- Updated:

- Published:

What Is KYC (Know Your Customer)

Know Your Customer procedure is a mandatory part of interaction with online platforms because of several reasons, including the detection of money laundering. This article brings the answer on what is KYC, why it matters, and how it works.

What Is KYC (Know Your Customer)

Search traffic still starts with what is KYC, yet the real answer sits in regulation, data architecture, and risk control. It is a working system, not a one-time form.

In practice, know your customer means proving identity, understanding activity, and judging risk before service begins. It also continues after onboarding through updates and monitoring.

Why KYC Matters

For regulated firms, this procedure is the front gate for fraud prevention, sanctions control, and account integrity. Weak checks create legal, financial, and reputational damage.

Preventing Money Laundering and Fraud

Criminal abuse usually appears through fake identities, mule accounts, stolen documents, or hidden beneficial owners. Strong controls reduce that room fast:

- identity proof,

- beneficial owner checks,

- transaction review.

Regulatory Compliance

Strong KYC compliance links onboarding, beneficial ownership, monitoring, and suspicious activity controls. In the US, FinCEN lists all four as core CDD duties.

Building Customer Trust

When the know your customer policy works smoothly, onboarding feels safer. That helps serious brands look reliable, not sloppy.

KYC vs AML vs CDD vs EDD: Key Distinctions

The search phrase what is KYC often gets mixed with nearby terms. They overlap, but they do different jobs.

| Criteria | KYC (Know Your Customer) | AML (Anti-Money Laundering) | CDD (Customer Due Diligence) | EDD (Enhanced Due Diligence) |

| Core Definition | The operating layer focused on identifying the customer and setting a risk profile. | The general legal and compliance system designed to prevent financial crimes. | The process of developing a customer profile based on data, activities, and ownership. | A deeper level of verification used specifically when the risk assessment increases. |

| Primary Scope | Proving identity, understanding the relationship, and judging initial risk. | Includes surveillance, reporting, screening, oversight, and global prevention. | Determining the exact level of risk involved based on identity and intentions. | It’s a key process in investigating high-risk factors, complex structures, and irregular activities. |

| Typical Triggers | Initiated before service begins (onboarding) and maintained via updates. | Continuous regulatory mandate for all regulated firms and financial industries. | Standard baseline requirement during the onboarding and customer profile setup. | Triggered by PEP status, high-risk jurisdictions, or complex corporate layers. |

| Action Items | Collecting full legal name, DOB, address, and verified government ID data. | Suspicious activity reporting, global screening, and transaction monitoring. | Analyzing expected account activity, business reasons, and beneficial ownership. | Deep-dive source of funds (SoF) checks, closer scrutiny, and rigorous verification. |

KYC (Know Your Customer)

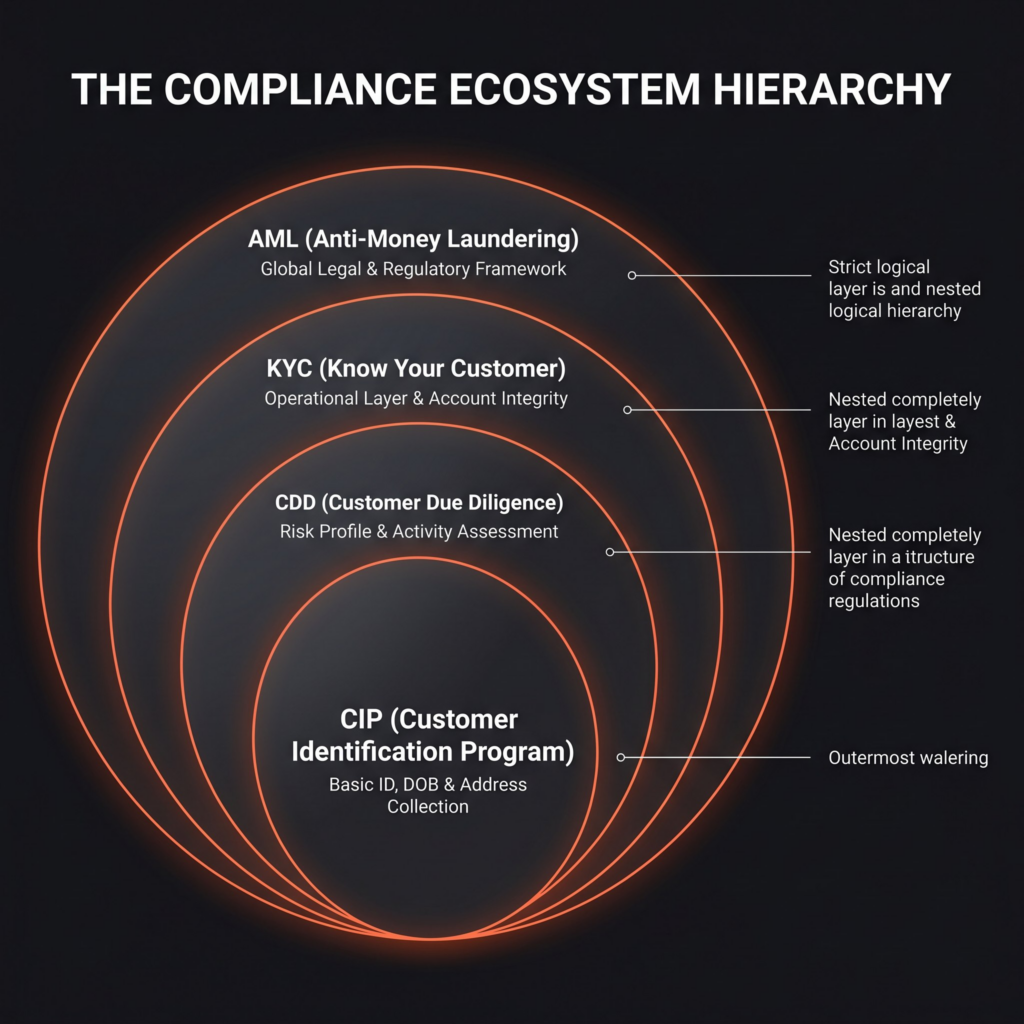

The KYC process focuses on identifying the customer, understanding the relationship, and setting a usable risk profile. It is the operating layer of due diligence.

AML (Anti-Money-Laundering)

AML refers to the general legal and compliance system. This includes surveillance, reporting, screening, oversight, and prevention of financial crimes.

CDD (Customer Due Diligence)

The CDD process helps develop the customer profile based on his identification information, activities, ownership, and intentions. This helps the operator determine the risk involved.

EDD (Enhanced Due Diligence)

EDD becomes relevant where risk increases. Common examples include being a PEP, dealing with high-risk jurisdictions, having complicated ownership structures, and irregular transactions.

The Three Pillars of KYC

Most compliance frameworks still rely on three fundamentals. These are identification, due diligence, and review. Together, these pillars form the KYC process, which operates as a core component of broader Anti-money laundering procedures.

Customer Identification Program (CIP)

CIP collects core identity data before access begins. It usually includes:

- full legal name,

- date of birth,

- address,

- government ID data.

Customer Due Diligence (CDD)

CDD will ask why the customer was here, what is expected to happen, and if the ownership seems clean. This will result in more accurate decision-making in the future.

Ongoing Monitoring

KYC doesn’t end after onboarding. The risk should be re-evaluated whenever behavior changes, new information comes in, or threshold levels are reached.

KYC Verification Process Step-by-Step

Programs should have a logical flow. Evidence is at the forefront, risk logic comes second, and monitoring continues throughout the process.

Document Collection (ID, Proof of Address)

Good KYC verification starts with reliable identity and address evidence. Passports, driving licences, and utility bills remain common proof.

Identity Verification (Manual and Biometric)

Today, KYC verification often blends manual review with biometrics, face matching, OCR, and selfie checks. That cuts fraud and speeds approval.

Risk Assessment and Scoring

Risk scoring turns raw data into action. Typical inputs include:

- geography,

- product type,

- transaction size,

- occupation,

- ownership structure.

Sanctions and PEP Screening

Screening entails identifying an individual or entity from the sanctioned, watch-listed, and PEP lists. Matches often trigger additional scrutiny.

Types of KYC

The delivery models depend on the market, product, and regulators, with the principle being the same, but the channel differing.

eKYC (Electronic)

Regarding digital onboarding, eKYC consolidates document uploading, database matching, consent, and identification into an electronic format process, which is more efficient than paper processing.

Video KYC (vKYC)

Video KYC brings an element of human touch. This can be used where stronger identification is needed.

Aadhaar-Based KYC (India)

In India, Aadhaar-based transactions can pass on details like name, age, gender, photograph, and address with consent. These might be considered adequate for KYC purposes.

Paper-Based KYC

Paper KYC continues to exist in legacy systems and lower tech settings. These processes are slower and more cumbersome.

KYC in iGaming and Online Gambling

High transaction speed, remote access, bonus abuse, and age risk make KYC in online gambling stricter than many people expect. Gaming checks are about safety, crime, and consumer protection.

Why iGaming Has Stricter KYC

Access to remote gambling sites should exclude minors, players who have self-excluded themselves, fraudsters, and criminals involved with dirty money. This brings the process of establishing someone’s identity forward in the process.

| Criteria | Casino with KYC | Casino without KYC |

| Licensing & Legal Status | Fully compliant. Eligible for reputable licenses (for example, UKGC). Operates legally in regulated markets. | Unregulated or “Gray” status. High risk of domain blocking by authorities and blacklisting by tier-1 infrastructure providers. |

| Payment Gateway Options | Access to premium fiat channels (Visa/Mastercard, Apple Pay, Google Pay, local bank transfers) alongside crypto. | Restricted mostly to cryptocurrency or high-risk, unstable P2P networks. Frequent payment processing drops. |

| Game & Software Providers | Direct integration with top-tier providers (NetEnt, Evolution, Pragmatic Play) that mandate strict compliance. | Limited game selection; often restricted to copycat (“scripted”) slots or niche providers with lower compliance bars. |

| Bonus Abuse & Fraud | Protected. Multi-accounting and bot farms are caught during verification, ensuring marketing budgets go to real players. | Highly vulnerable. Target for massive automated sign-ups to exploit free spins and welcome offers (Bonus Abuse). |

| Chargeback Risk | Minimal. Verified player identities and linked payment ownership make it incredibly hard for players to fraudulently dispute losses with banks. | Severe risk. Players can easily file for “friendly fraud” chargebacks, claiming their card was stolen, leaving the casino with heavy losses. |

| Responsible Gambling (RG) | Integrated self-exclusion programs (e.g., GAMSTOP), age verification blocks, and triggers to detect problem gambling. | No oversight. High risk of heavy regulatory fines or reputational damage for admitting minors or self-excluded players. |

| Player LTV & VIP Retention | High LTV. Serious highrollers and VIPs prefer secure, licensed platforms where their large funds and payouts are legally protected. | Low LTV. The audience is primarily composed of low-stakes anonymous players, churn-risk users, or bad actors. |

KYC at Registration vs Withdrawal

The stance held by the United Kingdom on the issue is that operators need to establish one’s identity prior to gambling and not at the time of withdrawal, especially when it could be done beforehand.

Source of Funds (SoF) Checks

SoF checks whether spending matches the player profile. Reviews may involve:

- bank statements,

- income patterns,

- affordability indicators.

Responsible Gambling KYC Triggers

Risk assessments could be initiated following rapid deposits, strange losses, issues with hardware, or any indicators of financial trouble. Both compliance and responsible gambling tend to converge at this point.

KYC Across Industries

The same control architecture will be seen in other industries, but the catalysts and indicators will differ. The risks associated with products are an integral part of this process.

Banking and Fintech

KYC in banking and fintech industries relies on customer onboarding, beneficial ownership verification, and ongoing monitoring as the standard baseline. While a faster user experience is important, strict documentation and regulatory compliance remain non-negotiable.

Crypto and Web3

Crypto companies need to protect themselves from risks like wallets, sanction threats, and international mobility. As such, transaction screening is just as important as identity verification.

iGaming and Sportsbooks

The iGaming industry uses identity screening, age verification, payment screening, behavioral monitoring, and bonus misuse detection.

Insurance and Lending

Lenders and insurers use due diligence to stop fraud, synthetic identities, and misrepresented applications. Risk data shapes pricing and approval quality.

KYC Regulations Around the World

Across jurisdictions, what is KYC changes in detail, but the core idea stays stable. The key process remains universal.

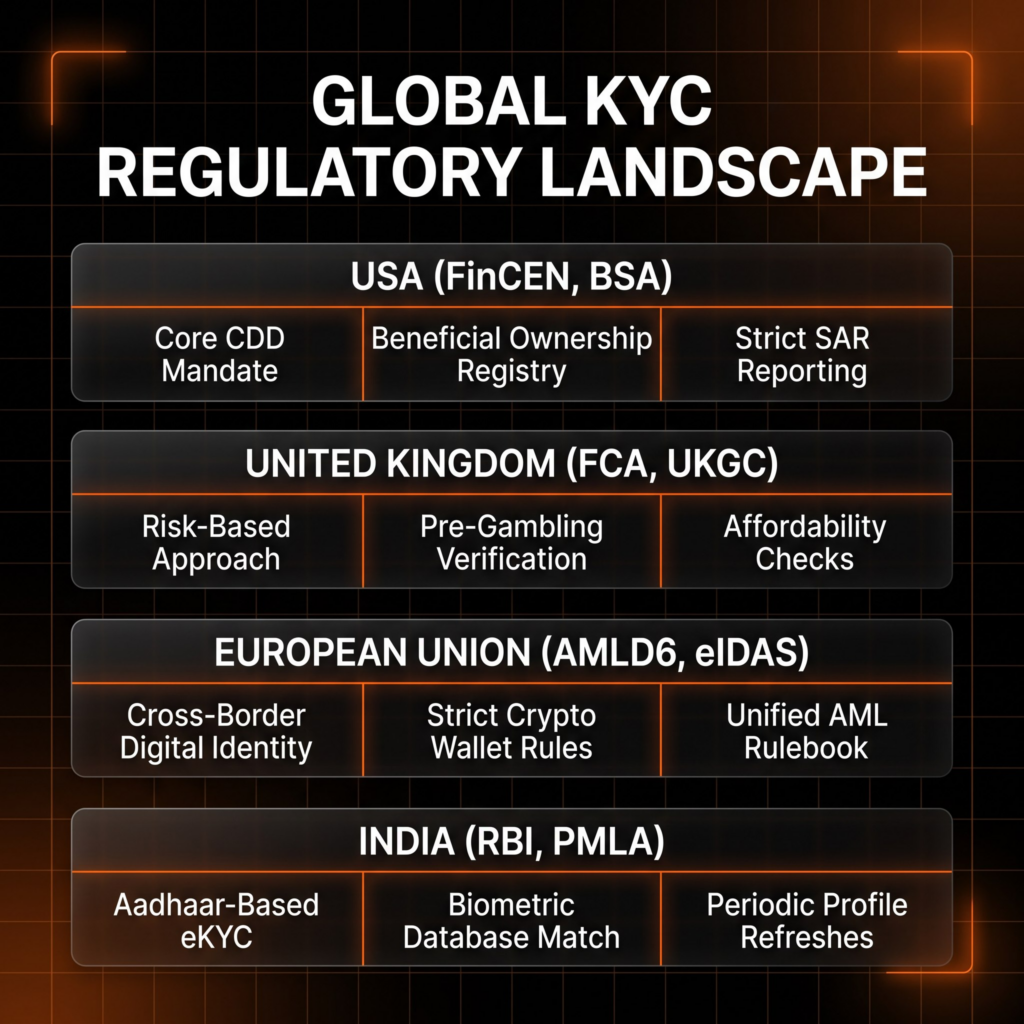

USA (FinCEN, BSA, Patriot Act)

The US regulations mandate that identity verification, identification of beneficial owners, risk assessment of the client, and continuous monitoring be done. These activities are considered critical customer due diligence activities by FinCEN.

UK (FCA, UKGC)

In the UK, however, the risk-based strategy is adopted. FCA’s guidelines emphasize customer due diligence, high-risk reviews, and continuous monitoring.

EU (AMLD5, AMLD6, eIDAS)

The EU approach uses anti-money laundering guidelines along with digital identity laws. The eIDAS directive enables trustworthy electronic identification and cross-border trust services.

India (RBI, PMLA)

In India, it involves validly issued documents, periodic updating of data, and the use of Aadhaar in electronic transactions wherever feasible.

| If you want to learn more about big iGaming countries, check Blask’s page with online gambling and betting market power ranking. |

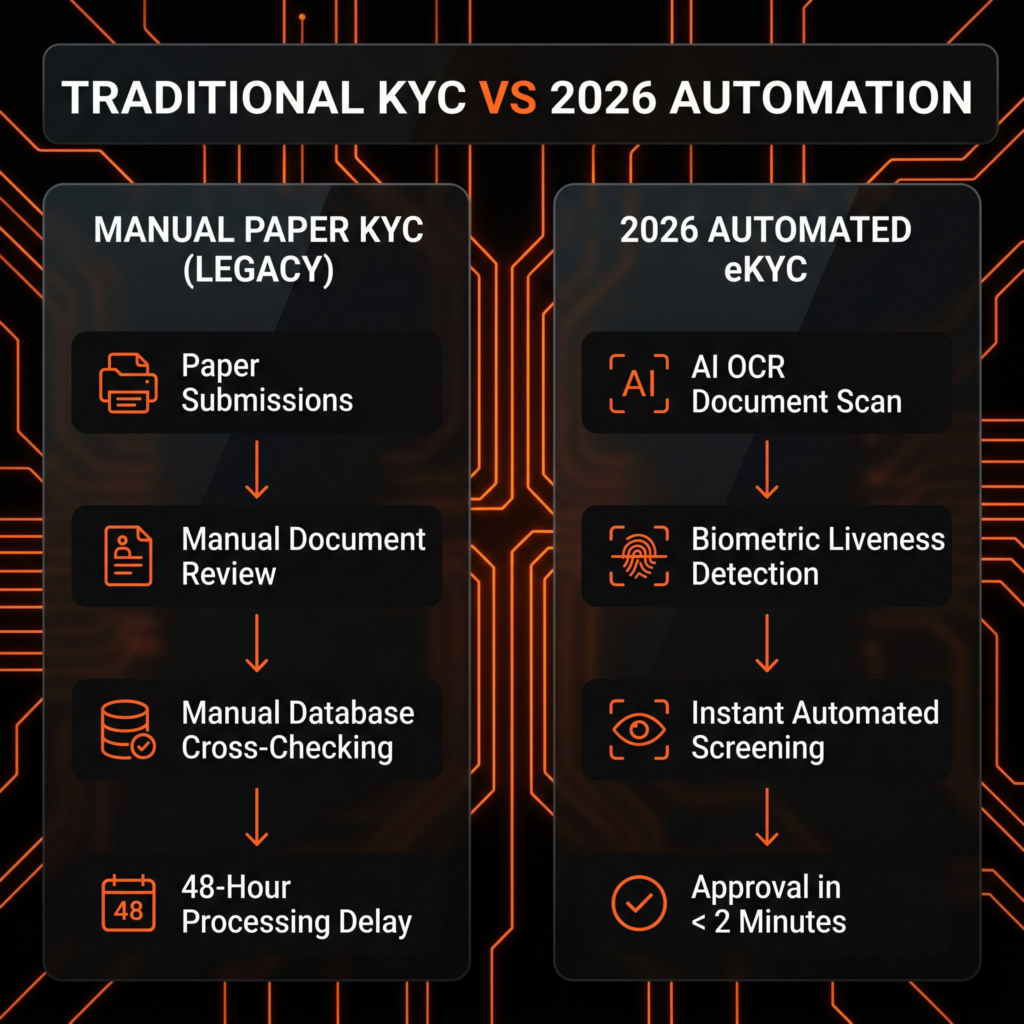

KYC Technology and Automation

The current stack has become more automated. Extraction, scoring, screening, and alerting processes are all managed through automation.

Biometric Authentication

Face recognition, fingerprints, and iris scans verify that the actual individual is the one making the claim. Such verification systems are used often during remote onboarding.

AI/ML Document Verification

The ID can be detected, checked for alteration, and matched against an existing database. This reduces human error and processing times.

Liveness Detection

Live facial detection technology confirms that a person is indeed there when taking their biometric features. The technique is useful in preventing fake and masked faces and replay attacks.

Blockchain-Based KYC

Blockchain-based identity verification models have the potential to offer portable identities and attestations. However, adoption is low because of issues of privacy and legality.

Common KYC Challenges

Even good systems hit trade-offs. Speed, accuracy, privacy, and regulation rarely move in perfect balance.

User Friction and Drop-Off

Long forms and repeated uploads kill conversion. Common friction points include:

- blurry documents,

- failed selfies,

- duplicate requests,

- slow manual review.

Privacy and Data Protection

KYC data is sensitive by nature. Storage, access control, retention, and lawful use must be tightly managed.

False Positives in Screening

Name screening still misfires on common names and poor data quality. Bad tuning overloads teams and annoys legitimate customers.

Cross-Border Compliance

Global firms face uneven rules, different document standards, and conflicting timelines. One workflow rarely fits every jurisdiction cleanly.

How Operators Implement KYC (Operator Side)

Strong KYC compliance usually starts with policy design, then vendor setup, decision rules, escalation paths, audit logs, and refresh cycles. The best teams connect onboarding with monitoring.

KYC Costs and ROI

Good Know Your Customer programs cut fraud losses, reduce manual workload, and lower the odds of regulatory pain.

| Metric | Target Range | Why It Matters |

| Auto-approval rate | 70–90% | Indicates efficient risk segmentation: low-risk users flow through instantly, preserving UX and CAC efficiency. Below 70% signals over-conservative rules or poor data quality. |

| False positive rate | <5% | Over-screening wastes compliance ops time, delays legitimate players, and inflates manual review costs. Low FP ensures teams focus on real risk, not noise. |

| Time-to-verify (median) | <45 seconds | Speed directly impacts conversion at registration and first deposit. Every 10-second delay can drop completion by 3–5%. Sub-45s is the 2026 industry standard. |

| Drop-off at KYC step | <15% | High friction at identity verification = wasted acquisition spend. Tracking drop-off by document type, geography, or device helps pinpoint UX bottlenecks. |

| Fraud catch rate (pre-funding) | >95% | Measures how well KYC stops synthetic identities, stolen docs, or mule accounts before they can deposit. Prevention is far cheaper than recovery. |

| Regulatory finding rate | 0 major findings/year | The ultimate lagging indicator: zero major audit findings on Know Your Customr processes proves operational effectiveness, not just policy documentation. |

| Cost per verified user | $0.80–$2.50 | Tracks efficiency of KYC stack (vendor fees + ops labor). Helps benchmark vendor performance and justify automation investments. |

Future Trends in KYC for 2026

The next wave focuses on portability, better signal quality, and fewer pointless checks. The model is getting smarter, not lighter.

Decentralized Identity (DID)

DID models aim to give users reusable, verifiable credentials. If standards mature, onboarding could become cleaner and faster.

Reusable KYC

Reusable profiles can reduce repeat uploads across products and markets. The challenge is trust, consent, and regulator acceptance.

AI-Powered Risk Scoring

AI scoring will keep improving alert quality and review priority. The winners will pair speed with explainability and audit control.