The Alberta Gaming, Liquor and Cannabis Commission (AGLC) published a list of confirmed registrants for the new online gaming market, which includes 30 B2C brands.

Alberta’s licensed market will launch with a strong Ontario link. Of the 30 consumer-facing brands listed for Alberta, 25 already have experience in that environment, which remains the main reference point for Alberta’s model.

The AGLC list also gives registered operators an early advertising advantage. After Google updated its gambling ads policy for Alberta, listed brands can start preparing paid acquisition, positioning and launch campaigns before the market opens on July 13.

Alberta is a country-sized iGaming market

Blask data shows the province’s 2025 CEB reached $1.34B, placing it between Bangladesh and Portugal by market size. It is smaller than Ontario by population, but its iGaming market is already large enough to be compared with national markets. Today, that market has only one licensed operator, Play Alberta. It is already a sizable local brand, but most of Alberta’s revenue potential sits offshore.

Ontario demand leaders enter Alberta

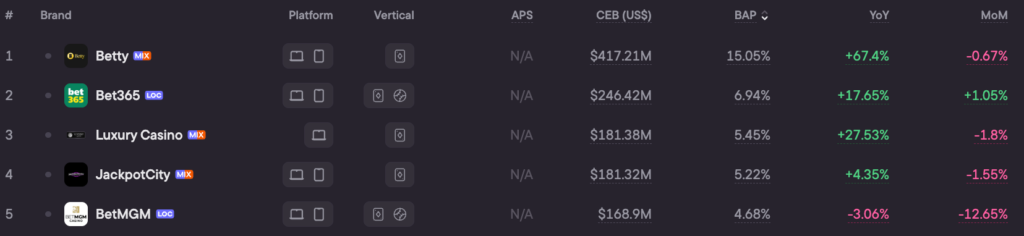

The AGLC list gives the first view of how Alberta’s licensed iGaming field may look at launch. It includes the province’s current monopoly operator, Play Alberta, and 25 brands that already operate in Ontario, Canada’s first open regulated iGaming market. Ontario data over the latest 12-month period gives the clearest read on several incoming brands: Betty ranks #1 by BAP, JackpotCity ranks #4 and BetMGM ranks #5.

US-linked operators sit lower in Ontario demand

The list also includes major US-linked names, including FanDuel, DraftKings, Betway, BetRivers, PointsBet and theScore. Ontario BAP data shows that US-linked scale has not automatically translated into top local demand in Canada.

Over the latest 12-month period, FanDuel ranked #11 in Ontario, with 2.27% BAP and $85.14M CEB. Betway ranked #14, followed by theScore at #15, DraftKings at #19, Sports Interaction at #20, BetRivers at #23 and PointsBet at #30.

Alberta’s local and lower-visibility entrants

The AGLC list is not made only of Ontario-tested operators. It also includes Alberta-linked names.

Play Alberta enters as the province’s existing regulated platform, while Pure Casino and River Cree iGaming bring local casino groups into the launch field.

Several applicants are harder to read before launch: Albertix has limited public visibility, Grizzly’s Quest does not appear as an Ontario iGO directory brand, and Pala / Stardust Casino needs careful treatment because the company and consumer-facing brand may not be the same.

The offshore question remains

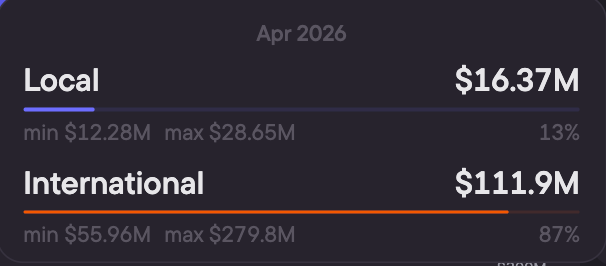

Alberta’s regulated market will be built by shifting existing offshore demand into the licensed channel. Blask data shows that offshore brands now account for 87% of Alberta CEB.

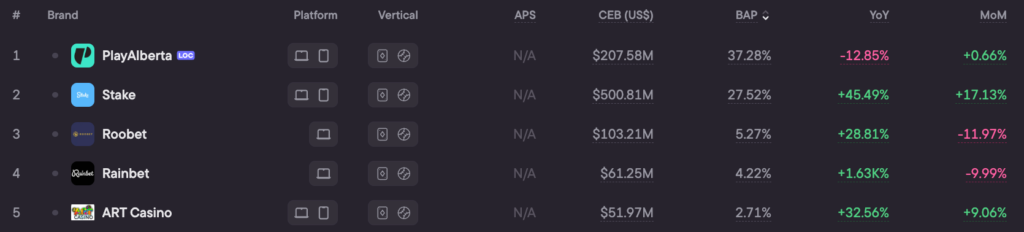

That means Alberta’s first licensed operators will compete on two fronts. They will compete with Play Alberta and each other inside the regulated market. They will also compete against offshore brands that already hold a large share of the province’s revenue potential. Stake is the clearest example of that offshore pressure. The brand is not on the AGLC list, but Blask data for the latest year shows it generated $500.8M in Alberta CEB, more than 2.4 times Play Alberta’s $207.6M.

What the launch will test

Alberta’s first regulated cycle will test whether Ontario-proven brands and local operators can redirect existing offshore demand into the licensed channel.

The launch field is strong by Canadian standards. The harder part is the starting demand map: Alberta already has a large active market, and most of its revenue potential sits outside the regulated perimeter.