Market intelligence from Blask maps Italy’s demand cycles onto a regulatory year that’s reshaping European iGaming’s biggest market

Italy has crossed a threshold that would have seemed improbable a decade ago. In 2025, it overtook the United Kingdom to become Europe’s largest regulated gambling market by total revenue, recording €21.5 billion in gross gambling revenue and accounting for 41.4 percent of the entire European online casino market. Underneath that headline number lies a demand engine that runs on a single fuel: the football calendar.

Market data from Blask, which tracks the relative intensity of iGaming search and engagement across geographies via Blask Index, reveals the mechanics behind Italy’s revenue cycle with unusual precision.

The insight is not that Italy bets on football — that has been known since the first Totocalcio coupon. The insight is that the demand curve follows the sporting calendar with near-mechanical fidelity, creating identifiable peaks and troughs that any operator, affiliate, or content team can plan around.

Europe’s Biggest Market Just Got More Concentrated

Before examining the seasonality data, the structural context matters. November 13, 2025 marked the go-live date for Italy’s new licensing regime, implemented under Legislative Decree No. 41/2024 and overseen by the Agenzia delle Dogane e dei Monopoli (ADM).

The overhaul reduced the active operator pool from 93 applicants in the previous round to 52 concessions held by just 46 operators — each of whom paid €7 million for a nine-year license, with ongoing obligations including a 3% annual fee on net gaming revenue, mandatory ISO certifications, and real-time data-access requirements for the ADM.

The immediate market read in December 2025 was mixed but instructive: online casino spending rose 18.4 percent year-on-year to €333.7 million as players migrated quickly to new domains.

Online sports betting, however, dropped 18.8 percent to €126.6 million, reflecting the friction of platform migration and reactivation during a month with structurally weak sporting fixtures. Lottomatica held its ground with 31.14 percent of online casino market share; Sisal followed at 12.10 percent.

January 2026 told a different story.

Italy’s fixed-odds sports betting market posted a record gross win of just under €330 million — a 28 percent year-on-year increase — with online accounting for 62 percent of the total at €205 million. According to H2 Gambling Capital, the full-year 2026 forecast stands at €2.94 billion in gross win, up nine percent from €2.71 billion in 2025. The December dip, H2 noted, was structural noise amplifying the month-on-month comparison; the underlying trend had not broken.

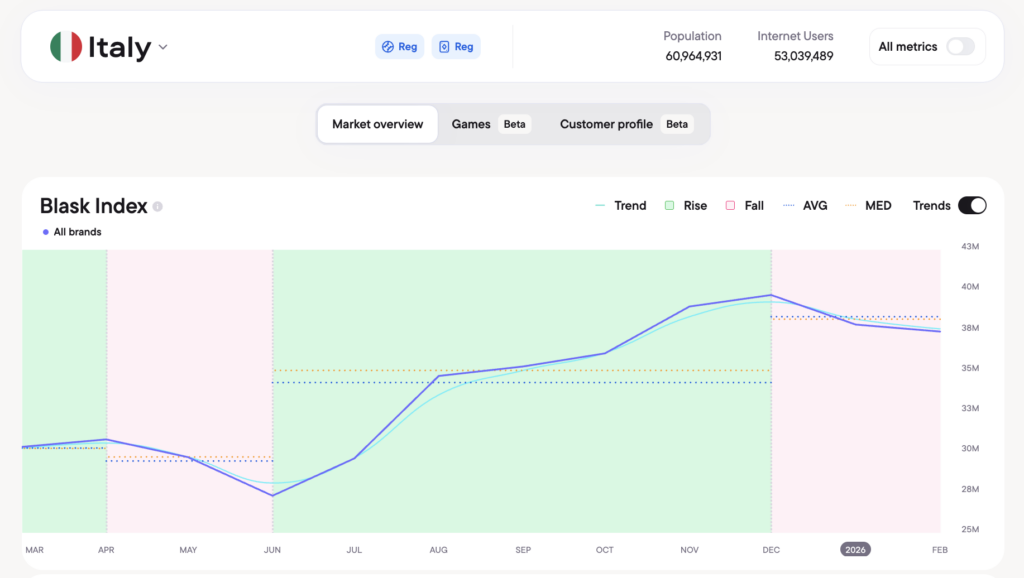

That dynamic — a December lull followed by a sharp January rebound — is precisely what Blask’s seasonality data predicts. And it has very little to do with regulation.

The Shape of a Year

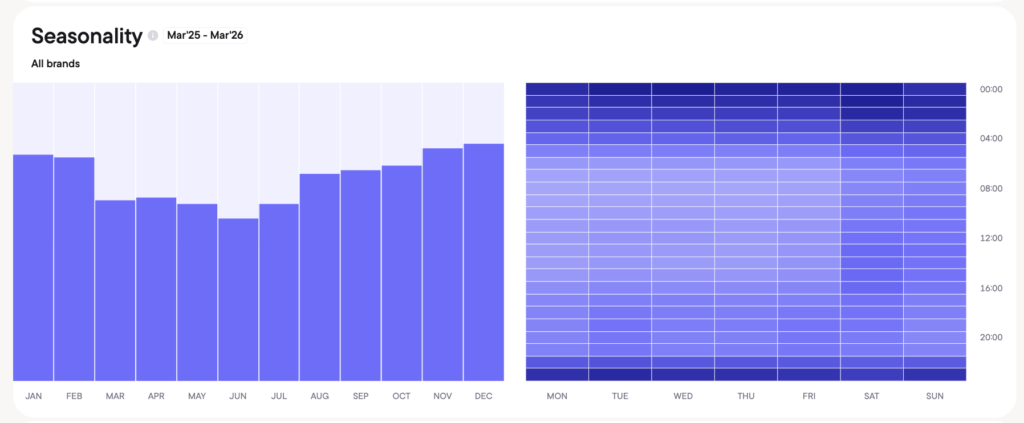

Blask Index data for Italy over the past 12 months traces a shape the company describes as a “U-recovery into an autumn staircase.”

From February through June 2025, demand softened by roughly seven percent, forming a spring trough that coincides with the mid-season plateau of Serie A — a phase when the title race is still unresolved but novelty has worn off. From there, the index reversed into a steady climb that accelerated into autumn, ultimately lifting the trend line by more than 35 percent from its seasonal low to the winter peak before stabilizing into early 2026.

The two strongest spikes in the annual cycle align with events that any football fan could name without prompting.

August 23, 2025 — the opening matchday of the 2025-26 Serie A season. After the summer lull, pent-up demand met the return of domestic football, generating a sharp reactivation spike driven by accumulated anticipation and heavy media coverage. In the context of Italy’s regulated market, this was the moment when newly licensed platforms, some operating under new brands following the ADM’s single-brand-per-license requirement, met a player base hungry for football content after months of relative inactivity.

December 13, 2025 — Matchday 15 of Serie A. Landing deep inside what Blask describes as the “high-intensity winter corridor,” this date coincided with dense fixture cycles across domestic and European competitions, mid-season positioning narratives, and a title race that Italian television had been building for weeks. The date also overlapped with Festa di Santa Lucia, extending leisure time in parts of northern Italy and marginally reinforcing weekend activity.

These are not random spikes. They sit at the intersection of fixture density, media intensity, and cultural moment — and they repeat, year on year, with enough consistency to inform planning cycles.

Summer Is a Structural Lull, Not a Warning Sign

Italy’s most repeatable trough runs from June through early August. The cause is blunt: Serie A is on summer break, European competitions have concluded, and the market reverts to friendlies and minor fixtures that generate a fraction of the betting interest of competitive play.

That data point is worth contextualizing against the broader market. Total online stakes in Italy reached €77.85 billion in 2025, with €3.3 billion in player spending — a record for the casino, poker, and bingo segments. Football betting alone generated €16.1 billion in turnover in 2024, an eightfold increase since 2006. State fiscal revenues from football betting hit €401.6 million in 2024, an all-time high.

These are not numbers generated evenly across 12 months. The summer dip — genuine, structural, and predictable — does not indicate demand collapse. It indicates that Italy’s wagering market is running on the same schedule as the Champions League group stages.

That connection has hardened in recent years. The UEFA Champions League’s reformed format, which replaced the previous group stage structure beginning with the 2024-25 season, is reported to have boosted operator betting revenue by up to 40 percent in the competition’s opening phase, according to industry analysis. The simultaneous fixture rounds under the new league phase created what one sportsbook called “a micro-betting surge opportunity” at scale. For the Italian market — home to clubs such as Inter Milan, Juventus, and AC Milan that routinely participate deep into the knockout rounds — this structural uplift has direct revenue implications across the October-to-March window.

Inside the Week: Where Liquidity Actually Lives

The Blask data becomes most operationally useful at sub-weekly resolution. Italy shows a football-anchored weekly structure, but the pattern is more textured than a simple “Saturday spike” narrative.

Saturday remains the most consistently elevated day of the week, with activity building through Friday evening and carrying into Sunday. The highest-liquidity single window is overnight Friday into Saturday — a slot where pre-weekend anticipation, live fixtures, and extended leisure time overlap to generate what Blask describes as the week’s peak concentration.

What the heatmap also reveals, however, is a persistence of evening engagement across non-match weekdays. Rather than sharp isolated spikes on fixture days, the data shows repeated daily surges concentrated in late-evening local time — a pattern consistent with a habit loop layered on top of sports-driven triggers. Users return at consistent hours regardless of weekday; sporting events amplify rather than create that demand.

This is relevant for operators building CRM and content schedules. A communications strategy anchored solely to fixture dates leaves value on the table during the mid-week off-peak windows where retention activity can operate at lower competitive noise levels.

The Operator Landscape Entering the Hot Season

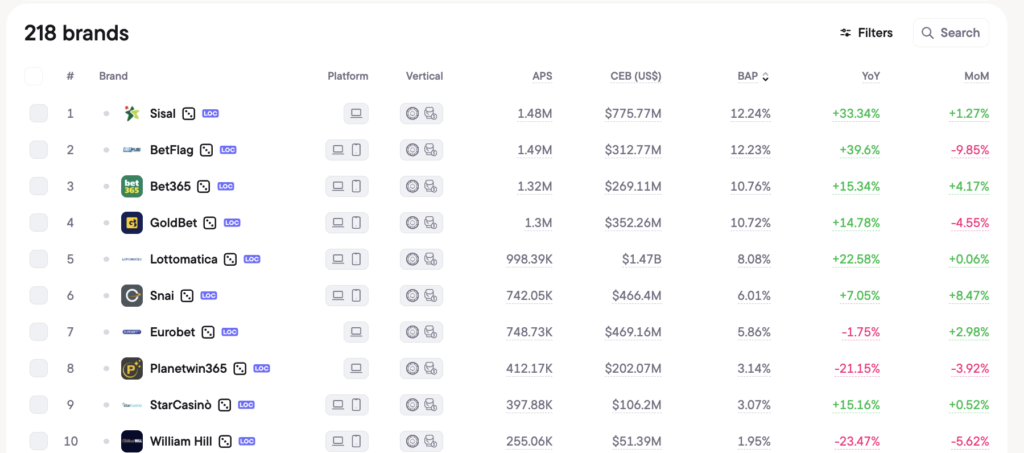

Italy’s competitive structure heading into the spring 2026 fixture stretch is the most consolidated it has been since legalization. Lottomatica, which reported full-year 2025 revenues of €2.26 billion — up 12 percent year-on-year — now holds 31.3 percent of total online market share, with online sports betting share at 32.4 percent. Group CEO Guglielmo Angelozzi described 2026 as “a year of further consolidation and evolution,” with 2026 revenue guidance set between €2.39 billion and €2.46 billion.

Flutter Entertainment completed its €2.3 billion acquisition of Snaitech in April 2025, combining Snai’s retail footprint of 2,047 gaming points with Flutter’s Sisal, PokerStars, and Betfair brands. The group targeted at least €70 million in operating cost synergies within three years of closing. Flutter’s combined Italian market share is now estimated at approximately 30 percent, positioning the company as the primary challenger to Lottomatica.

Entain, operating through Eurobet, holds approximately 10.6 percent of Italian market share, with particular strength in the retail-to-online acquisition model: 56 percent of Eurobet’s online revenue derives from its retail customer base. The company notes Italy represents its third-largest market globally by net gaming revenue contribution.

Betway and Unibet exited ahead of the November 2025 transition, choosing not to apply under the new framework. Their departure has concentrated available market share among the 46 surviving licensees — most of whom are now entering the period of highest structural demand on the Italian calendar.

What the Pattern Implies

The convergence of Blask’s seasonality data with Italy’s regulatory and market context produces a specific picture for anyone deploying capital in or around the Italian market in 2026.

The autumn window — Serie A’s full cadence layered with Champions League knockout rounds and international windows — is the period of maximum organic demand. It is also the period when the licensing regime’s 9-year structure gives incumbents the most confidence to invest. The summer trough is foreseeable and temporary; the late-August reactivation spike has arrived on schedule for multiple consecutive years.

Italy’s online betting penetration sits at 55 percent. Its online gaming penetration is 26 percent. The gap between those two figures is one of the largest in Europe, and it sits directly in the demand corridor that Blask’s weekly heatmap identifies as persistent evening engagement — not driven exclusively by sports fixtures, but amplified by them.

Europe’s biggest gambling market runs on football time. The clocks are already ticking toward Serie A’s summer restart.