After the tax cliff: UK iGaming under 40% Remote Gaming Duty

On 1 April 2026, the UK doubled its Remote Gaming Duty from 21% to 40% — the largest shift in British online gambling economics since the duty was introduced. This report uses Blask data to examine what actually happened in May 2026, the first month that offered a clean read on how the market behaves under the new regime.

What the data shows

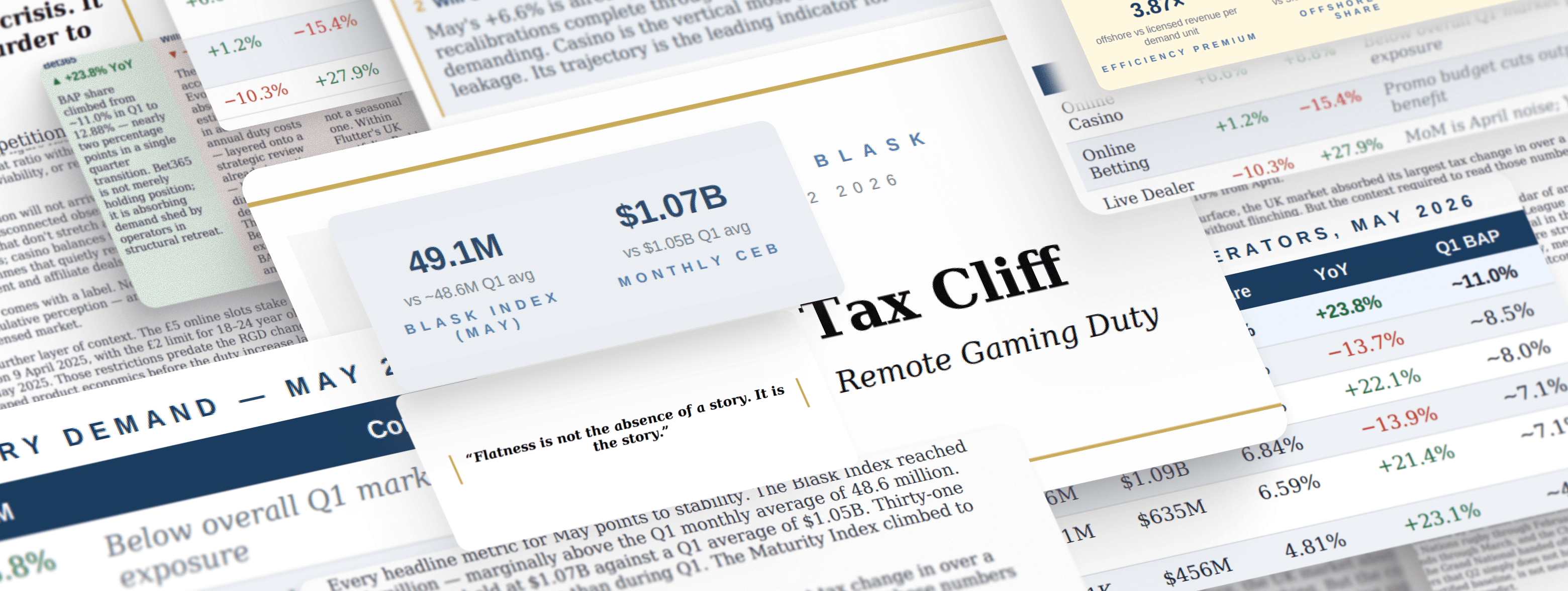

Blask Index held above its Q1 average in May — but Q1 was fortified by Six Nations, Champions League knockouts, Cheltenham, and the Grand National. At the brand level, demand is consolidating rather than growing broadly. One operator is absorbing share at a pace that raises structural questions about market concentration.

Online Casino is trailing the overall market's Q1 pace — and it's the vertical most directly exposed to the new duty rate. The offshore efficiency premium, meanwhile, has held stable for twelve months and shows no sign of narrowing as licensed player value compresses.

What's inside

Aggregate market metrics with context, brand-level rankings for the top operators, category breakdowns for Casino, Betting, and Live Dealer, an analysis of the offshore efficiency gap, and three forward questions that Q2 data will either confirm or deny.

Who should read this

Operators assessing how the 40% RGD is reshaping competitive dynamics and where demand is actually moving. Affiliates and media tracking which brands are gaining ground and which are losing it. Anyone who needs to read past the aggregate stability and understand what is happening at the brand and category level.

Get Access

Please enter your information to download the asset