- Updated:

- Published:

What Is a PSP Manager in iGaming

Payments in iGaming are a core driver of player retention, revenue stability, and regulatory compliance. The specialist who orchestrates this complex ecosystem, balancing provider relationships, fraud prevention, and conversion optimization, becomes indispensable to any operator aiming to scale globally. That is precisely what a PSP Manager is, and why this role matters so much inside modern betting and casino businesses.

What Is a PSP Manager

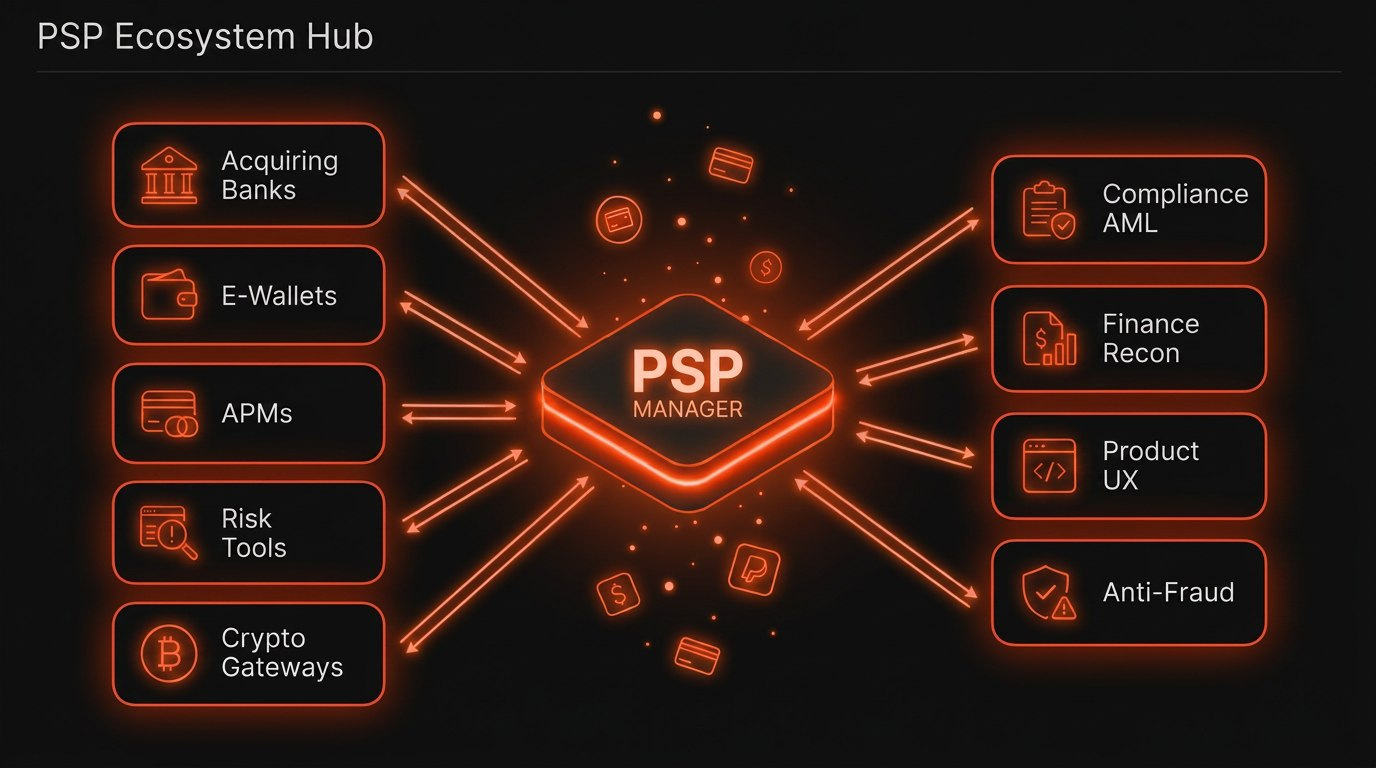

At the simplest level, what is a PSP manager in iGaming. It is the specialist who owns the relationship between an operator and its payment ecosystem. That ecosystem includes:

- processors;

- acquirers;

- wallets;

- local methods;

- risk tools;

- and finance workflows.

A PSP is a third party that helps merchants accept electronic payments. It connects merchants with banks, card schemes, and alternative payment methods. The manager sits above those connections and makes sure they work commercially and operationally.

Why PSP Managers Are Critical for iGaming Operators

A strong PSP manager iGaming setup protects revenue at the exact point where players decide to stay or leave. In gambling, poor approval rates or slow withdrawals damage retention very quickly. Payments also sit close to AML, KYC, fraud, and market access, so mistakes become expensive fast.

Operators also need different payment mixes for different regions. Cards may work in one market, while bank transfer, e-wallets, or instant methods dominate elsewhere.

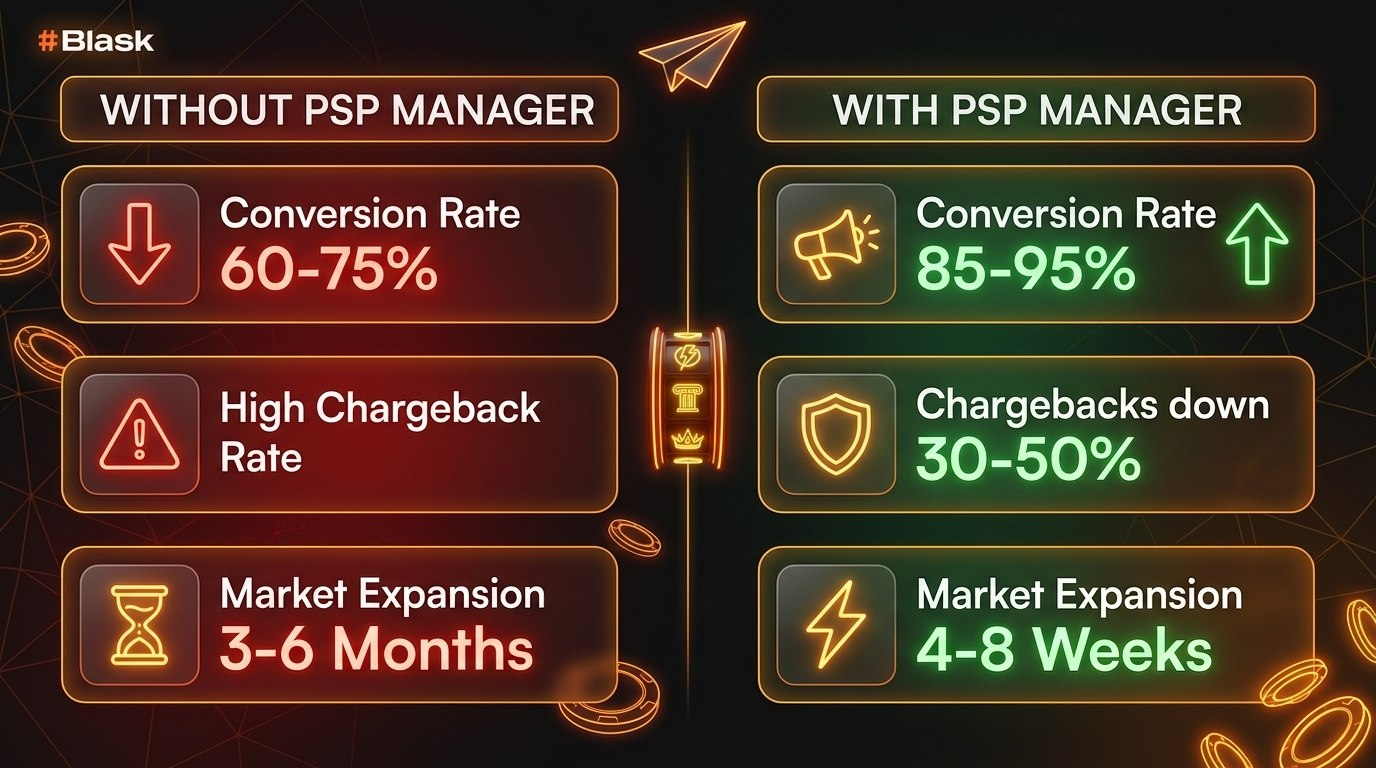

| Metric | Without PSP Manager | With PSP Manager |

| Payment Conversion | 60–75%, unstable, high drop-off rates | 85–95%+, optimized routing & methods |

| Fraud & Chargebacks | Reactive, high losses, provider risk | 30–50% lower chargeback rates, proactive prevention |

| Cost per Transaction | Hidden fees, poor routing, no negotiation | Optimized fees, balanced cost/conversion, better rates |

| Market Expansion | 3–6 months per market, wrong method mix | 4–8 weeks per market, data-driven local PSP selection |

| Provider Reliability | 1–2 partners, downtime during outages | Multi-provider routing, fallback logic, strong SLA |

Key Responsibilities of a PSP Manager

The daily scope is broad because payments touch product, finance, risk, and compliance at once. Most PSP manager responsibilities combine vendor management with hard performance control. The role is part commercial owner, part operator, and part internal fixer.

Managing Relationships with Payment Providers

A payment service provider manager spends a large share of the week with PSPs, acquirers, and account teams. That work covers pricing, service levels, outages, routing logic, and dispute escalation.

Onboarding New PSPs and Acquirers

A serious PSP manager job is never limited to maintaining old integrations. New markets, new products, and new regulatory rules force operators to add partners often. Each onboarding cycle needs due diligence, technical testing, legal review, and production monitoring.

Optimizing Payment Conversion Rates

One core task for a PSP manager is lifting approval and completion rates. That means studying declines, issuer behavior, fraud filters, and routing outcomes. It also means removing friction inside the cashier before players abandon the journey.

Monitoring Transaction Success Rates

Success rate monitoring sounds simple, but the detail is brutal. The manager tracks:

- deposits,

- payouts,

- pending states,

- retries,

- soft declines,

- and timeout patterns.

Chargeback and Fraud Management

A capable PSP executive cannot treat fraud as a separate department problem. Chargebacks, friendly fraud, abuse rings, bonus fraud, and account takeover all hit margin directly.

Financial Reconciliation

Reconciliation is where payment truth finally shows up. Operators must match gateway data, bank settlements, processor statements, and internal ledgers.

Geographic Payment Method Strategy

A payment manager iGaming specialist decides which methods deserve space in each country. That means understanding local customer habits, regulation, chargeback risk, and conversion costs.

Compliance Coordination (AML, KYC, PCI DSS)

Payments and compliance are joined at the hip in gambling. The manager usually coordinates with legal, fraud, and compliance teams on AML, KYC, sanctions, and PCI DSS expectations.

Required Skills for a PSP Manager

A strong PSP manager iGaming profile blends commercial judgment with operational discipline. The role needs curiosity, patience, speed, and strong tolerance for messy data. It also needs enough credibility to influence technical and finance teams.

Payment Industry Knowledge

The role starts with knowing how cards, bank rails, wallets, APMs, and crypto flows actually behave. Exacta and GamingCareer both point to broad payment method knowledge as a basic requirement.

Vendor and Partner Negotiation

A payment service provider manager must negotiate fees, reserves, settlement timing, support terms, and technical commitments. The best negotiators do not only chase lower costs. They push for better uptime, stronger escalation paths, and smarter routing support.

Data Analytics and Reporting

Payment teams live inside numbers. They track approval rates, fail reasons, fraud pressure, geographic spread, and processor costs every day.

Cross-Functional Communication

An iGaming payments manager spends most days translating between departments. Product wants fewer clicks, finance wants cleaner settlements, and compliance wants tighter controls.

Project Management

A typical PSP manager job includes launches, migrations, QA, contract changes, and emergency recovery work. That makes project management a real core skill, not a nice extra.

Tools PSP Managers Use Daily

The modern stack is much deeper than a processor dashboard. A PSP manager moves between orchestration panels, BI tools, finance systems, fraud engines, and provider portals.

Payment Orchestration Platforms

Orchestration tools help operators route traffic across multiple providers. That allows smarter fallback logic, cost control, and approval optimization.

BI and Analytics Tools (Tableau, Looker)

BI tools turn raw transaction logs into action. Teams use them to spot issuer drops, country issues, and payout delays quickly. Even when vendors differ, the reporting habit stays the same.

Reconciliation Software

Reconciliation software reduces manual matching and catches settlement drift early. Nuvei promotes dedicated reconciliation tooling because payment data rarely arrives clean from every source. In fast-moving operations, automation saves both money and argument.

Anti-Fraud Systems

Fraud tools score behavior, enforce rules, and support stronger authentication logic. Nuvei describes rule-based protection, geolocation controls, and smart 3DS routing as part of the fraud stack. In gambling, these systems protect both approval rate and risk exposure.

Key KPIs PSP Managers Track

Good teams do not manage payments by instinct. They manage them through numbers tied to revenue, risk, and player experience. That is why PSP manager responsibilities always include KPI ownership.

Payment Success Rate / Conversion

For a PSP manager iGaming specialist, approval rate is the headline metric. It shows whether players can actually fund accounts and complete the path. Conversion problems usually expose processor, issuer, UX, or fraud rule issues.

Average Transaction Time

Speed matters on both deposits and withdrawals. Slow deposits kill first-time conversion, while slow payouts damage trust and retention. The best teams measure time at each stage, not just end totals.

Chargeback Rate

Chargeback rate shows whether fraud, dispute handling, or payment method fit is deteriorating. It also affects processor relationships and commercial terms. A rising rate is never just a finance issue.

Cost per Transaction

A cheap payment method can become expensive if it converts badly. Strong teams compare direct fees with approval rates, support load, and fraud losses. Real optimization balances cost with usable revenue.

Geographic Coverage

A mature PSP manager tracks payment reach by country, currency, and product line. Coverage is not only about having methods live.

PSP Manager vs Other Payment Roles

Titles in payments vary widely between operators. One company says PSP Manager, another says Payment Operations Manager or Risk and Payments Manager. The difference usually lies in scope, seniority, and commercial ownership.

PSP Manager vs Payments Manager

Payments Manager is often broader and may include cashier UX, internal policy, and wider roadmap control. PSP Manager usually leans harder into provider relationships and payment performance.

| Criteria | PSP Manager | Payments Manager |

| Focus | PSP relationships, provider performance & routing optimization | End-to-end payment experience: UX, operations, policy & roadmap |

| Scope | External ecosystem: processors, wallets, APMs, fraud tools | Broader: PSPs + cashier flow + internal processes + compliance alignment |

| Strategic goal | Tactical optimization within existing framework | Mid-level strategy: method prioritization, vendor tiering, feature planning |

| Expected results | Higher approval rates, lower costs, stable provider SLAs | Smoother player journey, scalable operations, cross-functional alignment |

PSP Manager vs Head of Payments

Head of Payments owns strategy, budget, senior vendor relationships, and executive reporting. The manager handles execution, delivery, and day-to-day performance. In growing operators, the manager becomes the engine under the head role.

| Criteria | PSP Manager | Head of Payments |

| Decision level | Execution & optimization within approved strategy | Strategy definition, budget allocation, executive reporting |

| Time horizon | Weekly/monthly: performance tuning, incident response | Quarterly/annual: roadmap, partnerships, team structure, M&A input |

| Team role | Individual contributor or small team lead | Department head: hires, mentors, owns P&L for payments function |

| Stakeholder tier | PSP account managers, Risk, Finance ops | C-suite, Board, Legal, Strategic partners, Investors |

PSP Manager vs Payment Operations Specialist

An operations specialist is usually more hands-on and narrower. That person may monitor queues, reconcile issues, or support incidents.

| Criteria | PSP Manager | Payment Operations Specialist |

| Seniority | Mid/Senior: owns outcomes & KPIs | Junior/Mid: executes tasks & monitors queues |

| Scope | Multi-provider strategy, negotiations, root-cause analysis | Daily reconciliations, ticket handling, basic reporting |

| Autonomy | Decides routing logic, escalates to providers, proposes fixes | Follows playbooks, escalates issues, implements predefined actions |

| Problem Type | Structural. For example, why is CR dropping in Brazil? | Operational. For example, why the particular is stuck and to revolve it |

PSP Manager vs Acquiring Manager

An Acquiring Manager focuses more tightly on card acquiring banks, scheme performance, and routing. PSP Managers cover a wider mix of providers and methods. That wider lens matters in modern multi-method gambling cashiers.

| Criteria | PSP Manager | Acquiring Manager |

| Payment Coverage | Full mix: cards, wallets, bank transfers, local APMs, crypto | Focused: card acquiring (Visa/MC/Amex), scheme rules, bin routing |

| Partner Type | Diverse: PSPs, aggregators, fintechs, alternative methods | Narrow: acquiring banks, card schemes, processor tech teams |

| Optimization Lever | Method mix, geographic routing, fallback logic, cost/conversion balance | Scheme fees, interchange optimization, 3DS rules, auth rate tuning |

| Market Adaptability | High: quickly adds local methods per region | Moderate: changes require bank/scheme coordination, longer cycles |

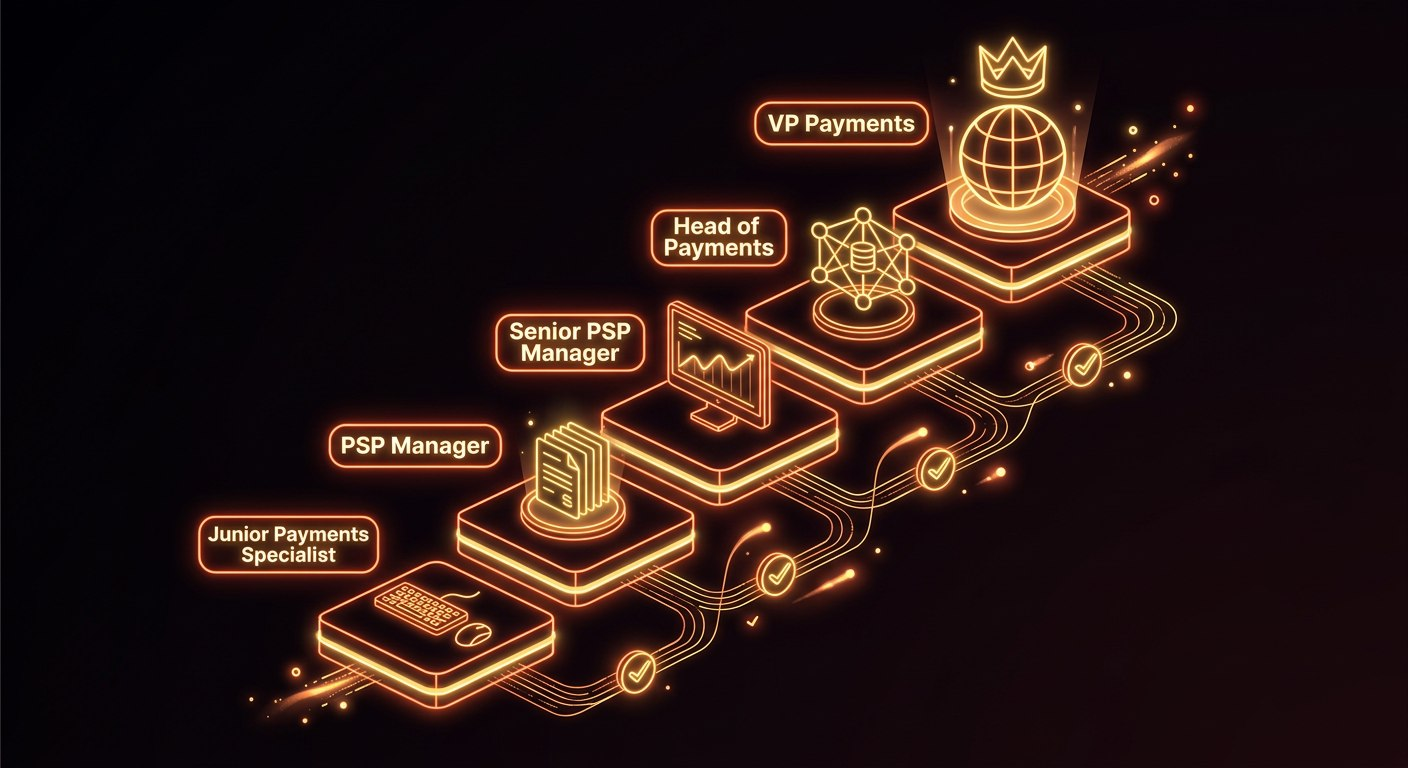

Career Path for PSP Managers

The career path is usually practical rather than academic. Most people arrive through operations, finance support, risk, or payment integration work. After that, scope expands through market launches and provider ownership.

This is a visualisation of the PSP manager career track. Detailed explanation of each position is provided below.

Junior Payments Specialist → PSP Manager

Many start in support, reconciliation, risk, or payment testing roles. That route teaches the ugly details of failure reasons and operational bottlenecks.

PSP Manager → Senior PSP Manager

Senior scope usually means more markets, bigger providers, and tougher commercial negotiation. It also means deeper ownership of KPIs and broader internal influence. The work becomes less reactive and more structural.

Senior PSP Manager → Head of Payments / VP Payments

At this stage, the role becomes strategic. The leader shapes processor mix, team design, payment roadmap, and board-level reporting. Commercial judgment starts to matter as much as operational control.

Lateral Moves (CFO Office, Risk, Compliance)

Reconciliation knowledge fits finance, fraud knowledge fits risk, and AML exposure fits compliance. That mobility makes the function attractive for ambitious operators.

PSP Manager Salary Ranges

The PSP manager salary depends heavily on geography, scope, and company stage. Public market data is patchy, so salary ranges should be treated as directional. Even so, the pattern is clear across hiring pages and salary trackers.

Junior / Mid (Cyprus, Malta)

In Cyprus, CyprusWork shows a Payments Operations Manager role at EUR 36,000 to 48,000 yearly. Malta market evidence also shows strong mid-level demand, including PSP-focused roles advertised up to EUR 70,000. Those ranges depend on licensing exposure and actual ownership level.

Senior (UK, US)

Glassdoor lists a UK average around GBP 43,468 for PSP Manager, while London Senior Payments Manager estimates sit higher. In the US, Glassdoor shows Payments Manager around USD 119,481 and Senior Payments Manager around USD 129,067. Salary.com also places US Payments Manager pay in a similar higher band.

Bonus and Stock Options

Variable pay is common in growth companies and fintech-adjacent operators. Sporty Group publicly highlights quarterly performance bonuses for its payment operations leadership roles. Stock options appear more often in venture-backed or international groups.

How to Become a PSP Manager

The route into the role is practical and cumulative. Employers usually want real payment exposure, not only theory. Experience with gambling flows, fraud pressure, and market launches helps a lot.

Educational Background

Most employers prefer finance, business, economics, or technical education. That said, payment teams often value hands-on operators over perfect degrees. Results and process discipline usually beat academic prestige.

Industry Certifications

Formal certificates help most when they support real experience. AML, fraud, PCI, and product or project certifications can strengthen a profile. They rarely replace strong live-market exposure.

Building Experience

The best route is to own real payment problems. Reconciliation, testing, provider communication, and performance reporting all build useful muscle. That is why adjacent roles often feed into the function.

Networking in iGaming

Payments hiring still runs strongly through specialist recruiters and industry circles. Exacta openly notes that many payment positions are not always widely advertised. That makes networking more important than in many other functions.

Common Challenges PSP Managers Face

The role looks glamorous from the outside, but most days are messy. Payment teams deal with commercial pressure, regulatory pressure, and live customer friction at once.

High-Risk Merchant Status

Gambling is generally viewed as a high-risk vertical both for banking partners and payment processors. This usually results in reserve requirements, close scrutiny, increased charges, and longer approval times.

Banking Restrictions

The appetite for gambling banking services varies between iGaming markets and depends on a gambling company’s characteristics. While one jurisdiction might offer trouble-free card processing, another will require excessive use of locally based processors.

Crypto Integration

The advantages brought by crypto are speed and access; however, risks and policies become an issue to consider. The wallet integration, tracing, sanctions screening, and internal controls will also become challenging.

Multi-Jurisdiction Compliance

Multi-licensed companies have varying local regulations regarding KYC, payout, limits, and provider implementation. Payments, legal, and compliance should always work hand-in-hand.

How to Hire a Great PSP Manager (For Operators)

An operator must always choose for judgment, not processors’ names. The ideal candidate should be able to articulate problems, enhance metrics quickly, and be comfortable working with the finance and product teams. A good hiring decision also involves knowing not to go ahead with a poor strategy.

The signs of a poor specialist:

- Can’t explain KPI drops in plain language. It means that a worker doesn’t clearly understand the reason for the drop.

- Reacts on chargeback spikes after they have happened. A good specialist can detect the problem before it will affect the business.

- Provides their boss with blur answers. For example, when asked “What would you fix first?”, they give vague answers (“improve performance”) vs. specific, prioritized actions (“reduce BR declines by tuning 3DS rules + adding local wallet X”).

- Overoptimizes the costs but ignores the conversion rate. Chases the cheapest PSP but ignores approval rates or UX friction. As a result, the company gets lower fees, but much lower revenue. True optimization balances cost and conversion quality.

- Has no GEO or method diversification strategy.

A good interview process must measure live thinking skills. Some helpful examples may involve deposit failure in one market, increasing chargebacks, or settlement delay.

Top iGaming Companies Hiring PSP Managers

Sporty Group has publicly advertised payment operations leadership with ownership over conversion, compliance, and fraud strategy. Rush Street Interactive also lists Risk and Payments Manager and Risk and Payments Analyst roles on its public jobs board. Cyprus and Malta listings include Senior Payments Manager, Account Manager for Payment Solutions, and PSP-focused iGaming roles.

Future of the PSP Manager Role in 2026

In 2026, the strongest teams will likely reward managers who can combine data, compliance, and commercial logic. The classic operator who only maintains provider contacts is fading out.