- Updated:

- Published:

Italy’s iGaming market keeps growing, but the field has narrowed

One of the world’s largest regulated markets closed 2025 with half the brands gone.

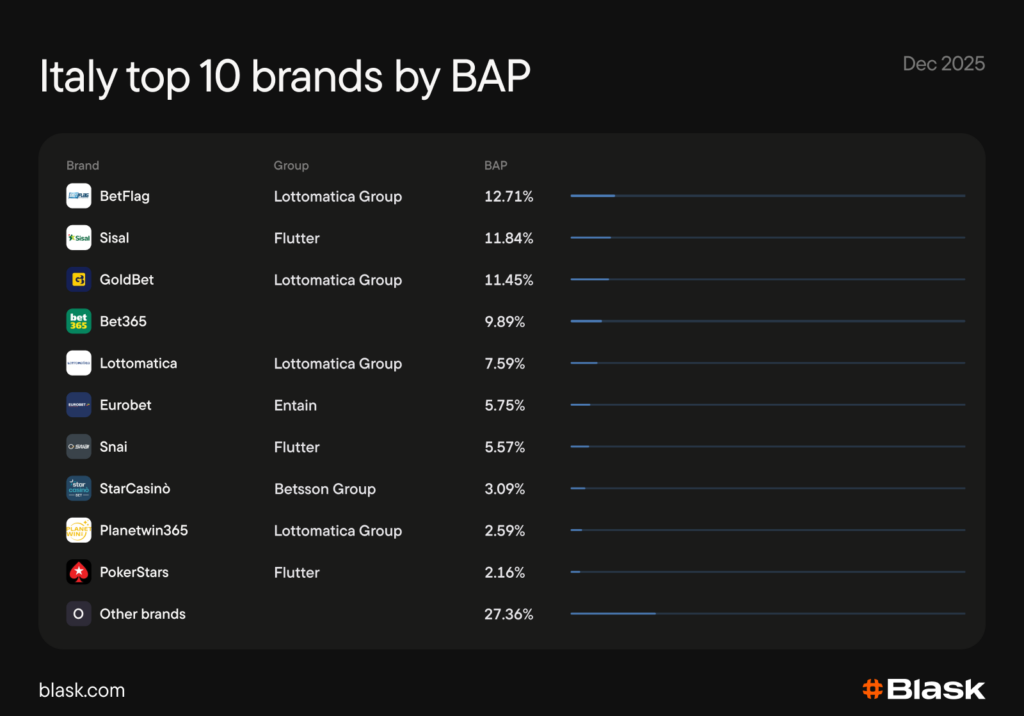

Italy is the largest iGaming market in continental Europe and it keeps expanding year after year. The pace is steady rather than explosive, but concentration is rising. Blask data shows that four operator groups account for about 72% of total digital attention, and the two largest portfolios — Lottomatica Group and Flutter — hold around 55% of BAP between them.

A market that keeps growing

Blask data shows that the Italian iGaming market is almost 2 times bigger than Germany’s and 2.5 times bigger than France’s by CEB in 2025. With a very low share of offshore operators, it is a mature market that slowly but constantly grows over the years.

According to official data, licensed operators generated €4.76B in GGR in 2025, up roughly 8% YoY. Online casino contributed over 64% of it. Since 2019 the official market has tripled, while according to Blask, the share of offshore brands decreased from over 20% to 2%.

Blask Index rose approximately 11% in 2025 versus 2024 on a yearly average basis, confirming that financial growth reflected higher audience engagement. But the number of operators capturing it changed dramatically.

From fragmentation to oligopoly

By December 2025, the top 10 brands in Italy accounted for 72.6% of the country’s BAP. Those ten brands roll up to four groups — Lottomatica Group, Flutter, Entain and Betsson — plus the standalone global brand bet365.

Outside the top 10, the portfolios extend further. Lottomatica Group also owns Totosì, Flutter controls Betfair, Entain is backed by bwin and Gioco Digitale, Betsson also operates through its own brand.

Taken together, those four groups plus bet365 held 75.7% of Italy’s total Blask Index in December. Lottomatica and Flutter alone were at about 55% by year-end. The concentration was built through a run of acquisitions between 2022 and 2025.

November’s regulatory reset

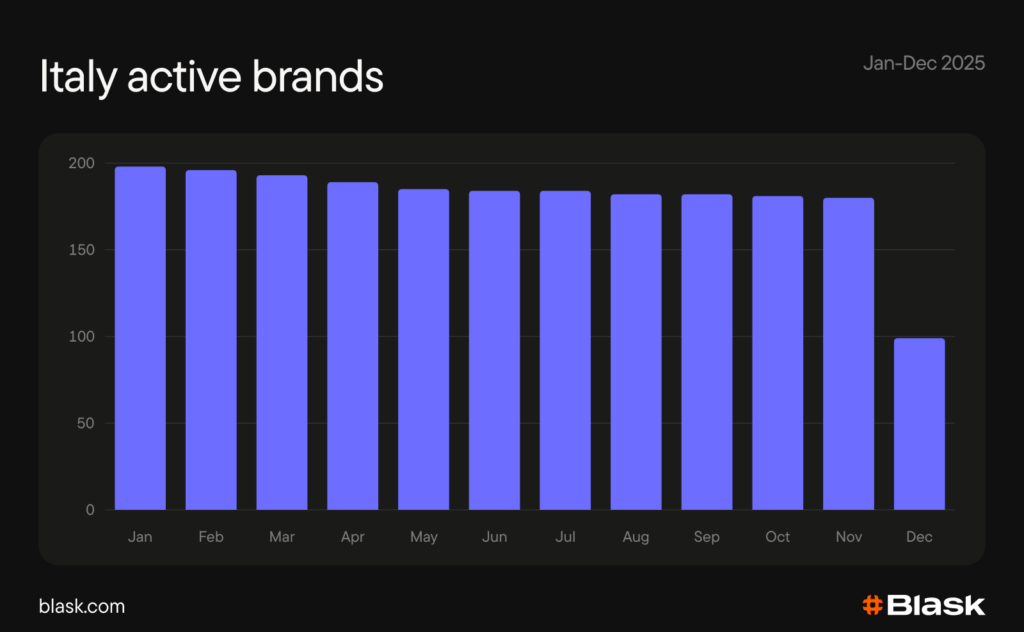

By the end of 2025, the rulebook tightened, leaving little room for new challengers. Italy’s new concession framework went live on 13 November 2025, compressing the market to 52 licences. The reform ended the “skin” model — secondary domains marketed as standalone brands under a parent licence — and moved the market to nine-year, non-renewable concessions priced at €7M each. That made the licence fee 35 times higher than before.

In Blask, the change looked like an exodus. The number of active brands still sat around 180 in November, then fell to 99 in December as the new framework took effect. The reset was structural: it made fragmentation harder to sustain and pushed the market towards well-capitalised operators. Among brands that exited the Italian market under the reset were such globally known names as Unibet, Betway and 1xBet.

What 2025 locked in place

Italy’s iGaming market structure did not form overnight. Over several years, the groups with capital and scale absorbed smaller operators, while regulatory pressure made standalone operation increasingly difficult. In 2025, the process of transformation was completed.