- Updated:

- Published:

Spain’s iGaming market: busy, not booming

A mature market closed 2025 with a sigh of relief — lawmakers dropped the bonus ban at the last step.

In December, lawmakers in Spain removed the iGaming provisions from the customer‑service bill at final passage after months of heated debates. The plan to re-ban welcome bonuses did not make it into law, leaving the existing framework in place as 2026 begins.

For years, Spain’s iGaming market has been shaped by a cycle of tightening restrictions, partial rollbacks, and court rulings. This regulatory rollercoaster has defined the market’s current structure, best understood through a combination of official and Blask data.

More on European trends: Spain, Germany, France, and 7 other markets — in our new Europe’s iGaming pulse report.

Scale and momentum

Spain’s iGaming market has expanded significantly since 2020. Data provided by market regulator (DGOJ) shows that gross gaming revenue (GGR) of all licensed operators rose from around €850M in 2020 to about €1.45B in 2024. Growth continued into 2025, with nine‑months GGR already exceeding €1.2B — roughly 1.5 times the full‑year total for 2021.

Since 2021, casino vertical has consistently accounted for over half of GGR, while sports betting hovered around 40%. This marks a shift from 2020, when sports betting led at 43% versus 41% casino.

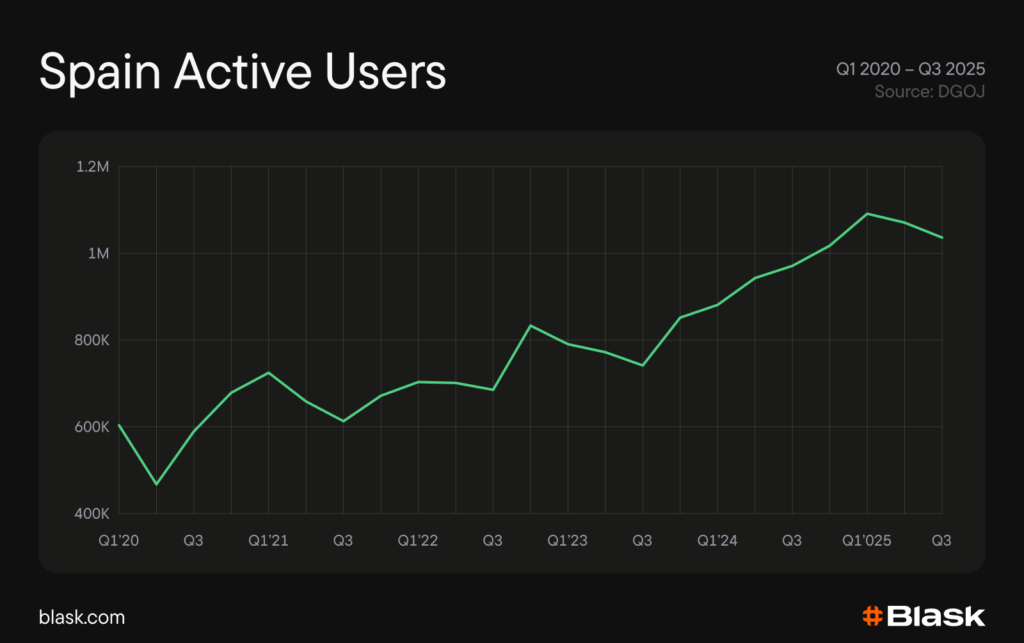

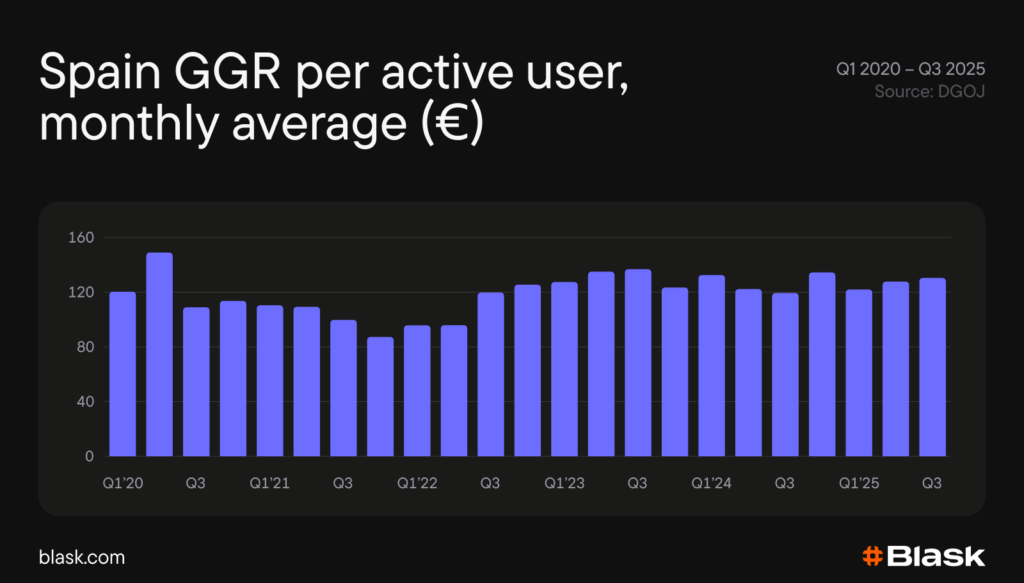

Participation has grown in line with revenue. In 2025, monthly averages stood at about 1.7M active accounts and just over 1M active players, up roughly 95% and 70% respectively from 2020 — a much broader user base. Despite this expansion, average monthly GGR per active user peaked in mid-2023 and has remained flat since, indicating that growth is driven by volume, not higher spend per player.

Competition

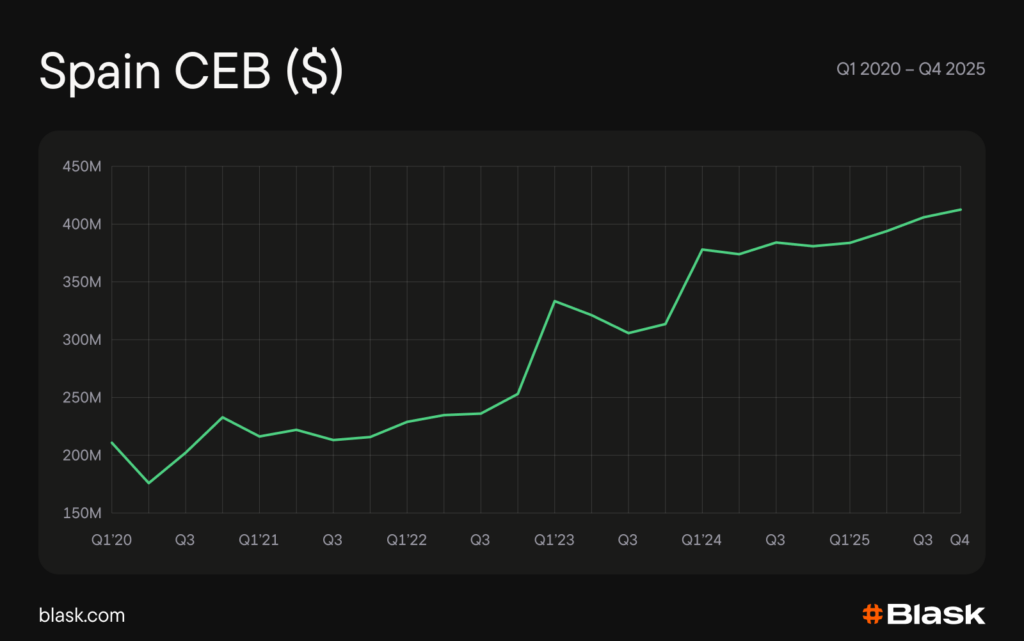

Beneath the official figures lies a competitive landscape detailed by Blask’s metrics. Brand Accumulative Power (BAP) captures overall brand reach, and Competitive Earning Baseline (CEB) reflects expected digital earnings. In late 2025, these metrics signalled a highly regulated, onshore-dominated market.

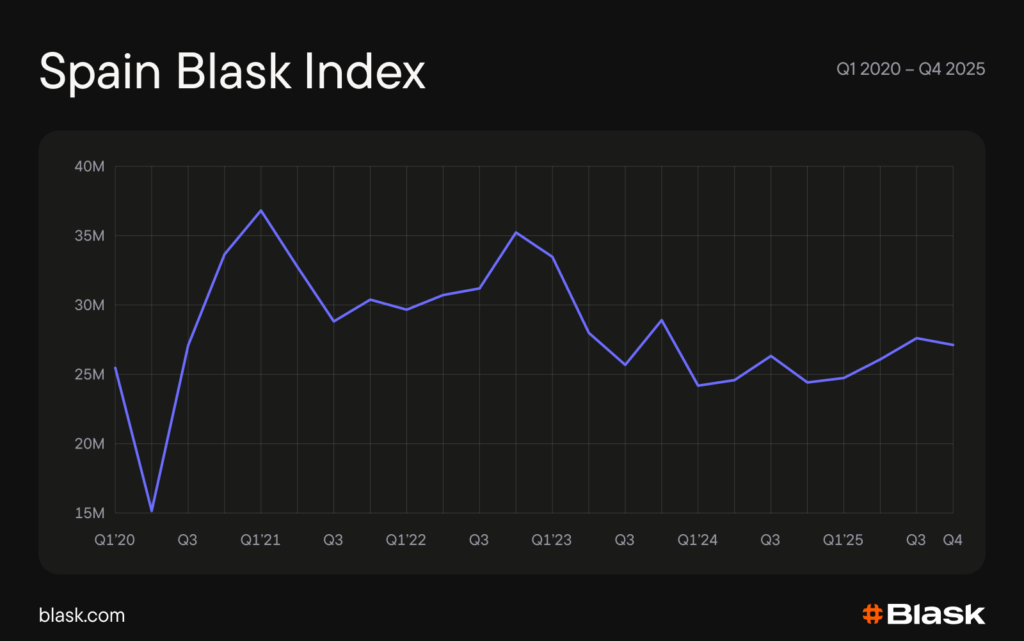

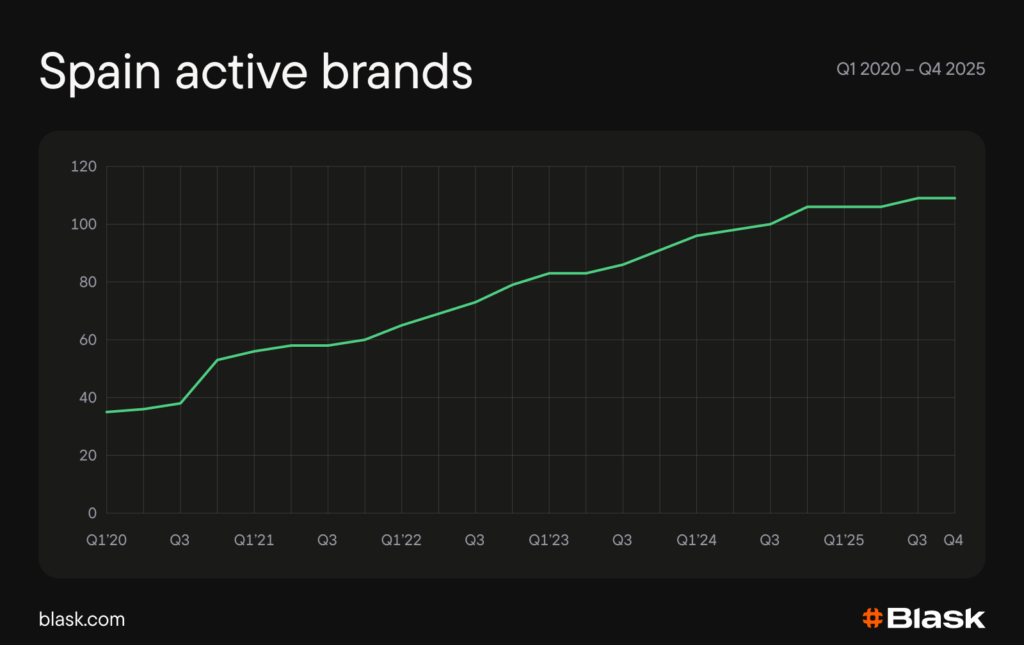

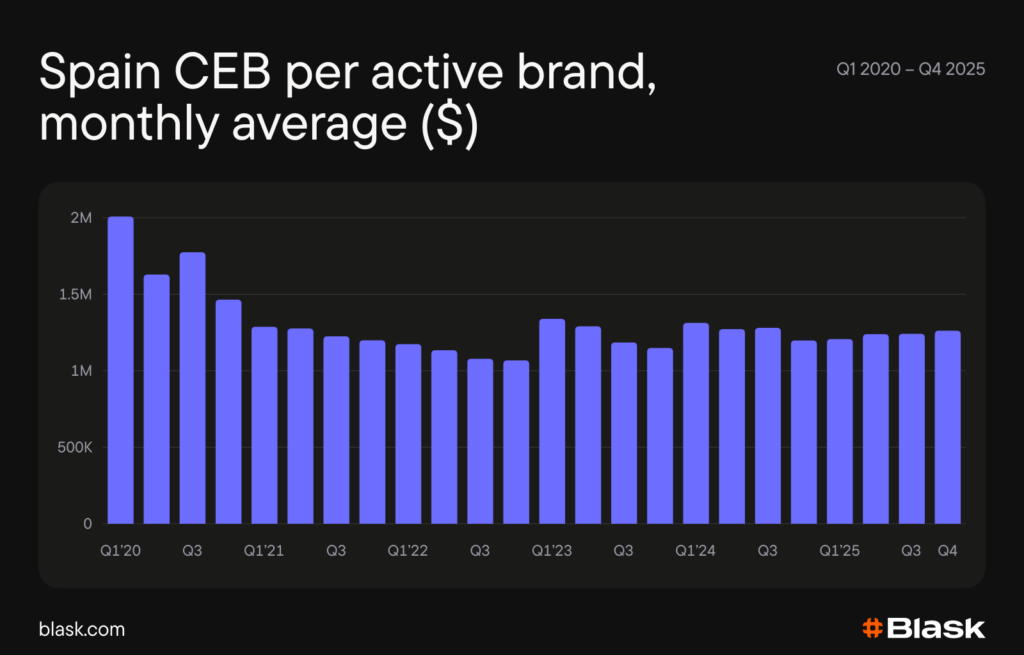

Digital attention in Spain has declined rather than held steady. Blask Index — a composite measure of market engagement — peaked in early 2021, then fell sharply and stabilized at a markedly lower level. Over the past six years, the number of active brands tripled and total monthly CEB roughly doubled, but CEB per brand has remained largely flat since early 2021.

Market leadership has fragmented. Bet365’s share of BAP fell from over 50% in early 2020 to around 18% by the end of 2025. Half of the market is now controlled by six brands — still concentrated, but significantly less dominant than in 2020.

All these trends confirm the broader narrative: the reported rise in total GGR reflects growth in the user base, not increased spend per player or per brand. With digital attention stable at a lower level and more operators competing, the market is being split into increasingly narrow shares.

Rules and results

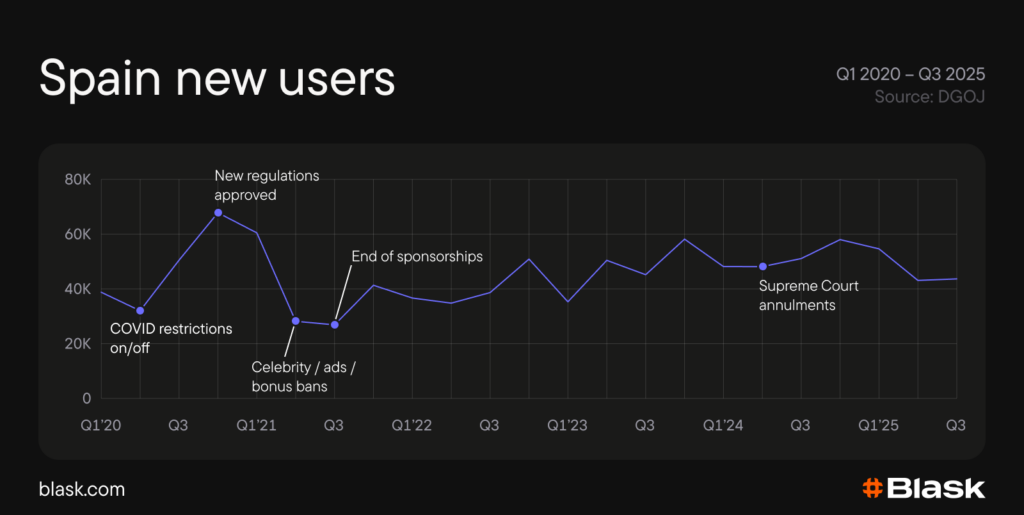

The maturation of Spain’s market unfolded under some of Europe’s tightest rules. The first wave of severe restrictions arrived in spring 2020, banning most iGaming advertising, promotions, and bonuses for several months. The aim was to limit problem gambling during lockdowns.

Those rules were reset in late 2020. Rolling out through 2021, they confined TV, radio, and streaming ads to the 1:00–5:00 AM window, barred celebrity endorsements, and phased out sports sponsorships. Crucially, the bonus promotions were restricted to verified customers with at least 30 days’ history.

In 2024, the Supreme Court partially annulled several ad and promo provisions reopening sign‑up offers. The ruling was published in May 2024, leading to a clear uptick in acquisition activity.

The restrictions were designed to limit the scale and visibility of iGaming advertising and promotions. They aimed to protect younger adults from marketing pressure and reduce aggressive inducements. At the same time, they sought to reinforce responsible‑gambling messaging across the market.

Official quarterly data show sign‑ups fell sharply in spring–summer 2021 and stayed subdued into early 2022. They rebuilt from late 2022 to a peak at the end of 2024, then softened again in 2025.

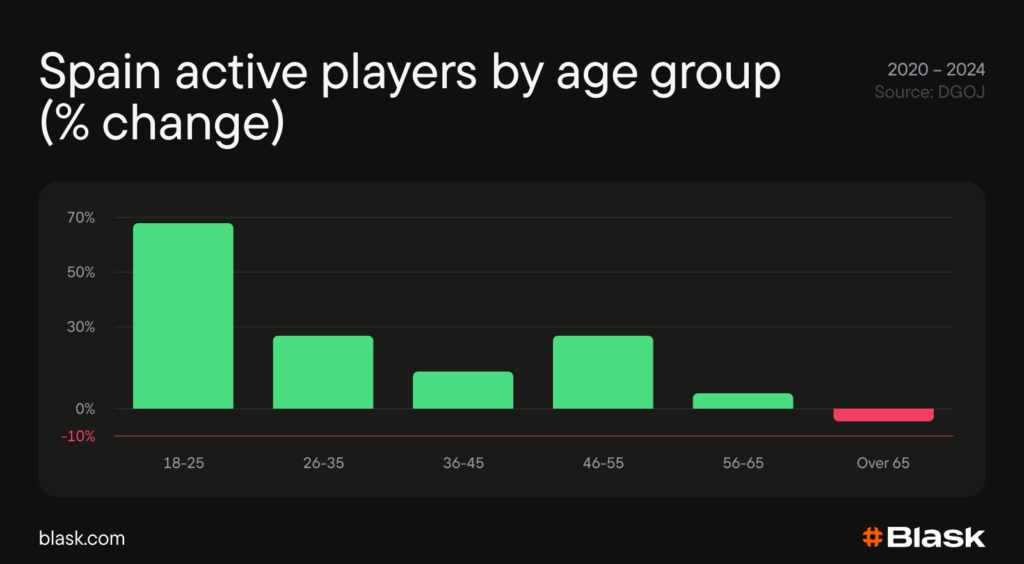

On the other hand, the policy failed to achieve its aim regarding young adults. The share of active players aged 18–25 rose from about 27% in 2020 to around 34% in 2024. The largest year‑on‑year increase came in 2024, when bonuses were reinstated, but a significant jump also occurred in 2022, when restrictions were at their peak.

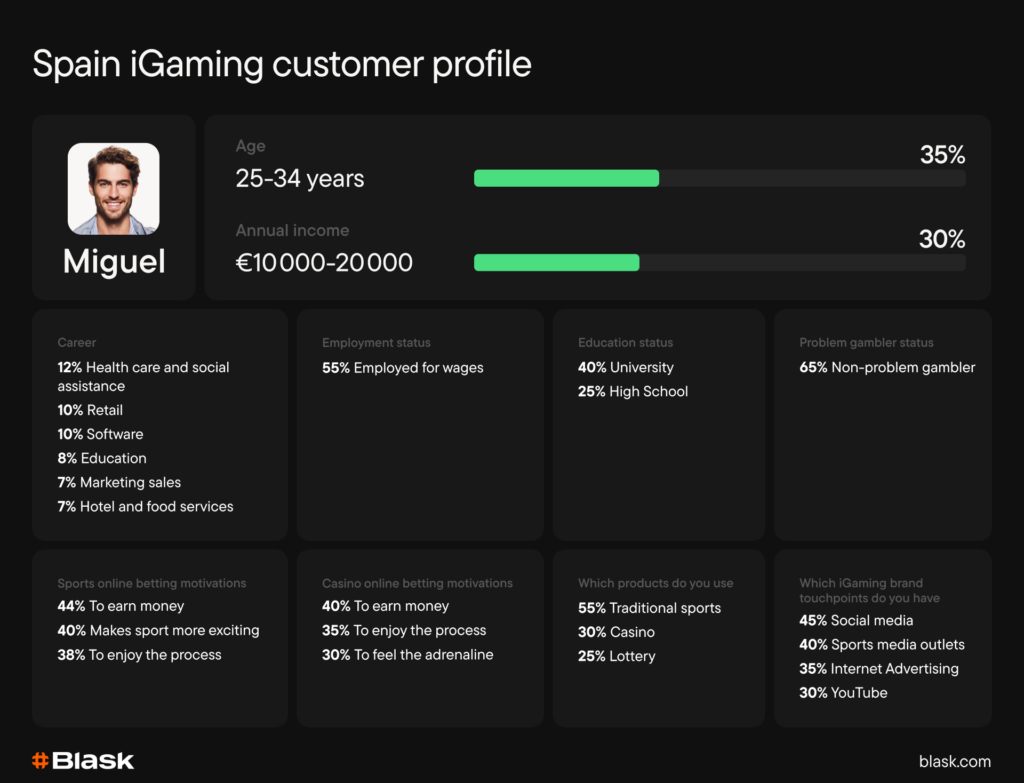

The audience

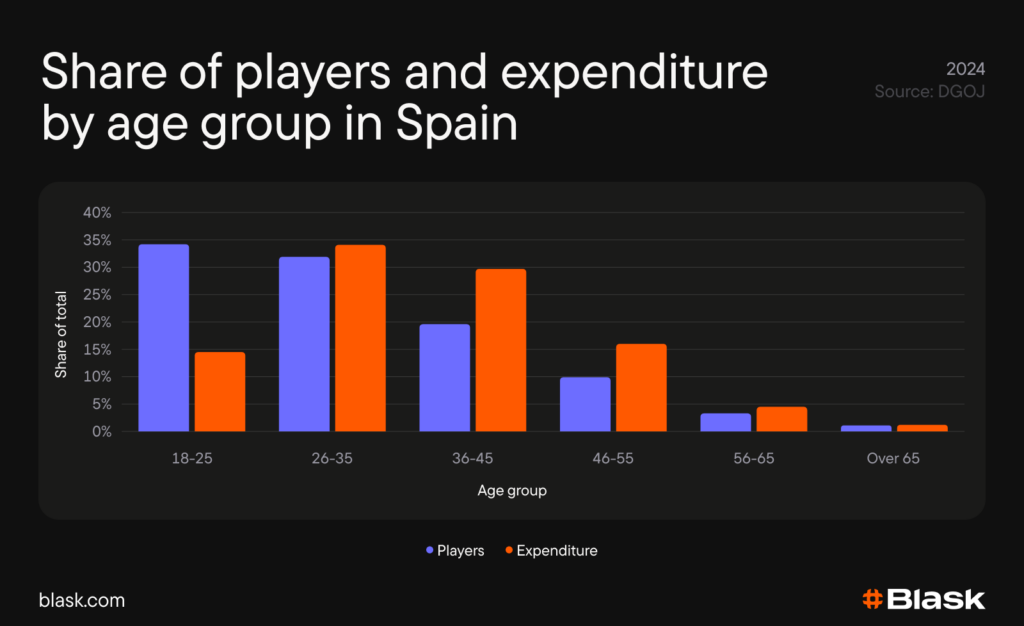

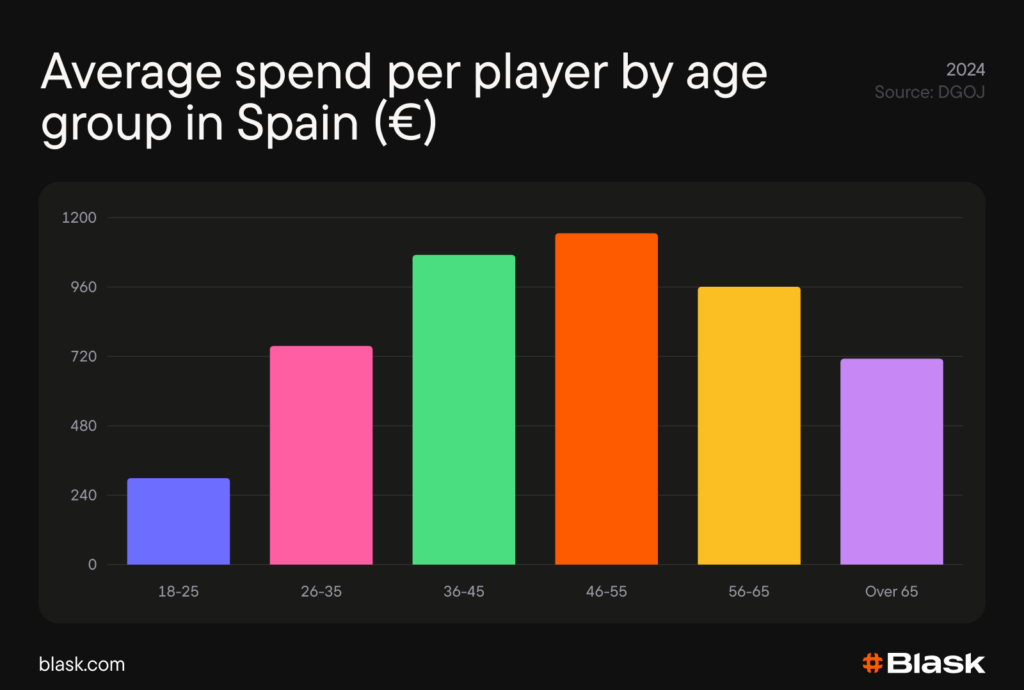

Although the 18–25 cohort is the largest by headcount, it is modest in spend. In 2024, this group generated about 15% of total expenditure, with an average annual outlay of roughly €300 per player. Spending rises with age. The market’s breadth skews young, while its depth lies with older cohorts.

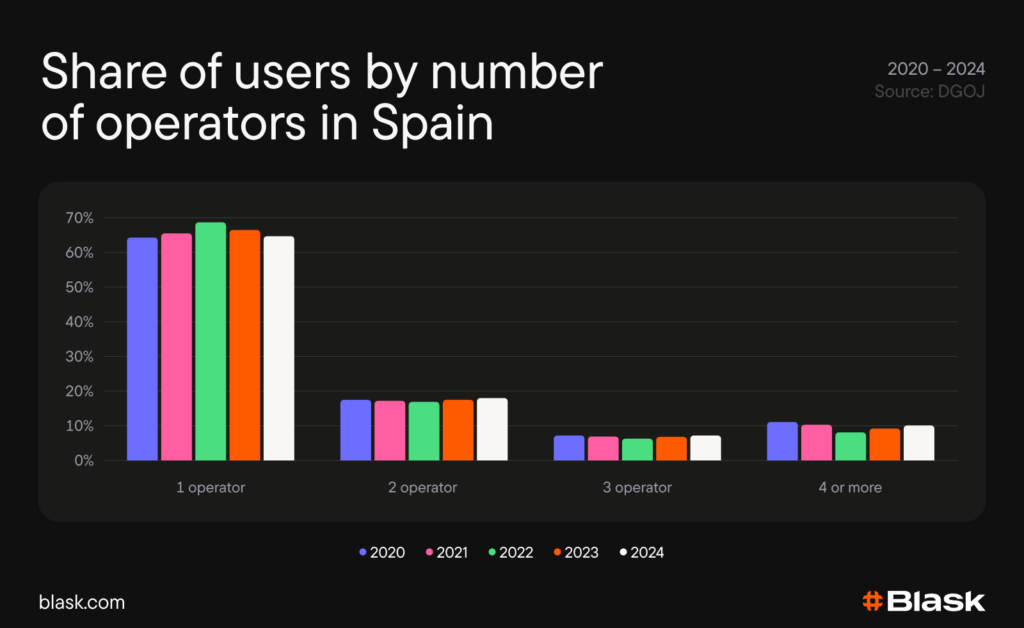

Operator loyalty is high. About two‑thirds of active players used only one operator in 2024, and the pattern has been broadly stable over the years, suggesting limited multi‑operator behaviour despite increased brand crowding.

Product behaviour is gradually diversifying. The share of players who were active in only one product type fell from just over 60% in 2020 to around 50% in 2024, with a growing number participating in both sports betting and casino.

Blask’s audience snapshots portray a mainstream, wage‑earning base with mid incomes, tilted toward 18–34 and reached chiefly via social and sports media. Occupations cluster in services, retail, and tech/marketing, with most respondents educated to university or college level.

In practice, it is a broad, digital‑first cohort whose spend is thinly spread. This pattern is consistent with official per‑player averages, high single‑operator loyalty, and only a slow move toward multi‑product engagement.

Breadth into depth

Spain enters 2026 with rules intact and growth fueled by volume, not spend per player. Competition is fierce, attention is split. With the bonus ban averted, the market’s challenge shifts from acquisition to retention — turning casual players into committed ones.