- Updated:

- Published:

Pragmatic Play is a true leader: introducing the provider content share metric

Pragmatic Play dominates across regions, while the mid-tier leaderboard stays fiercely contested.

Blask launched a new provider content share feature in Blask Games. Here’s what the data says about dominant iGaming suppliers across Europe, LatAm, and Africa.

| Provider content share reflects the provider’s share in casino lobbies. WoW and MoM fluctuations can provide operators and game providers with the data about competitive shifts and enable them to identify emerging trends. |

Strategic applications

This metric delivers key insights for both operators and game providers:

- iGaming operators. When entering a new jurisdiction, one of the key questions is which game providers go first. Provider content share enables operators to identify leading studios in the market and prioritize integrations with high-performing suppliers.

- Game providers. Studios can use provider content share metric to evaluate their position in the market, track their key competitors, and refine regional expansion plans.

Blask’s new metric is also a robust resource for iGaming journalists for analytical articles and market research.

Regional market analysis

There is the same pattern in each country: Pragmatic Play heavily dominates the market. In the majority of jurisdictions it has no contenders, the battleground is in the mid-tier leaderboard. This analysis focuses on top countries by CEB in three key regions: Europe, Latin America, and Africa.

Europe

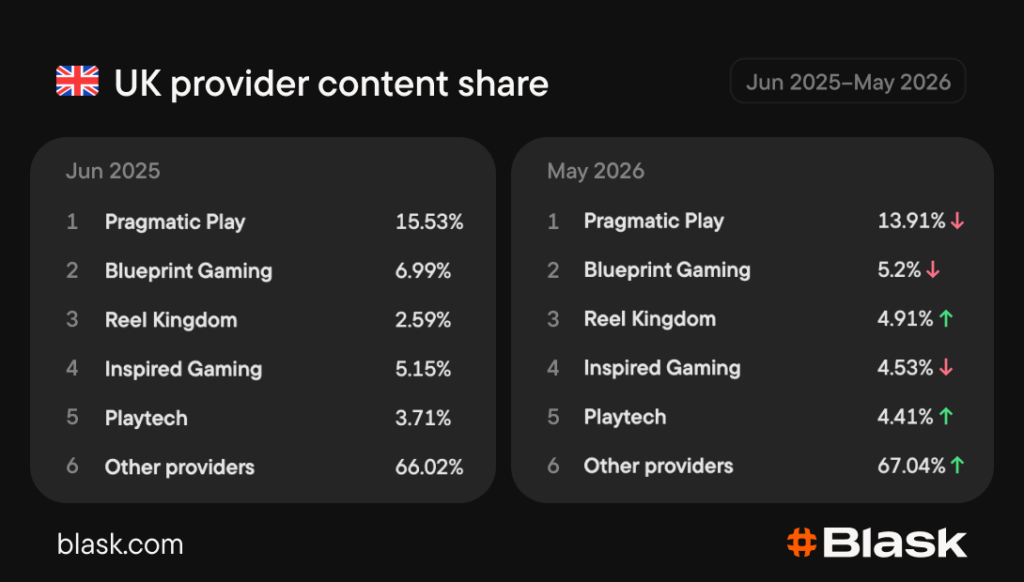

United Kingdom. Pragmatic Play is an undisputed leader here. Its nearest rival, Blueprint Gaming, accounts for content share that is twofold lower than Pragmatic’s commanding figures.

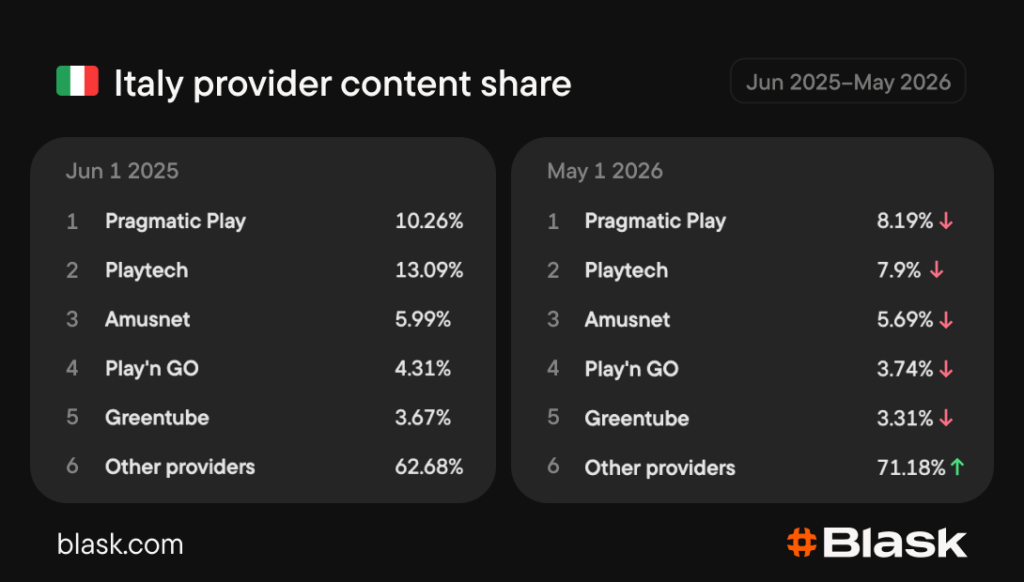

Italy. Pragmatic Play and Playtech are locked in a tight race. Data from June 2025 and May 2026 indicates a stable equilibrium: both suppliers hold almost equal content share.

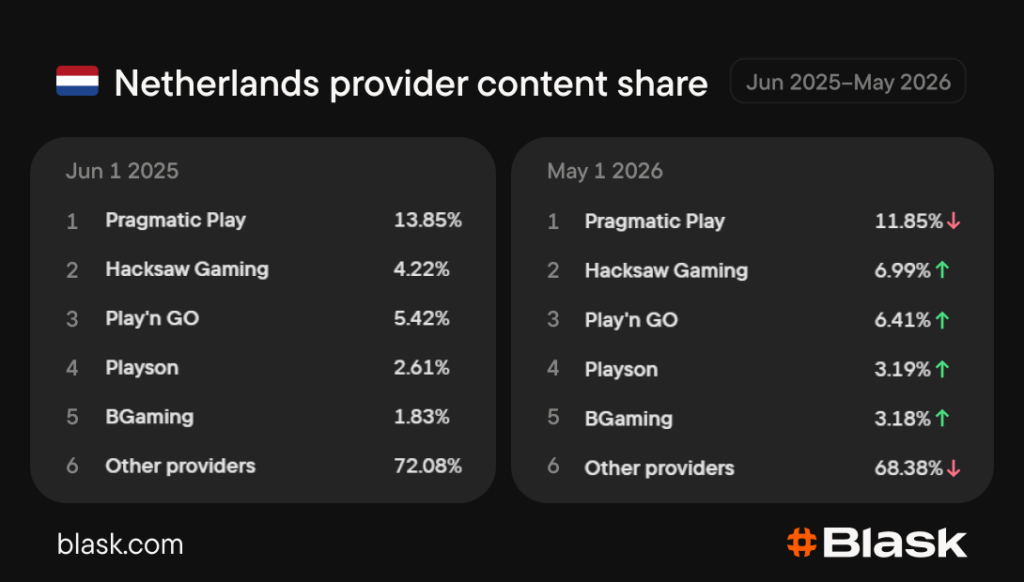

Netherlands. Pragmatic dominated the Dutch landscape in 2025, while other iGaming suppliers were far away. As of May 2026, the leader retains its top position, though competitors’ shares showed a year-over-year growth.

Latin America

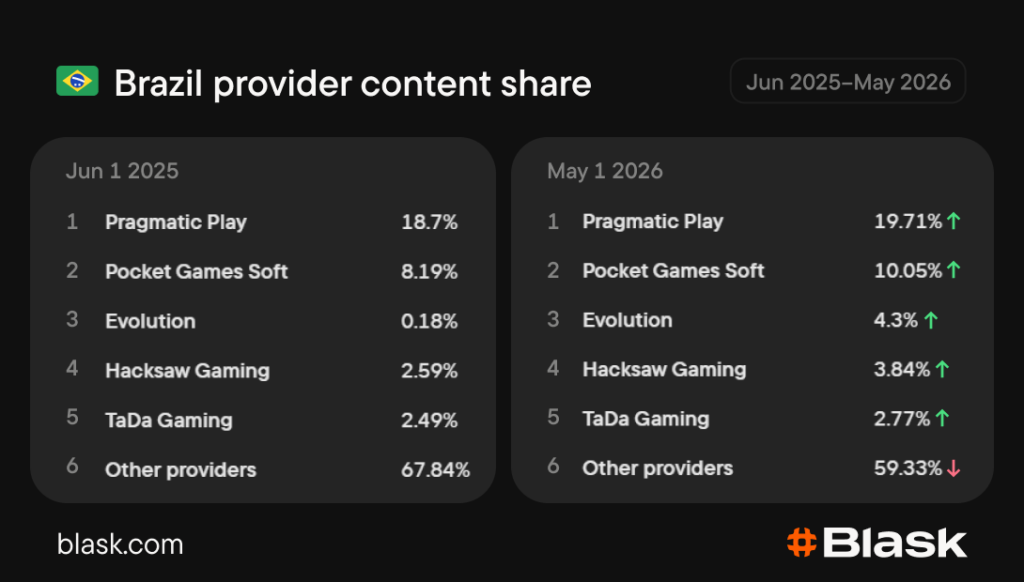

Brazil. The Brazilian market is driven by two suppliers: Pragmatic Play and Pocket Games Soft. There’s a twofold difference in their content shares.

Before July 2025, other game providers struggled to cross a 2% threshold. However, Evolution, Hacksaw Gaming and TaDa Gaming gained their content shares, indicating potential for further expansion.

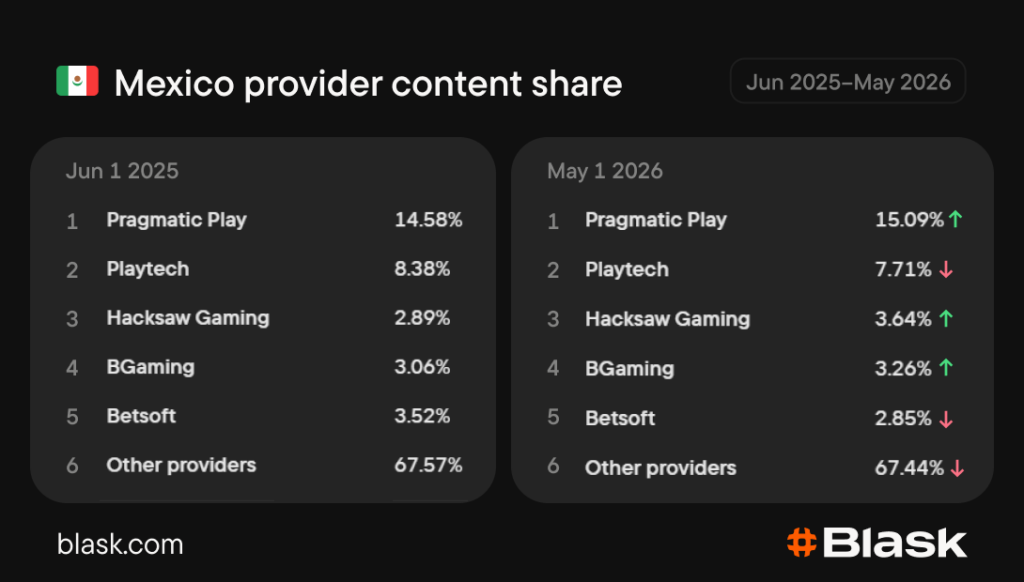

Mexico. Pragmatic Play outperforms Playtech in this jurisdiction. Usually, the dominant force in the segment secures a comfortable 13%-15% content share, while Playtech stabilizes within the 7% to 9% range.

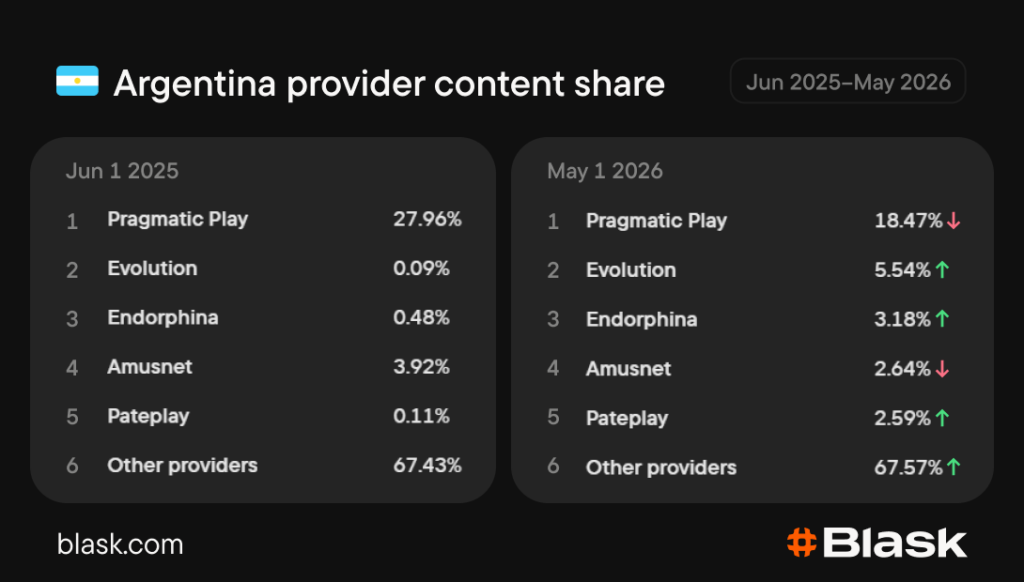

Argentina. Pragmatic Play dominates Argentina with a threefold content share advantage over Evolution at second position.

By June 2025, Argentina had consolidated almost entirely around Pragmatic Play. As of May 2026, the situation has changed — top 5 providers gained their shares and exceeded the 2% threshold.

Africa

South Africa. Pragmatic Play is also a leading provider in this GEO.

BGaming and Hacksaw Gaming are engaged in a close contest for second place with almost equal shares. Moreover, other providers also are gaining traction, for example RealTime Gaming (RTG) and Red Tiger Gaming are narrowing the gap with top-tier competitors.

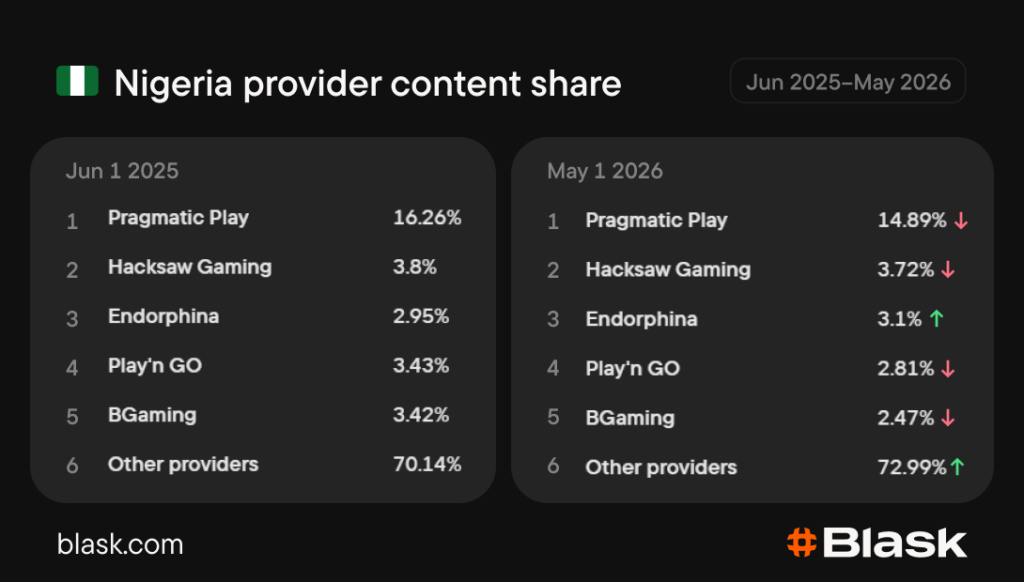

Nigeria. No surprise — Pragmatic Play dominates the market. Hacksaw Gaming, Endorphina, Play’n’GO, and BGaming have maintained comparable content share levels over an extended period, but none of them are a threat to Pragmatic leadership. Although alternative suppliers are far from the leading market participant, there’s a battleground in the mid-tier leaderboard.

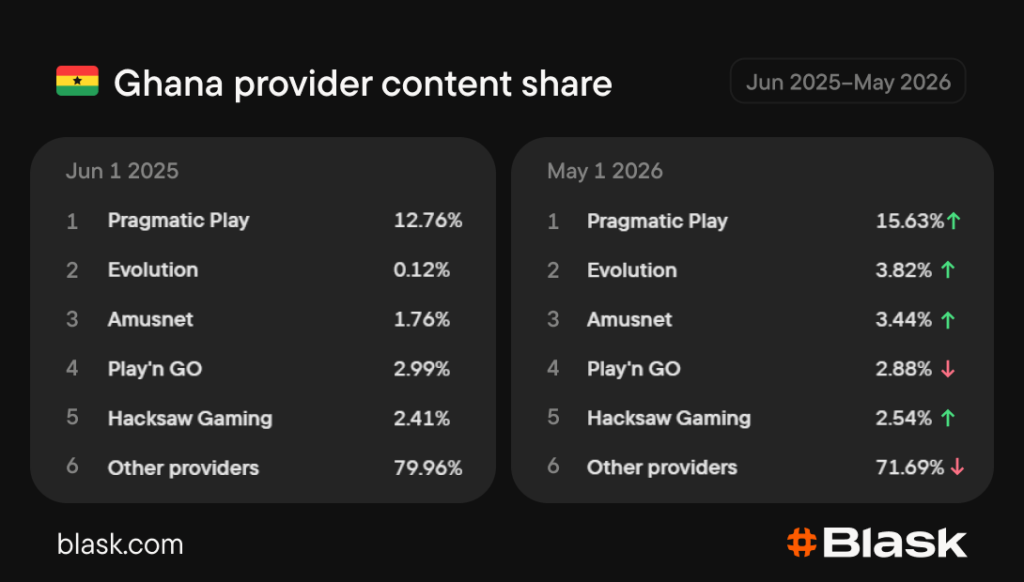

Ghana. Ghana follows the same pattern: near-total concentration around Pragmatic Play. With ~15% share each month, the studio dictates the market pace.

There have been positive shifts from June 2025: other providers started to gain their share, gradually diversifying the Ghanaian landscape.

Key takeaways

The data is consistent across all regions: Pragmatic Play leads, everyone else competes for second. The mid-tier is getting crowded, but the top spot isn’t up for grabs.