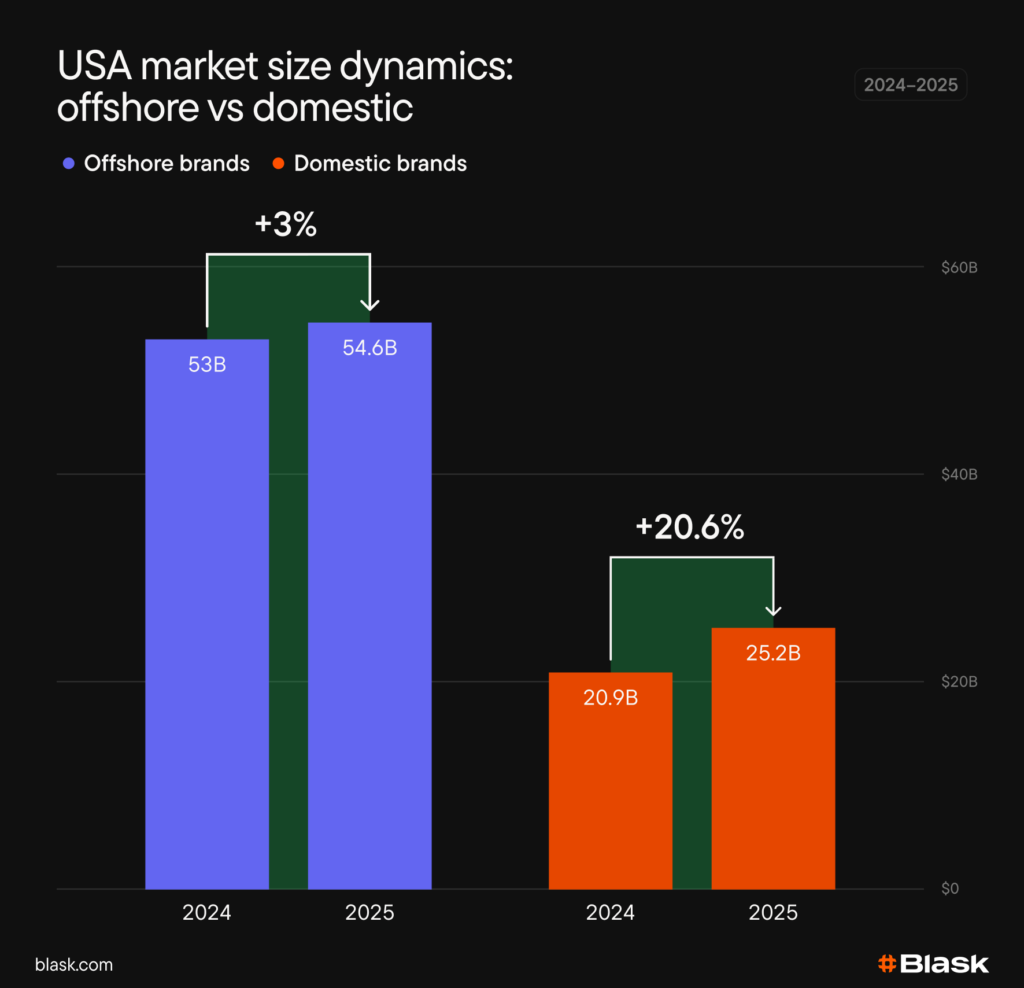

According to Blask data, the US iGaming market reached $79.8B in CEB in 2025 — by far the largest in the world. Offshore operators controlled over two-thirds of total market volume, but licensed brands grew faster. In 2025, CEB of onshore brands rose 20.6% year-over-year against 3% for their offshore rivals.

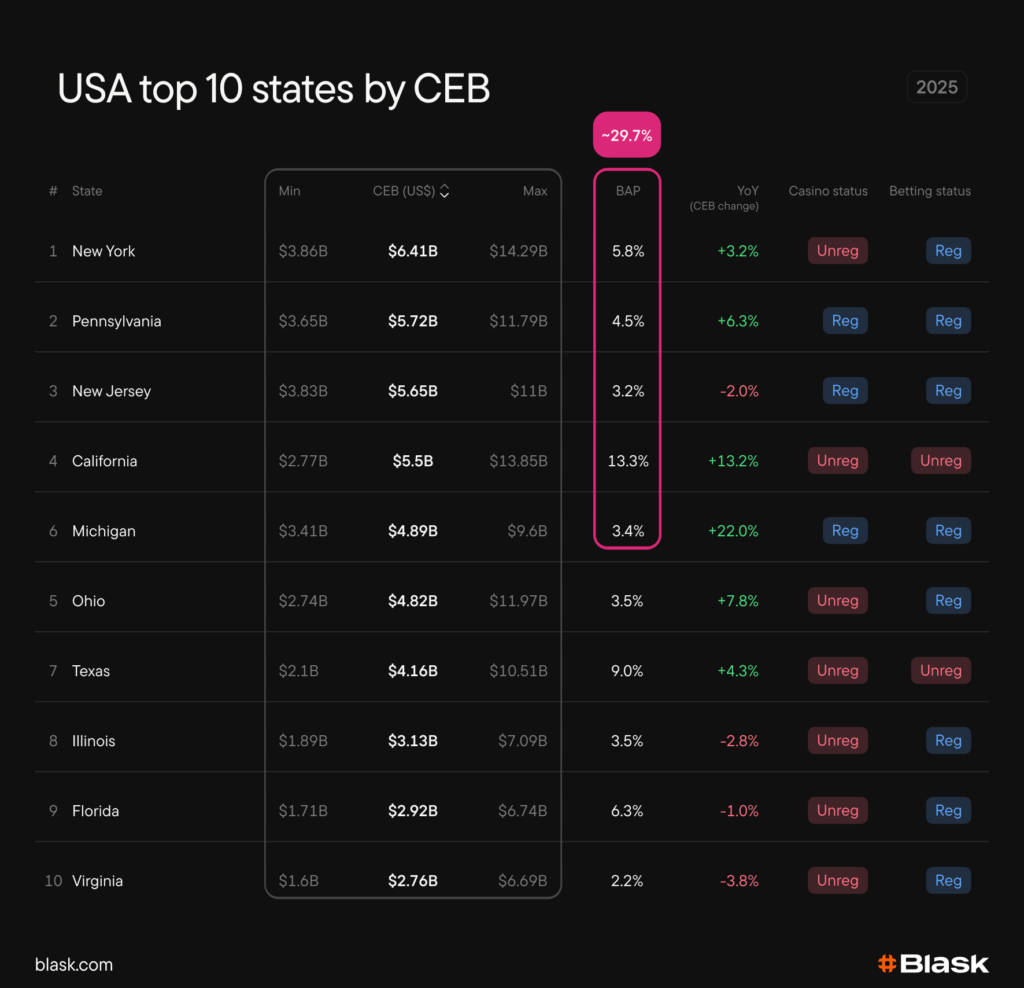

The onshore gain came mostly from seven fully regulated states — those with both online casino and sports betting. Domestic operators there were responsible for about 69% of CEB on average.

But across the 24 states with legal sports betting and no licensed online casino, offshore operators still accounted for about 72% of CEB on average. Without legal casino products, a large share of demand goes offshore by default.

Unregulated states like California and Texas demonstrate how large the offshore opportunity remains. Together these states generated almost $9.7B in CEB in 2025. If treated as standalone countries, California would rank eighth globally by CEB and Texas ninth.

Those two states are the primary revenue source for the largest iGaming brand in the world — Bovada.

The offshore brand that is bigger than most countries

Bovada launched in December 2011, spun off from the Bodog brand that had served US players for years before federal pressure forced a restructuring. It inherited Bodog’s US player base and built from there — operating under a Curacao licence.

According to Blask data, Bovada’s CEB in 2025 was $9.25B. That makes it the largest iGaming brand in the world, ahead of every national market except the top three — the US, UK and Canada. Almost all of Bovada’s CEB comes from the US.

The brand’s core states are California and Texas. Together they generated a third of Bovada’s US CEB in 2025. Bovada also dominated there in terms of user demand, measured by Blask Index. Bovada’s BAP (Brand’s Accumulated Power, a brand’s share of total market potential) in 2025 was over 29% in California and over 31% in Texas.

Across the whole country, Bovada’s BAP was 16.3%. It grew 1.5 percentage points from 2024 to 2025, even under intensified pressure from regulators.

Regulation capped Bovada, but didn’t reverse it

From 2024, state regulators began issuing cease-and-desist letters to Bovada directly. By early 2025, more than a dozen states had sent letters or listed Bovada as restricted.

Bovada did not stop growing after that. In 2025 its US CEB grew by 11.6% compared to 2023. But that growth became increasingly concentrated in states where it still had room to operate freely — California and Texas alone accounted for roughly 64% of Bovada’s entire US growth over that period.

In almost all states that ended up on Bovada’s restricted list, the brand’s share of CEB and BAP fell in 2025 compared to 2023. In Michigan, Pennsylvania, Connecticut and Massachusetts, licensed brands like DraftKings, FanDuel and BetMGM expanded as Bovada weakened. In others, like Arizona, Bovada lost ground but some of the displaced demand went to other offshore operators.

Regulation and enforcement did not eliminate Bovada’s US presence. They rather capped its expansion, preventing Bovada from growing in restricted states the way it still grew where it had space.

The gap remains

Bovada built its position by serving the US markets that regulation had not yet reached. Together with other offshore brands it still controls the vast majority of the country’s CEB. The momentum, however, is shifting — licensed operators are growing six times faster, and the regulatory perimeter keeps expanding.