- Updated:

- Published:

Which iGaming markets are growing fastest in 2026

Nigeria grew player acquisition by 44% in 2025. Mexico matched it at 42%, Brazil’s first licensed year produced $7 billion in GGR, and Greece outpaced every European market in the second half of the year. Together, those shifts offer one of the clearest snapshots of iGaming industry trends 2026 and where demand is moving fastest, according to Blask data.

Online gambling markets don’t grow at the same speed, or for the same reasons. Some grow because regulation opens the door. Others grow because mobile penetration finally reached critical mass. A few grow because years of suppressed demand found a legal outlet overnight.

Heading into 2026, five markets stand apart from the rest: Nigeria, Mexico, Brazil, India, and Greece. Each tells a different growth story. Together, they make a case that the fastest-moving action in global iGaming is no longer happening in Western Europe.

How Blask measures market growth

Growth in iGaming is notoriously hard to measure. Operators don’t publish player counts. Revenue figures are self-reported, delayed, or jurisdictionally narrow. Third-party estimates vary by hundreds of millions.

Blask approaches this differently. Blask Index is an AI-enhanced demand signal built from search activity across all tracked brands in a market. It captures player intent — the behavioral footprint users leave before they bet — and aggregates it into a comparable measure across geographies. It’s a leading indicator, not a lagging one.

Two financial metrics underpin the market comparisons below:

- Acquisition Power Score (APS) estimates how many new customers a market’s brands collectively attract per period. It’s a min–avg–max range because acquisition varies by season, competitive intensity, and campaign timing.

- Competitive Earning Baseline (CEB) estimates total market revenue based on brand strength and competitive positioning — also a range, with the minimum reflecting conservative competitive conditions and the maximum reflecting favorable ones.

Neither metric relies on operator-reported data. That matters when comparing markets where reporting standards differ significantly.

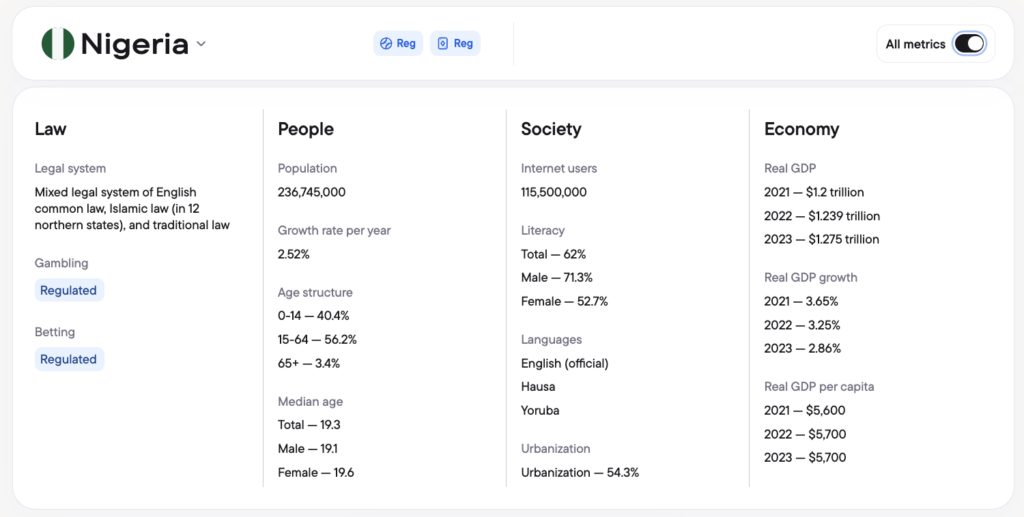

Nigeria: Africa’s fastest-growing acquisition market

Nigeria added more new iGaming customers in 2025, relative to its base, than any other major market in Blask’s dataset. Acquisition Power Score grew from an average of 8.0 million in 2024 to 11.6 million in 2025 (8.6M–20.4M range) — a 44% jump year-over-year.

Revenue followed. CEB moved from $500 million in 2024 to $634 million in 2025 ($473M–$1.1B range), up 26.8%.

The top brand, Bet9ja, reflects the market’s momentum. Its Blask Index grew 53.3% year-over-year — the highest growth rate among any major brand in the country. According to SiGMA, Nigeria’s online gambling market reached $3.87 billion by broader revenue estimates in 2025. Blask’s CEB figure captures the competitive brand-level view at $634 million, a narrower scope focused on the addressable licensed market.

The drivers are structural. Nigeria has a population above 220 million, a median age under 20, and mobile penetration that crossed 50% of adults in recent years. Sports betting became culturally embedded before casino products. That sequencing mirrors how several Southeast Asian markets matured a decade earlier, and it tends to produce sustained multi-year growth.

Nigeria’s 184 active brands are competing for a player base that is growing faster than any other market at comparable scale. That combination — high acquisition growth, strong structural tailwinds, still-fragmented competition — is rare.

Read also: Fastest growing online casino markets to watch in 2026

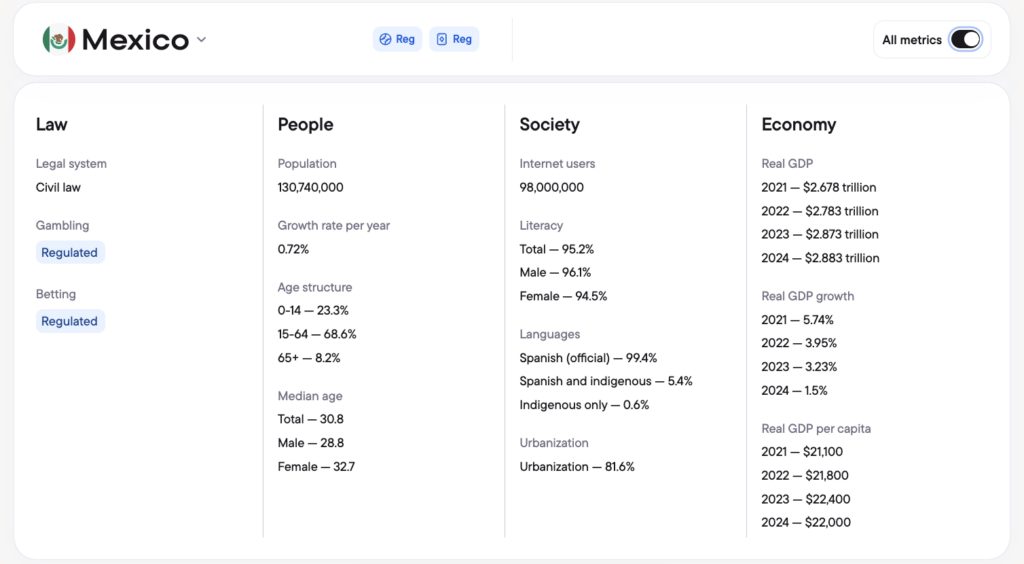

Mexico: LatAm’s rising acquisition engine

Mexico grew player acquisition 41.8% in 2025. APS moved from 2.5 million to 3.5 million (2.5M–6.4M range), and CEB rose 14.2% to $1.9 billion ($1.4B–$3.4B range).

The top brand, Caliente, grew its Blask Index 26.5% year-over-year. Its month-over-month growth in December 2025 reached 55.2%, suggesting the acceleration is still building rather than peaking.

Mexico’s trajectory differs from Nigeria’s. The digital infrastructure is already there: high smartphone penetration, an established payments ecosystem, and a large urban population accustomed to online services. What has been missing is regulatory certainty.

In 2025, Mexico’s betting sector underwent regulatory modernization, updating a framework that had remained largely unchanged for years. The iGaming Business Mexico Market Report 2026 describes the market as standing “on the verge of a new era” — still navigating uncertainty, but trending toward a more structured operating environment.

With 143 active brands and acquisition growth near 42%, Mexico is not a market that can keep being treated as a secondary LatAm play.

Brazil: The regulated reset

Brazil’s numbers require context. In January 2025, the country launched its regulated online gambling framework. The effect on Blask’s competitive market data was significant.

CEB fell from $7.2 billion in 2024 to $5.1 billion in 2025 ($3.4B–$10.1B range). That looks like a contraction. It isn’t.

The 2024 figure captured hundreds of unlicensed offshore brands competing for Brazilian players. Regulation removed them from the active competitive set. The licensed market alone generated BRL 37 billion ($7 billion) in GGR in its first year, according to the country’s betting regulator.

APS held steady, growing slightly from 76.7 million to 79.2 million (58.1M–142.5M range). Player acquisition didn’t slow. It consolidated into a smaller group of licensed operators.

The demand signal confirms the shift. Betting site traffic in Brazil surged 237% in 2025 relative to the pre-regulation baseline. Brazil’s Blask Index reached 2.57 billion — the largest of any single country in the dataset by a wide margin.

In absolute terms, Brazil is the largest iGaming market in Latin America. In growth terms, 2025 was a structural reset, not a growth year.

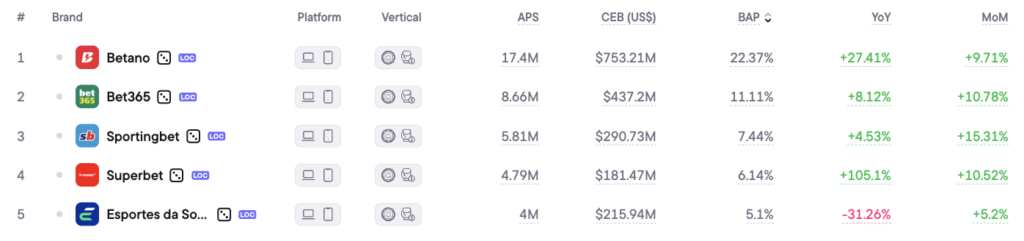

The question for 2026 is how fast the licensed brands compete for the demand that’s now theirs to capture. The #1 brand, Betano, grew 21.1% YoY. Bet365 holds #2 with an APS of 8.2 million new customers per year.

India: Scale without noise

India doesn’t post the growth rates Nigeria does, or the regulatory drama Brazil does. But at 462 active brands, a Blask Index of 567 million, and a CEB of $5.2 billion ($2.6B–$13B range), it’s the second-largest market in Blask’s data by revenue estimate.

CEB grew 11.8% in 2025 and APS held nearly flat at 19.1 million (+1% year-over-year). These are modest numbers, but “modest growth at $5.2 billion” still represents real scale.

The Indian government pegged the online gaming market at ₹23,200 crore (approximately $2.7 billion) and projects growth to ₹31,600 crore by 2027. That figure covers only platforms within the government’s formal framework — it’s narrower than Blask’s competitive view, which includes offshore operators serving Indian players.

The competitive structure in India is still fluid. The top brand, 4RABET, posted +73% Blask Index growth year-over-year — the highest single-brand growth rate of any major brand across all five markets. That kind of outlier performance signals an early-mover advantage playing out in real time: one brand capturing a disproportionate share of a market that is still deciding who it belongs to.

India lacks a federal regulatory framework for online gambling. Several states operate their own regimes. A national framework, if it emerges in 2026 or 2027, would likely produce a demand surge comparable to Brazil’s.

Greece: Europe’s fastest-growing market

Within Europe, Greece stood apart in 2025. In the second half of the year, iGaming demand grew more than 50% according to Blask data cited by iGaming Analytics, making it the fastest-growing regulated market in Europe.

Blask’s own figures show the sequential acceleration: total Blask Index in Greece was 47.9 million in H1 2025, rising to 56.7 million in H2 2025 — an 18.4% increase half-over-half. Full-year CEB reached $1.44 billion ($1.0B–$2.7B range), up 4.7% from $1.38 billion in 2024.

The top brand, Stoiximan, is a local operator that has held market leadership since Greece’s market formalized. According to iGaming Business, Greece has developed into a “thriving European iGaming hub” — a market combining a functional regulatory framework with strong demand driven by sports betting culture.

In a European context where most established markets are growing at low single digits — or not growing at all — a 50%+ half-year demand surge is a meaningful outlier.

Read also: European iGaming market outlook 2026: where demand is growing

What the fastest-growing markets have in common

Three patterns repeat across all five markets:

- Regulation as catalyst.

Brazil’s 237% traffic surge, Greece’s H2 demand jump, Mexico’s growing licensed brand base — all followed or accompanied regulatory change. Regulation doesn’t create demand; it converts latent demand into measurable, accessible activity. - Young demographics and mobile penetration.

Nigeria and India have among the youngest populations and fastest mobile growth globally. Player acquisition in these markets tracks mobile adoption as much as marketing spend. - Supply catching up with demand.

Fast growth often reflects suppressed demand finding a legal, accessible product for the first time. The Brazil traffic spike wasn’t new demand appearing overnight. It was existing demand moving from offshore to licensed channels.

Conclusion

Nigeria and Mexico posted the fastest player acquisition growth in 2025, at 44% and 42% respectively. Brazil restructured its entire market around a new regulatory framework and generated $7 billion in first-year licensed GGR. India scaled quietly to $5.2 billion while 4RABET grew 95% in a single year. Greece outpaced every European market in the second half of the year.

None of these markets is anywhere near the saturation levels of Western Europe. That is precisely why they belong in any serious conversation about the top iGaming markets 2026.