The UK gambling market is heading for a major consolidation move. Evoke, the company behind the legacy brands William Hill and 888, is set to be acquired in an all-share takeover.

Bally’s Intralot has agreed to acquire Evoke, the holding company behind William Hill, 888 and Mr Green, in a recommended all-share deal worth approximately $325M (£243.1M). Evoke shareholders will receive 0.537 Intralot shares for each Evoke share held, valuing the company at $0.70 per share. The deal also includes a partial cash alternative capped at $157M.

Evoke’s board approved the deal only on the sixth attempt, after earlier proposals started at $0.43 per share. The merger is expected to close around the turn of 2026 and 2027. Management expects to generate $241M (£180M) in cost and capex savings within two years.

For Bally’s Intralot, formed in October 2025 after Greek lottery operator Intralot acquired Bally’s International Interactive, the deal marks a strategic breakthrough. The group had limited weight in the UK, while Evoke’s assets bring onshore licences and a powerful search footprint that closes that gap.

The valuation paradox: buying declining demand for long-term expansion

Together, Evoke’s UK portfolio generates around $1.4B in CEB, making the $325M deal value look unusually modest. Bally’s Intralot is paying for ready-made distribution, established brands and access to millions of players in the world’s largest iGaming market.

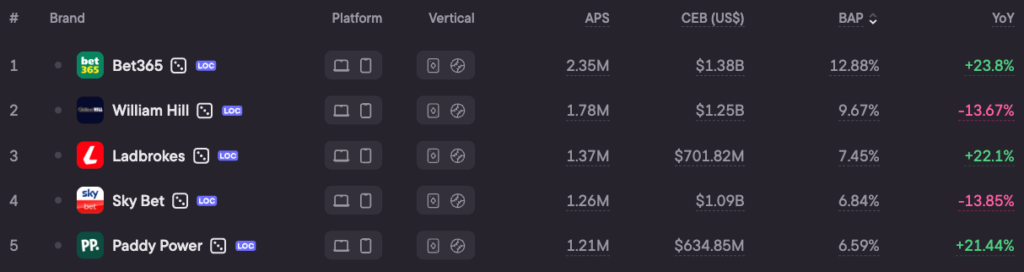

The low price is explained by the weakening of Evoke’s digital dominance. Over the year, William Hill’s UK Blask Index fell by 11.35%, while its BAP share declined from 13.21% in April 2025 to 8.54% in April 2026. While William Hill and Sky Bet lost audience share, rivals including Bet365, Ladbrokes, Paddy Power and Betfred strengthened their positions.

The group is following a familiar home-market playbook: in May 2026, it secured a licence in Rhode Island by relying on its local land-based casino base. Now the same logic is being applied to William Hill’s fading but still monumental demand, which the group will try to stabilise and monetise.

A strategic gambit in the UK market

The modest $325M equity cheque and William Hill’s weakening trajectory may create the impression of a falling asset being acquired cheaply. However, the scale of lender support and the much higher enterprise value of $2.94B point to a longer-term calculation.

For Bally’s Intralot, this is a tactical land grab: by acquiring onshore licenses and a huge search footprint, the US group instantly becomes one of the heavyweights in the UK market, betting that synergies and aggressive marketing can restore the strength of its legacy brands.