- Updated:

- Published:

Fastest growing online casino markets to watch in 2026

Where player demand grew the fastest in 2025 — and what the data says about why.

The global gambling industry generated $643.74 billion in revenue in 2025, continuing a five-year growth streak. But that growth was far from evenly distributed. While mature markets in Western Europe and North America moved incrementally, four markets — the Philippines, Nigeria, Argentina, and Mexico — delivered demand growth that clearly stood apart. Together, they offer an early read on the forces likely to shape iGaming industry trends 2026.

Blask tracks brand-level demand across more than 120+ markets using the Blask Index, an AI-enhanced demand signal built from search activity across iGaming operators. It measures behavioral demand — searches, brand interactions, account-related activity — before it converts to bets or revenue. That makes it a leading indicator: operators see what’s moving before quarterly financials confirm it.

The metrics used in this article — Acquisition Power Score (APS) and Competitive Earning Baseline (CEB) — are derived from that signal. Each is calculated as a range (min–avg–max), because market conditions create a spectrum of plausible outcomes. The averages appear in the text; full ranges are included where the detail matters.

Read more: What is Blask Index?

Philippines: demand doubled in a single year

Any ranking of the top iGaming markets 2026 will have to account for the Philippines, which produced some of the most striking growth figures seen anywhere in 2025.

Acquisition Power Score (APS) — Blask’s benchmark for how many new customers a brand’s current market position should generate — reached 14.4M for the full year (range: 9.7M–28.5M). In 2024, it was 7.1M. That’s a 103% jump year-over-year.

Competitive Earning Baseline (CEB) — Blask’s revenue benchmark built from brand strength and competitive positioning, not operator-reported financials — grew to $3.66B ($2.68B–$6.60B range), up from $2.63B in 2024. A 39% gain in revenue potential in a market that was already one of Asia’s largest.

The driver is structural. PAGCOR, the Philippines’ gaming regulator, reported PHP 69 billion in regulated online gaming revenue for 2025, and the sector generated $1.2 billion in fees in the first seven months alone. PAGCOR’s net income soared 49% as enforcement against unlicensed operators pushed players toward regulated platforms.

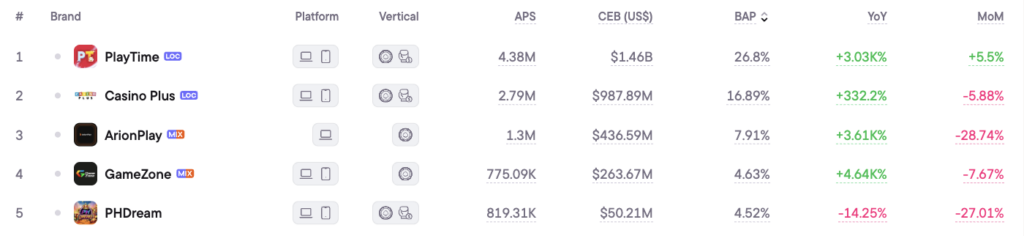

The brand-level data reflects this compression. PlayTime, the market’s top brand by Blask demand, posted 3% YoY Blask Index growth. GameZone, ranked fourth, grew 4,64%. These aren’t niche operators catching a short-term wave. They’re capturing players who previously sat outside the regulated market entirely.

With 212 active brands tracked in the Philippines, it’s also one of the more competitive markets in the region — operators who moved early are already consolidating share while latecomers fight for what remains.

Nigeria: Africa’s standout market

Nigeria grew 26.7% by CEB to $633.6M ($472.6M–$1.12B range) in 2025, up from $500M the year before. APS grew 44.3%, from 8.0M to 11.6M (range: 8.6M–20.4M).

For context, Nigeria’s total gambling market has been projected at $3.63 billion for 2025 when accounting for the full market including informal operators. Blask’s CEB measures the segment where brands generate trackable consumer demand — the credible floor of regulated activity.

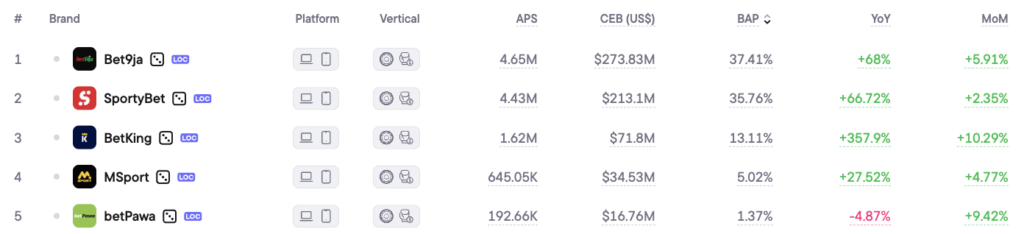

The market is concentrated.

Bet9ja and SportyBet together account for the majority of Blask demand in Nigeria. Bet9ja grew 53.3% year-over-year by Blask Index; SportyBet 46.1%. The more revealing figure is BetKing, which grew 244.1% over the same period — evidence that mid-tier operators are capturing share as the market expands beyond the top two.

Nigeria’s growth correlates directly with mobile infrastructure and demographics. Sports betting has become embedded in the informal economy for millions of Nigerians, driving volume that established Western markets can’t replicate. The acquisition numbers reflect a market still in expansion, not saturation.

Latin America: Argentina and Mexico

Latin America produced two of the clearest growth stories in 2025, driven by different mechanisms.

Argentina

Argentina grew 25.2% by CEB to $1.44B ($846M–$3.21B range), with APS up 24.1% to 5.96M (range: 4.1M–11.7M). The story is regulatory expansion.

Buenos Aires Province moved to regulate online gambling through most of 2025, with biometric identification requirements for licensed platforms added in December. Provincial licensing is gradually formalizing what was already a high-volume market.

Betano’s 329.6% year-over-year Blask Index growth in Argentina illustrates how quickly new entrants can capture share in a market still defining its structure. Betsson, the market leader, grew a steadier 30%. Bet365 grew just 0.1% — evidence that scale alone doesn’t guarantee growth when focused challengers move faster.

Mexico

Mexico posted APS growth of 41.7% — from 2.5M to 3.5M (range: 2.5M–6.4M) — while CEB grew at a more measured 14.3% to $1.89B ($1.39B–$3.40B range).

The gap between strong acquisition numbers and moderate revenue growth suggests Mexico is still in a user-acquisition phase. Operators are building player bases faster than revenues scale, which is typical of markets in early consolidation.

Caliente, the market’s top brand, grew 26.5% year-over-year by Blask demand. BetMexico, the second-ranked operator, grew 68.3% — a faster trajectory from a smaller base.

What separates the fastest growing markets

The four markets above share structural characteristics that set them apart from mature ones.

- Regulatory movement. Each market either completed, advanced, or expanded its regulatory framework during 2024–2025. Regulation doesn’t suppress demand — it compresses it from informal to formal operators, making it measurable and compressible into licensed channels.

- Mobile-first player bases. In Nigeria and the Philippines, the majority of iGaming activity runs through mobile apps. Acquisition costs are lower, but so are the barriers to switching. Operators who build strong brand recognition early have a structural advantage.

- Room ahead. The Philippines at $3.66B CEB and Nigeria at $634M are large in absolute terms but small relative to population size. India, for comparison, sits at $5.20B CEB with a population more than 10× Nigeria’s. The headroom in these markets is a long way from closed.

Brazil: what post-regulation normalization looks like

Brazil offers one of the clearest counterpoints in the debate over which iGaming markets are growing fastest in 2026. It was the most anticipated market of 2024, attracting heavy operator investment ahead of federal regulation taking effect in January 2025. CEB for Brazil stood at $7.21B in 2024. In 2025, it fell to $5.08B — a 29.5% contraction.

Player volume barely moved (APS grew just 3.2%, from 76.8M to 79.2M), but demand intensity dropped sharply as operators normalized marketing spend following the regulatory rush.

Brazil’s market is not contracting — it’s recalibrating after a speculative run-up. Operators who invested heavily in 2024 are now competing in a defined regulatory environment with clearer rules and tighter margin assumptions.

This pattern — demand spike before regulation, contraction after — is worth watching in Argentina and the Philippines as their frameworks mature.

Markets to watch in 2026

The 2025 data points in different directions for each market heading into 2026. Blask Q1 2026 figures (January–March) show which stories are still running and which have already turned.

- Philippines: the momentum hasn’t stopped.

Q1 2026 CEB reached $1.73B — compared to $382M in Q1 2025. That’s a 353% year-over-year gain in the first quarter alone. Most markets that double in a year spend the next 12 months digesting. The Philippines is still accelerating. The catalyst is ongoing PAGCOR enforcement: every offshore operator removed from the market transfers its player base to licensed brands, and that process isn’t finished. The market to watch most closely in 2026. - Brazil: looking for the floor.

Brazil’s regulated market launched in January 2025 and contracted 29.5% for the year. Q1 2026 CEB came in at $871M, down 33% from Q1 2025’s $1.31B. The post-regulation compression is still running. Industry analysts tracking Brazil’s regulated market expect stabilization once operators stop competing on marketing spend and shift to retention. When Brazil finds its floor — most likely H2 2026 — it will still be one of the top five iGaming markets globally by volume. The APS pool is 13.9M players in Q1 2026 alone. - West Africa: Nigeria holds, the frontier expands.

Nigeria’s Q1 2026 growth rate has moderated from 2025’s 44% APS run to a more measured +14%. But that’s still growth in a market with 236 million people and rising mobile penetration. The more interesting 2026 question is the next tier: Ghana and Angola are seeing early-stage demand signals that resemble Nigeria’s 2022–2023 profile. Sub-Saharan Africa’s regulated market structure is shifting from a Nigeria-only story to a regional one. - Mexico and Argentina: consolidation over growth.

Both markets show flat-to-declining Q1 2026 numbers compared to Q1 2025. Mexico CEB is down 16% quarter-over-quarter; Argentina is down 11%. The 2025 acquisition surge in both markets ran ahead of monetization, and the correction is visible. The brands that built strong positions in 2025 — Betano in Argentina, BetMexico in Mexico — are better positioned to hold share than to grow it this year. Consolidation is the story, not expansion.

Read also: European iGaming market outlook 2026: where demand is growing

For operators evaluating market entry

The fastest growing online casino markets in 2025 are not the largest. They’re the ones where regulatory clarity is increasing, mobile infrastructure is maturing, and demand is shifting from informal to licensed operators.

Blask tracks all four of these markets in real time: 212 active brands in the Philippines, 184 in Nigeria, 167 in Argentina, and 143 in Mexico. The Blask Index gives operators a demand signal that updates before quarterly earnings confirm what moved.