iGaming in the CIS

The CIS is one of the most underrated regions in global iGaming. It contains a top-5 world market by Blask's CEB ranking, two more in the top 40, and a cluster of fast-growing markets that most operators still treat as an afterthought. Eleven countries, one shared cultural and linguistic legacy — and almost nothing else in common when it comes to market size, regulation, or competitive dynamics.

What the data shows

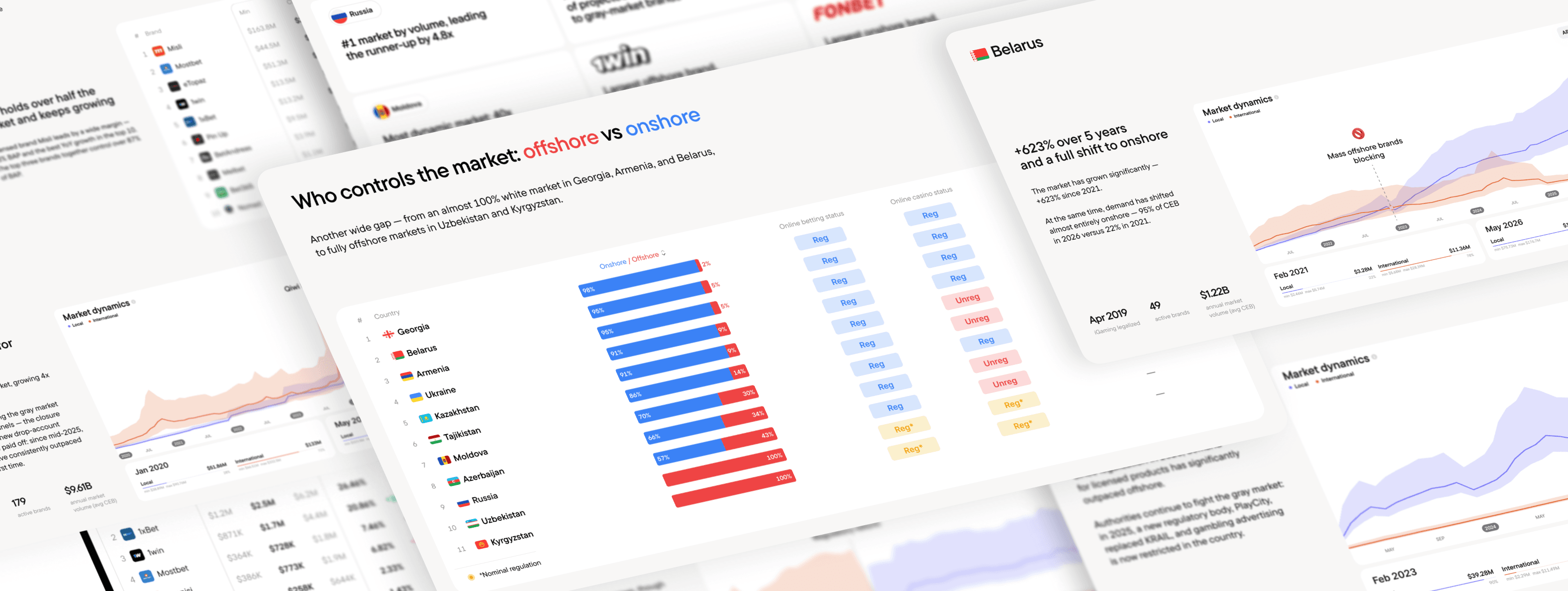

Scale varies by a factor of 1000 — from Russia's $9.61B in projected annual revenue down to Kyrgyzstan's $9.4M. Regulatory status runs the full spectrum, from long-established licensed frameworks to markets that are banned outright or legal on paper with no licenses issued. Offshore share follows: Georgia and Armenia operate at 95%+ onshore while Uzbekistan and Kyrgyzstan are fully gray. And in four of the eleven markets, a single brand controls more than half of all projected revenue.

Who should read this

Operators and investors assessing entry points across CIS markets, where regulatory status, offshore share, and brand concentration vary more than anywhere else in the world. Suppliers and affiliates mapping which brands are actually taking share and which are losing ground. Anyone who works across the post-Soviet space and needs data beyond aggregate estimates.

What's inside

Market-level breakdowns for all eleven countries covering Blask Index dynamics, CEB with min/avg/max ranges, active brand counts, and onshore/offshore splits; brand rankings with BAP and year-over-year CEB for the top 10 operators in each market; regulatory timelines and the measurable impact of key legislative events on market structure; and a closing summary of the standout records across the region — fastest growth, highest concentration, largest offshore share.

Get Access

Please enter your information to download the asset