- Updated:

- Published:

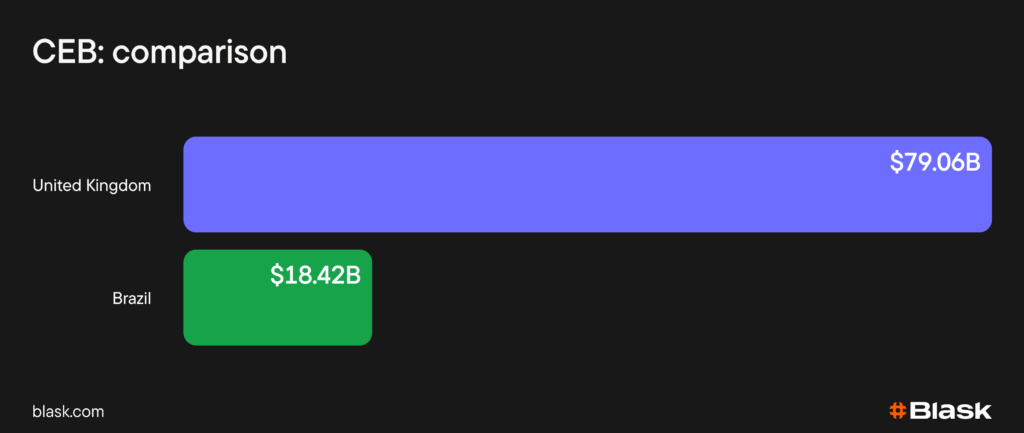

Reading the “X”: Brazil vs. UK, and how to actually use the Blask Index

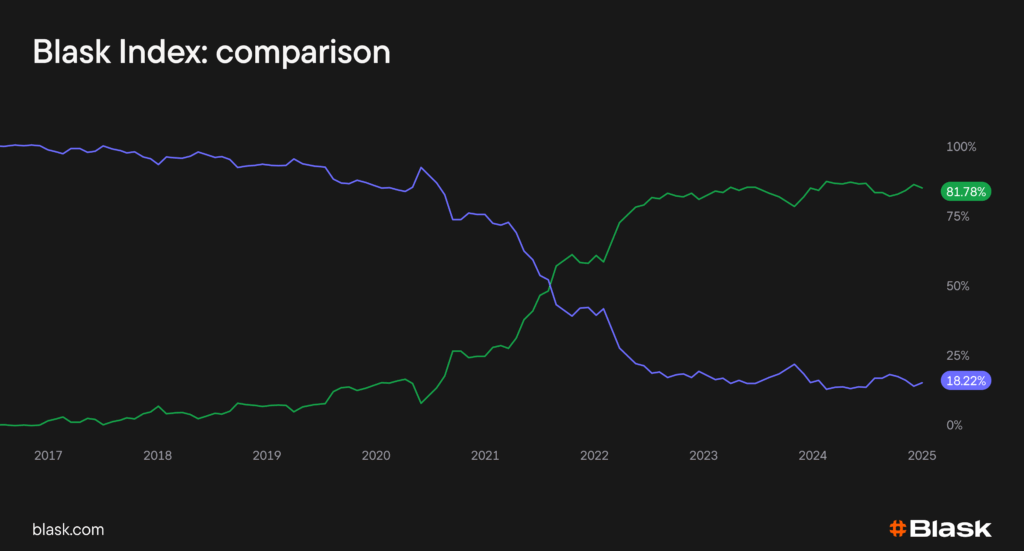

Let me start with a simple truth: the Blask Index is a benchmark of user interest — not a P&L statement. At least, not always. When one market’s line rises above another, it means more people are thinking about, searching for, or linking to brands there. Money might follow, but not automatically. That distinction matters if you’re allocating budgets or judging market health.

Brazil: the noisy acquisition phase

Brazil’s surge is real, but the “why” is marketing and infrastructure as much as “new demand.” Operators poured fuel on the fire — think R$1bn to sponsor all 20 Série A clubs, plus a grey market worth $3.4bn in 2022 flowing into legal channels and inflating search chatter.

On-ramps are almost frictionless thanks to Pix (used by 76% of Brazilians; 42bn payments in 2023) and a 5G backdrop that makes mobile UX feel instant.

In short: the crowd was already in the stadium; legalization turned on the floodlights and the megaphones. Early GGY? Razor-thin margins or losses while CAC is high and responsible gambling rules settle.

United Kingdom: the LTV-optimization phase

The UK looks “quiet” on radar — and that’s exactly the point. Compliance has added weight (credit-card ban in 2020; stake caps at £5/£2; affordability checks), and some activity moves into the shadows: ~£2.7bn in wagers and ~1.5m users. How much is it? That’s the entire population of Manhattan, for example.

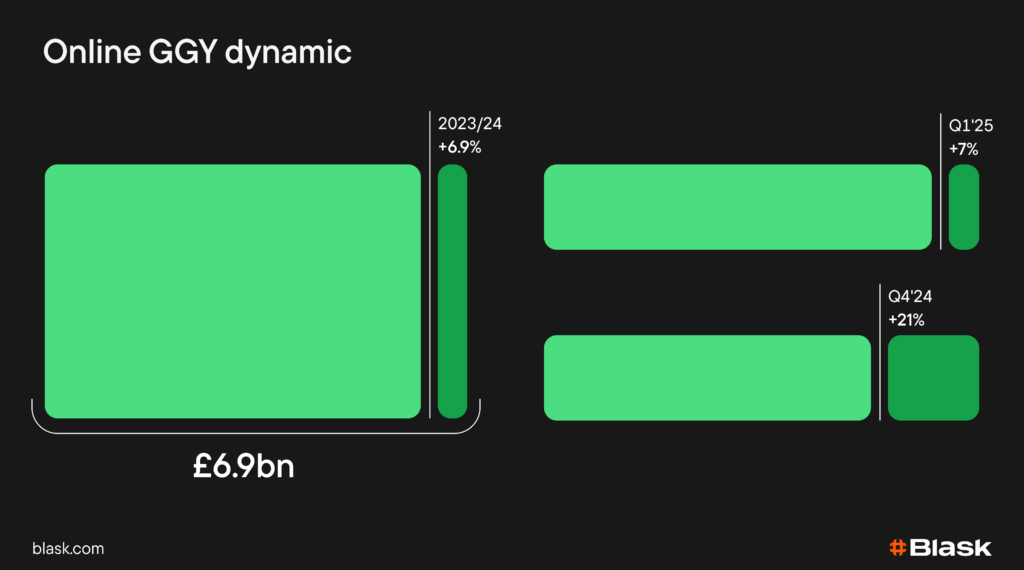

But the business headline is different: online GGY grew 6.9% to £6.9bn in 2023/24, with Q4’24 +21% and Q1’25 +7%; slots +11–15%. Mature market, loyal cohorts, omnichannel apps — less search, more direct. Quiet table, growing chip stack.

Why the lines form an “X”

Brazil and the UK are at opposite lifecycle stages: early land-grab vs. late-cycle consolidation.

- Regulation acts as catalyst vs. brake: Brazil’s law unlocked pent-up demand; UK rules cool it by design.

- Demographics & mobile: Brazil’s young, mobile-first population reacts strongly to marketing; UK uptake is already near-universal.

- And marketing firepower diverges: new entrants outspend in Brazil while UK budgets tilt to compliance.

That’s the “X” — marketing cadence, not a profit proxy.

Looking ahead

Consensus forecasts expect double-digit GGR growth in Brazil through 2028, with volatility around tax and responsible-gaming rules. In the UK, secondary legislation flowing from the white paper (rolling out in 2025) likely flattens or nudges the line down unless lower-risk, innovative products rekindle interest.

How to read the “X” (so you don’t misallocate capital)

If you bet strategy purely on the crossing lines, you’d overweight Brazil (drawn in by the roar, then find knife-fight margins) and underweight the UK (mistaking quiet for shrinking revenue while operators harvest loyal, profitable cohorts).

The fix is simple: layer financial KPIs over the Blask Index and segment markets by lifecycle — acquisition markets (Brazil, India, parts of LatAm): track CAC/LTV, media-cost inflation, regulator mood; optimization markets (UK, Italy, mature Nordics): track churn, wallet-share shifts, black-market leakage.

Keep an eye on UK compliance roll-outs — stake caps & vulnerability checks can nudge search as casuals re-research safer offers.

Bottom line

Blask Index tells you who’s loud, not who’s most profitable. Brazil is loud because it just got a microphone while the UK keeps cashing cheques behind sound-proof compliance walls. Read the phase — not just the volume — and make decisions where interest meets economics.