Nigeria’s Supreme Court ended the federal model for gambling regulation in November 2024. Eighteen months later, Blask data shows a market that is still growing, but no longer works as a single regulatory space.

The ruling voided the National Lottery Act and handed gambling oversight to Nigeria’s 36 states after a 16-year legal dispute. As a result, the country’s gambling market has split into three different operating zones: southern states with established local frameworks, FSGRN member states using a reciprocity licensing model, and northern states where gambling remains prohibited under Sharia law.

The market split

The Supreme Court ruling did not replace federal oversight with one national model. It split Nigeria into three operating zones.

- Active south. Several states — Lagos, Rivers, Delta, Oyo, and others — had been regulating gambling long before November 2024. When the Supreme Court ruling came, the Lagos State Lotteries and Gaming Authority treated it as confirmation of powers it was already exercising.

- FSGRN cluster. 22 states formed the Federation of State Gaming Regulators of Nigeria (FSGRN) and in May 2025 launched a Subnational Reciprocity Licensing Framework — a universal certificate covering all member states in one application. The system works for online gaming; for offline, each state still negotiates separately.

- Closed north. Nine Muslim-majority states prohibit gambling under Sharia law. Pew Research estimates Nigeria’s Muslim population at about 120M people, or 56% of the country. A significant part of that audience lives in regions where licensed gambling operators cannot legally enter the market.

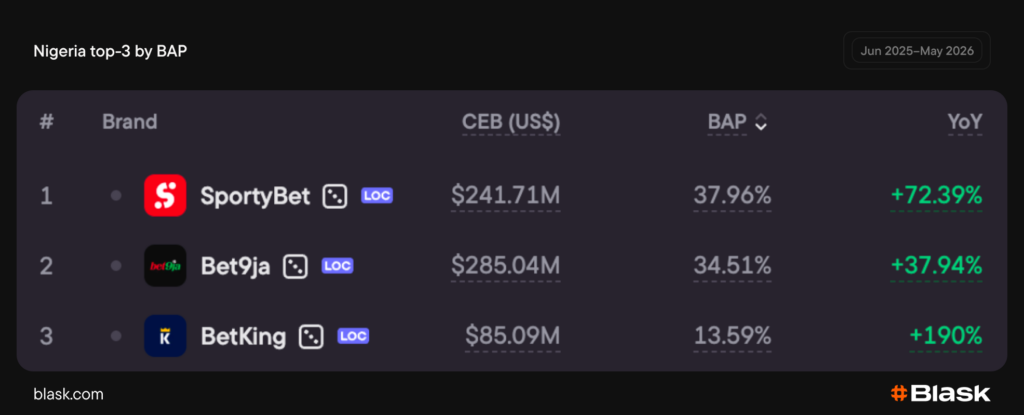

Nigeria’s demand sits with local operators

According to Blask, Nigeria ranks 41st among global iGaming markets. Over the last 12 months, Blask tracked 175 brands in the country, while CEB reached $746.46M.

The market is almost entirely local. In May 2026, Nigerian brands generated 98% of CEB, while international brands accounted for only 2%.

The top three brands also show how concentrated the market is. SportyBet, Bet9ja and BetKing together control 86.06% of branded demand in Nigeria, leaving the rest of the market highly fragmented. International brands remain marginal: 1xBet, Betway and Betano together do not even reach 2.1% BAP.

One country, three gambling rulebooks

The Supreme Court ruling replaced one federal framework with three operating realities. For operators, this means the south is open and active, the FSGRN cluster is accessible through a single reciprocity licence, and the north is off the table. The main unresolved issue is jurisdictional overlap in online gambling — and until that is clarified, cross-border player access remains a legal grey zone.