- Updated:

- Published:

USA: in a league of its own

Blask data reveals the real scale of the US iGaming market.

Blask tracks almost every meaningful iGaming market in the world. With the latest addition of the US and Canada, coverage now extends to 126 countries. Their combined CEB (Competitive Earning Baseline, a projected revenue calculated by Blask) exceeded $200B in 2025.

The largest tracked market is the US, accounting for nearly 40% of the global total. Several states on their own produce more CEB in 2025 than recognised iGaming countries, and four out of five largest global brands by CEB are operating primarily in the US.

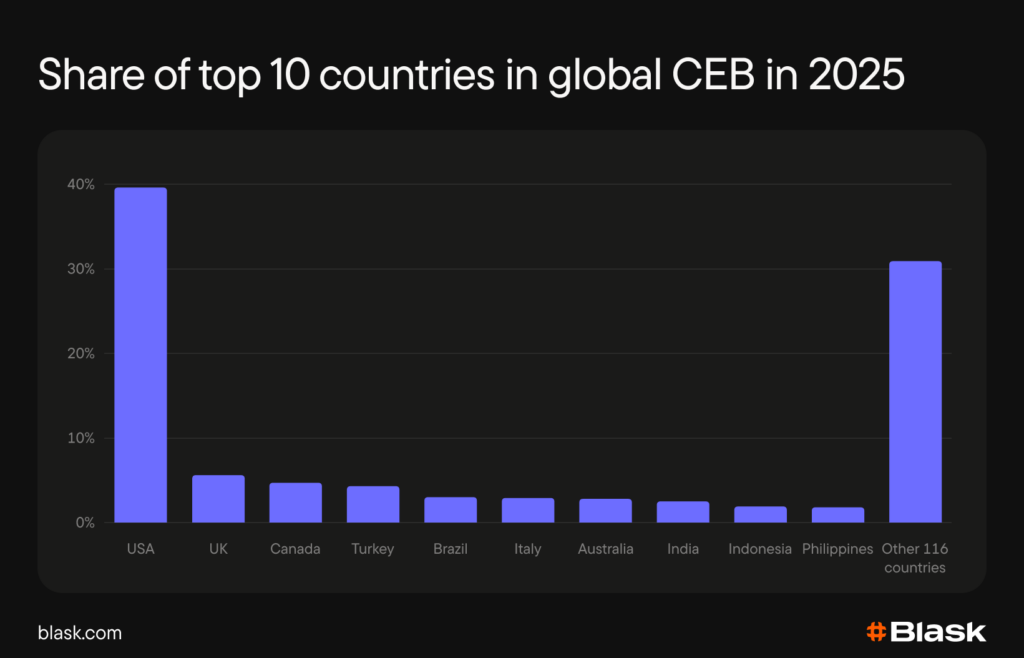

The US outweighs other markets from top 10 combined

The easiest way to comprehend the scale of the US iGaming market is to compare it with other countries.

According to Blask data, the top 10 countries generated around 70% of global CEB in 2025. And the US alone contributed almost three-fifths of that amount.

In terms of CEB the US iGaming market in 2025 was 7 times the size of the UK, which holds second position in the global ranking. Compared to Canada, which occupies third place, the US market is over 8 times larger.

The US iGaming market is by far the largest globally by CEB, and data at the state level is just as striking.

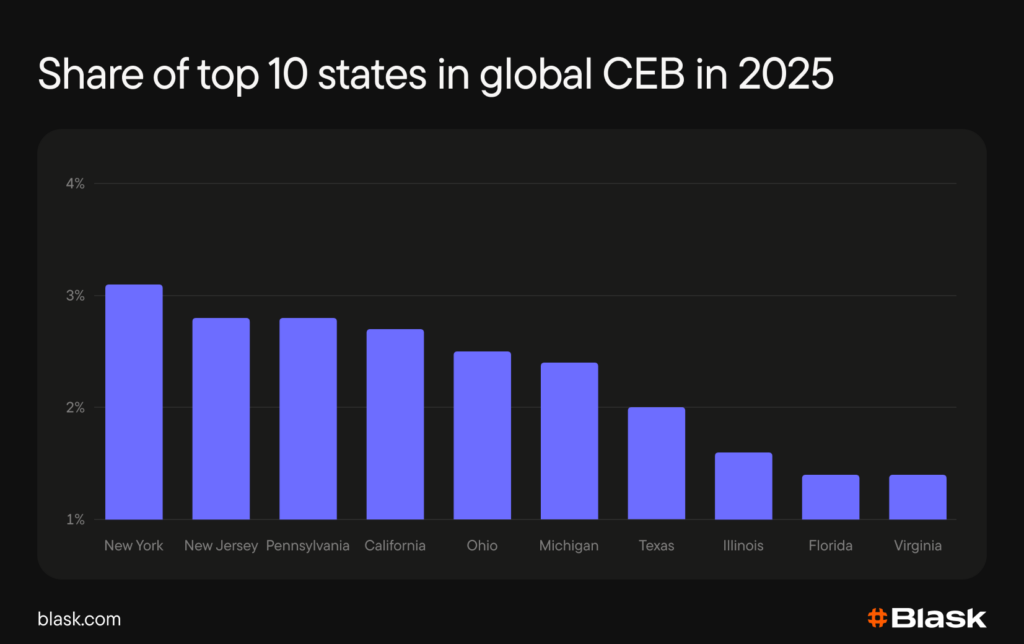

Top states rival entire countries

According to Blask data, some states on their own produced more CEB in 2025 than acknowledged top iGaming countries.

For example, the CEB of New York State’s iGaming market was bigger than Brazil’s, while New Jersey, Pennsylvania and California each accounted for more CEB than India.

The top 10 states accounted for almost 23% of global CEB in 2025. That is more than the five largest countries excluding the US combined.

Treated as separate markets, four US states would rank in the top 10 globally by CEB. But not all of these states lead in user demand.

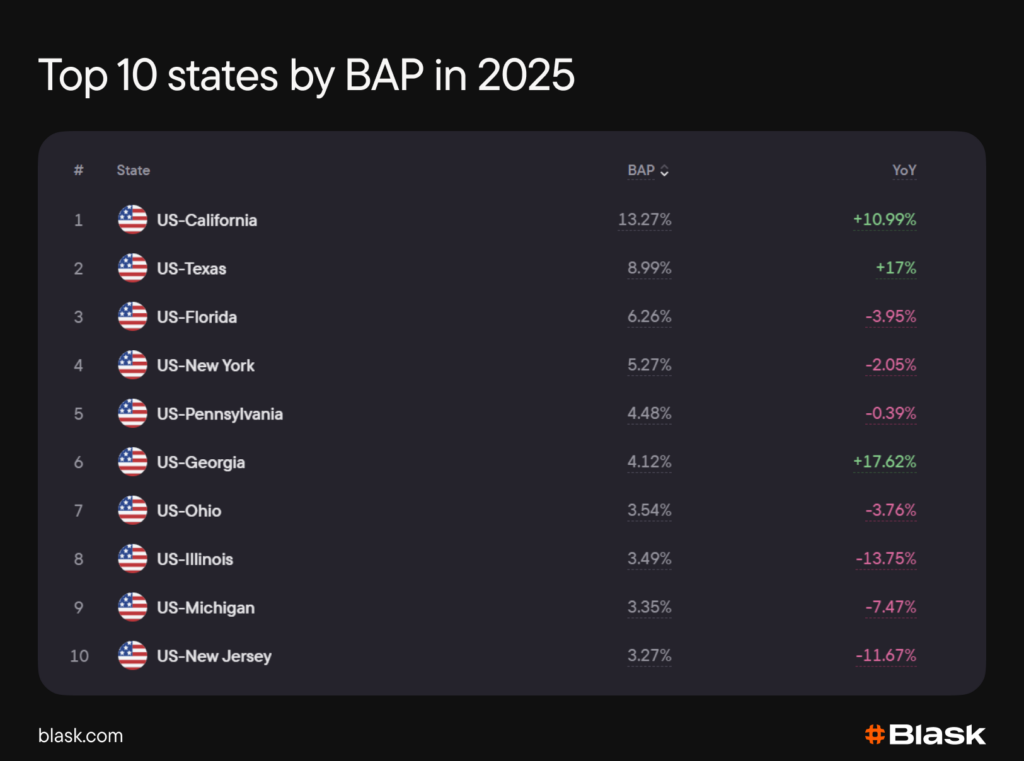

State-level rankings by revenue and demand do not match

Unlike the CEB ranking, state-by-state rankings by BAP (Brand’s Accumulated Power, the share of the country’s Blask Index, which represent user demand for iGaming) are more consistent with population numbers.

The top three states by BAP are California, Texas and Florida. Combined they held 28.5% of the country’s Blask Index in 2025, while the top 10 accounted for over 56%.

Among the 10 largest states by BAP, Georgia posted the strongest Blask Index growth in 2025, while Illinois fell hardest. Among all 50 states, Delaware led year-over-year Blask Index growth with 48.7%, and North Carolina registered the steepest decline at −21.1%.

The total US Blask Index is not the largest in the world. Several countries rank higher, including those with significantly smaller populations, such as the UK and Italy. And there are other metrics where the US is far from leading.

Fewer brands, stronger performance

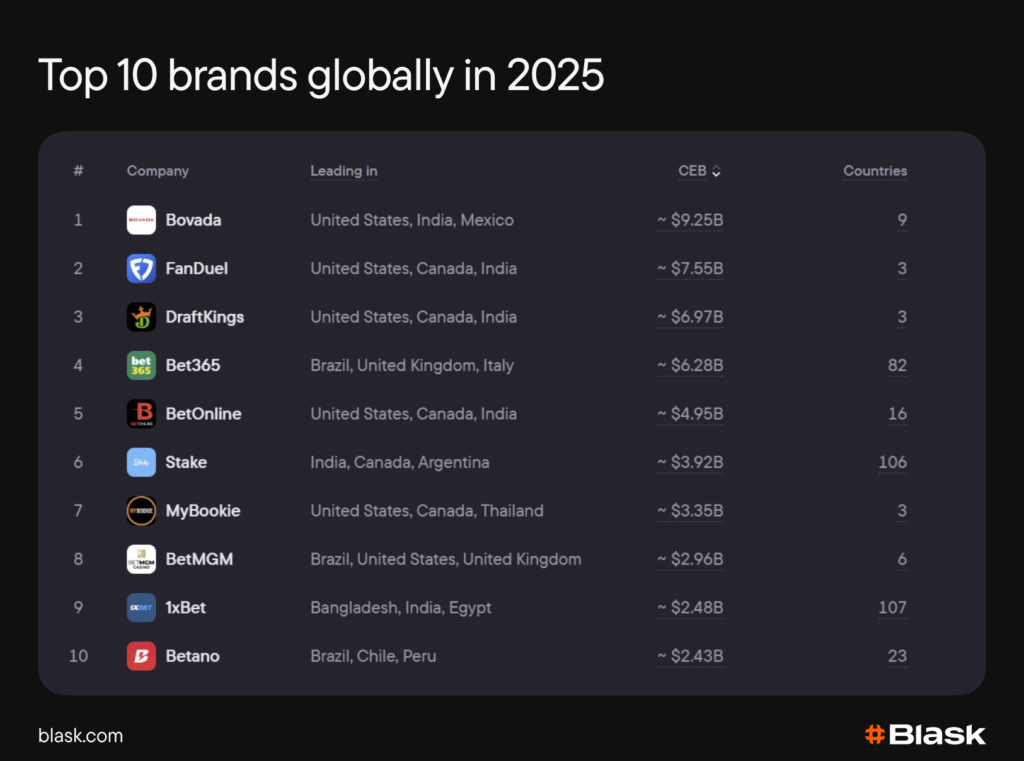

The US ranks only third by number of active iGaming brands, behind Brazil and India. Yet, each of the five largest iGaming brands globally (by CEB) operates in the USA.

For four of them the US market is where almost all CEB came from in 2025. The exception is bet365, ranked fourth globally, where the US accounted for just 12% of total CEB. The largest brand by CEB that was not present in the US in 2025 is Stake, which is ranked sixth globally.

Among the top 5 global brands (by CEB) with a US presence, three hold domestic licences — FanDuel, DraftKings and bet365. The remaining two — Bovada and BetOnline — operate offshore.

The full onshore-offshore breakdown is far more complex and offshore biased than this split suggests, and forms the centerpiece of the special report by Blask.

Get the full picture

The US iGaming market is not just the largest in the world by CEB — it is also the most complicated. The onshore-offshore split, state-by-state regulation landscape and dynamics, the rise of prediction markets, and much more — all in Blask’s US and Canada iGaming report.