- Updated:

- Published:

What is a white label casino

Launching an online casino from scratch takes 12 to 24 months and can cost over a million dollars before a single player registers. A white label casino compresses that timeline to 4–8 weeks and a fraction of the capital — by shifting the licensing, technology, and compliance burden to a specialist provider while the operator focuses on brand and player acquisition. This article explains exactly how that model works, what it costs in 2026, how it compares to turnkey and in-house alternatives, and when it makes commercial sense to use it.

What is a white label casino

| In iGaming, a white label casino works in the following way: a specialist technology provider builds, licenses, and maintains a fully operational gambling platform, which an operator then rebrands, markets, and monetizes under their own domain and identity. |

Understanding what is a white label casino means distinguishing it from every other route into the iGaming market. The operator does not own the gambling license, does not integrate the games directly, does not negotiate merchant accounts with payment processors, and does not manage regulatory compliance. All of that sits with the provider. The operator contributes a brand, a marketing strategy, and a player acquisition budget — and in exchange earns a share of the gross gaming revenue (GGR) generated on the platform.

Modern packages from established providers include a full game catalog (often 5,000–10,000 titles), integrated payment processing, KYC and AML tooling, a bonus engine, affiliate management, customer support infrastructure, and regulatory compliance — all covered by the provider’s master gambling license.

How a white label casino works

The provider supplies the infrastructure; the operator supplies the brand and the players. Each party has defined responsibilities that rarely overlap.

A white label casino operates through a structured commercial and technical partnership.

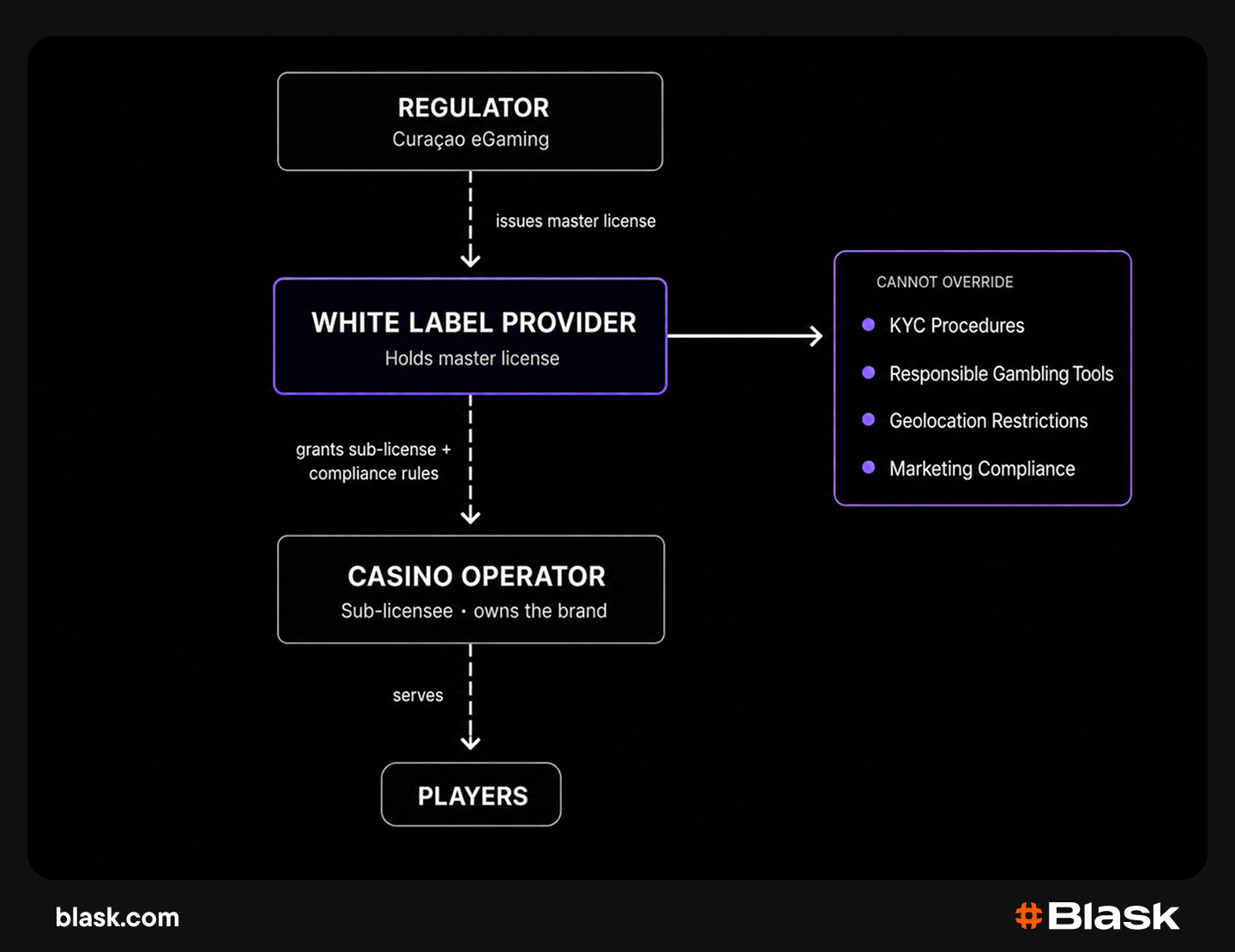

Provider’s license covers operator

The most commercially significant feature of white label gambling is license coverage. Obtaining an independent gambling license is expensive, slow, and jurisdictionally complex. For example, a Malta Gaming Authority (MGA) license can take 12–18 months and cost €25,000 in application fees alone, plus ongoing compliance costs. A UK Gambling Commission (UKGC) license requires a dedicated compliance team and carries operational restrictions that smaller operators struggle to maintain independently. Curaçao eGaming licenses are faster and cheaper — typically $30,000–$50,000 and 4–8 weeks — but still require ongoing renewal and compliance.

Under the white label model, the operator’s platform operates as a sub-licensee under the provider’s master license. The operator avoids the licensing process entirely but is bound by the provider’s compliance standards. KYC procedures, responsible gambling tools, geolocation restrictions, and marketing compliance are all set by the provider and cannot be overridden.

Operator brands the frontend

The operator receives a templated frontend — website layout, mobile interface, game lobby structure — which they customize according to the developed design. Most white label iGaming platforms include a CMS allowing non-technical operators to update promotions, configure banners, and manage content without developer support.

Shared banking and payment setup

Payment processing in a white label arrangement is pre-integrated. Providers maintain master merchant accounts with major PSPs, enabling operators to accept cards, e-wallets, bank transfers, and increasingly crypto from launch day. This solves one of the most practically difficult problems in iGaming: payment processors treat online gambling as a high-risk category and routinely reject new operator applications. The white label model bypasses this entirely through the provider’s established relationships.

Revenue share with provider

White label gambling is funded through a GGR revenue share. The provider takes a percentage of every dollar the operator generates — typically 30–50% — in perpetuity. Some providers add a monthly platform fee on top. The operator earns the remainder after game royalties and platform costs. This structure caps long-term margin potential but eliminates the need for significant upfront capital.

White label vs turnkey casino: key differences

White label vs turnkey casino is one of the most searched questions among new iGaming operators. The terms are sometimes used interchangeably in the industry but describe fundamentally different arrangements.

| Blask has the article with a detailed explanation of what a turnkey casino is. |

License ownership

| Criterion | White Label | Turnkey |

| License holder | Provider | Operator |

| Regulatory liability | Provider | Operator |

| Portability on exit | None | License stays with operator |

In a white label setup, the operator never acquires a license. If the provider relationship ends, the operator cannot continue work. In a turnkey model, the operator obtains their own license — often with the provider’s assistance — and retains it independently of any software relationship.

Setup time and cost

| Component | White Label | Turnkey |

| Time to launch | 4–8 weeks | 3–9 months |

| Upfront investment | $10,000–$50,000 | $150,000–$600,000+ |

| License included | Yes (provider’s) | No (separate process) |

Customization depth

| Capability | White Label | Turnkey |

| Frontend design | Template-based | Fully custom |

| Game catalog control | Provider’s selection | Direct studio contracts |

| Bonus engine | Standard configuration | Full ownership |

Revenue control

White label revenue share permanently transfers 30–50% of GGR to the provider. Turnkey operators pay a platform license fee and retain their full GGR minus game royalties. An operator generating $1M GGR per month pays $300,000–$500,000 monthly under white label; a comparable turnkey operator might pay $20,000–$50,000 in platform fees.

Long-term independence

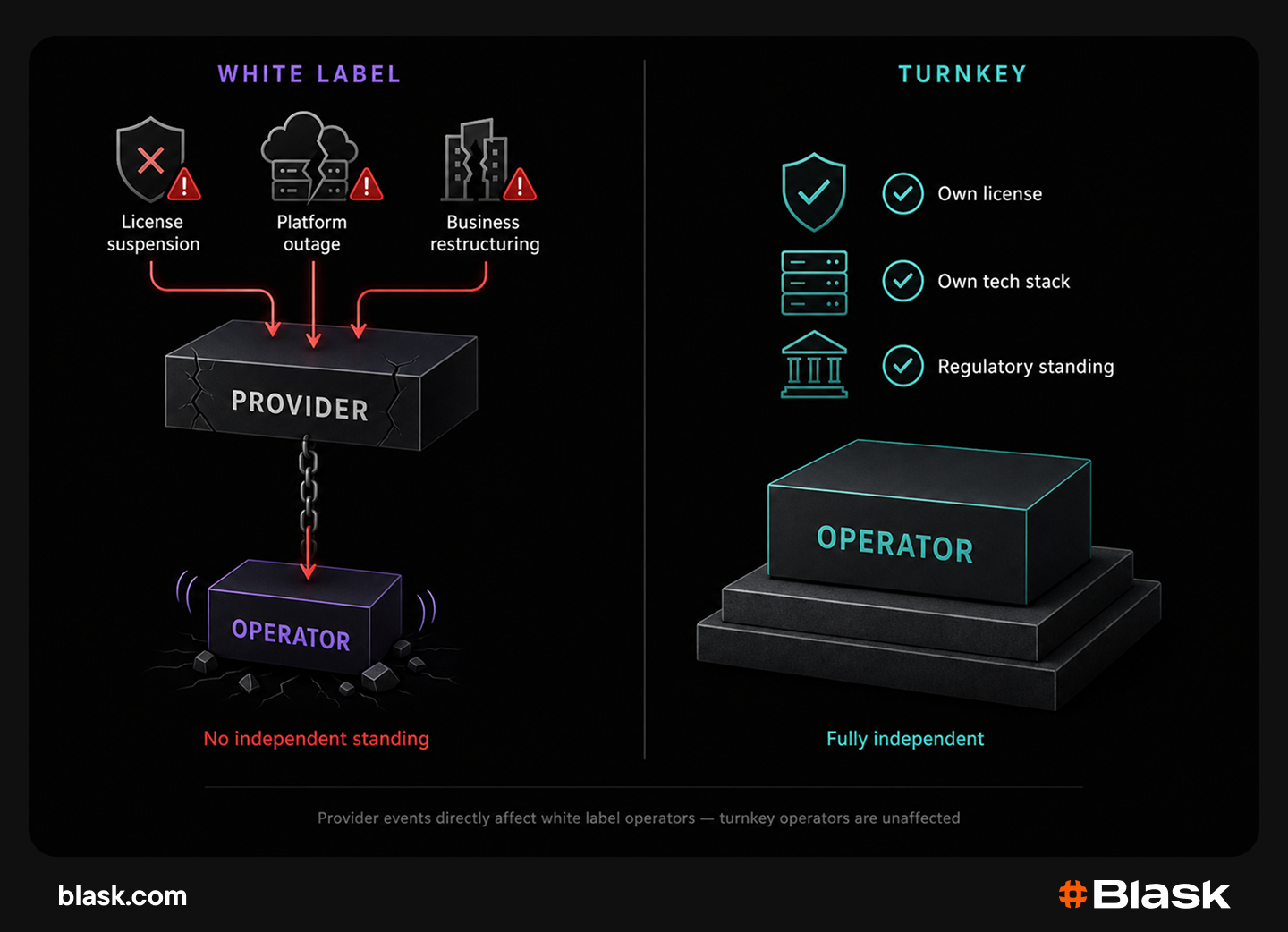

White label operators are commercially and technically dependent on their provider.

A provider’s license suspension, platform outage, or business restructuring directly affects the operator. Turnkey operators own their technical stack and regulatory standing independently, providing significantly more resilience.

What’s included in a white label package

A comprehensive white label casino solution bundles several layers of infrastructure into a single commercial agreement.

Gambling license coverage

Sub-license access under the provider’s master license. Common base jurisdictions:

- Curaçao (fastest, most permissive, lowest cost);

- MGA Malta (EU-facing, higher compliance bar);

- Isle of Man (mid-tier);

- Gibraltar (UK-adjacent).

UKGC white label products exist but are limited due to the Commission’s strict sub-licensing rules.

Casino platform software

The core platform includes:

- player registration and KYC flows;

- account and session management;

- game RTP configuration;

- bonus and promotions engine;

- loyalty and VIP tiers;

- automated CRM triggers;

- operator-facing reporting dashboards.

Game aggregation (1,000+ titles)

Providers aggregate content from multiple studios — typically 1,000 to 10,000 titles depending on the package. Content spans:

- slots;

- live casino (Evolution Gaming, Pragmatic Play Live, Ezugi);

- virtual sports;

- crash games;

- table game variants.

According to Statista, slots account for approximately 70% of global online casino revenue, making depth of slot catalog a primary commercial variable.

Pre-integrated PSPs

Standard white label casino solution packages include Visa/Mastercard processing, major e-wallets (Skrill, Neteller), and crypto options (Bitcoin, USDT, Ethereum).

Regional packages add market-specific methods. For example, PIX and Boleto for Brazil, OXXO for Mexico, PSE and Efecty for Colombia, local bank transfers for Nigeria and Kenya.

Customer support infrastructure

Most providers include 24/7 shared support (live chat and email) that operates under the operator’s brand. Dedicated support teams are available on premium tiers.

Anti-fraud and compliance

The most serious aspect when it comes to launching the casino. Ant-fraud and compliance include:

- KYC identity verification;

- AML transaction monitoring;

- responsible gambling features (deposit limits, session limits, self-exclusion, reality checks);

- geolocation blocking;

- fraud detection.

CMS and back-office

Operator-facing back-office for player management, bonus configuration, game lobby curation, financial reporting, and affiliate tracking. Most include a CMS for marketing content, SEO metadata, and promotional materials.

White label casino setup process

Despite the operational complexity behind the scenes, the operator-facing launch process is structured and predictable.

Step 1: choose a white label provider

To choose the white label provider, the casino needs to evaluate the following things:

- license jurisdiction coverage for your target market;

- game catalog depth;

- payment method availability in your region;

- revenue share structure;

- monthly platform fees;

- existing operator track record.

The provider selection effectively sets the ceiling of the product’s capabilities for the duration of the contract.

Step 2: brand and design frontend

Then, an iGaming brand has to submit brand assets — logo, color palette, typography, domain — and configure the templated frontend. Providers typically offer a library of pre-built themes with customization options. Custom frontend design is available at additional cost on higher tiers. Typical turnaround: 1–2 weeks.

Step 3: configure game lobby

The third step is selecting and sequencing titles from the provider’s catalog. The customer has to define lobby sections (slots, live casino, jackpots, new releases, crash games), set featured content, and configure demo-play permissions where permitted by license jurisdiction.

Step 4: set up marketing and promotions

The fourth step is to configure welcome bonus structure, ongoing promotions calendar, loyalty program tiers, and affiliate program parameters. Most providers include an affiliate management module or integrate with platforms such as Income Access, MyAffiliates, or TUNE.

Step 5: launch and acquire players

Following QA testing and compliance sign-off by the provider, the platform goes live. Player acquisition through SEO, paid media, affiliate networks, and partnership marketing begins. The provider manages platform maintenance and security; the operator focuses on growth.

White label casino costs in 2026

White label casino cost structures in 2026 reflect a mature market with several price tiers. The following figures represent current market benchmarks for established providers.

Setup fees (low upfront)

| Cost component | Typical range | Notes |

| Platform setup fee | $10,000–$50,000 | One-time, covers onboarding |

| Frontend design | $2,000–$15,000 | Template vs. custom |

| Domain and SSL | $500–$2,000 | Annual recurring |

Monthly platform fees

| Tier | Monthly fee | Key inclusions |

| Entry | $2,000–$5,000 | Standard features, shared support |

| Mid-market | $5,000–$15,000 | Custom integrations, dedicated AM |

| Premium | $15,000–$30,000+ | Custom dev, dedicated support team |

GGR revenue share (typical 30–50%)

The revenue share is the dominant ongoing cost of white label gambling operation. An operator generating $500,000 GGR per month at a 40% share transfers $200,000 monthly — or $2.4 million annually — to the provider.

| Monthly GGR | 30% Share | 40% Share | 50% Share |

| $100,000 | $30,000 | $40,000 | $50,000 |

| $500,000 | $150,000 | $200,000 | $250,000 |

| $1,000,000 | $300,000 | $400,000 | $500,000 |

Marketing budget

The white label model does not reduce player acquisition costs. CPA in competitive markets (UK, Brazil, Germany, Canada) ranges from $200 to $800 per depositing player depending on channel and vertical. New operators typically budget $50,000–$200,000 for the first six months of acquisition.

Top white label casino providers

The white label casino providers landscape is concentrated, with a small number of platforms accounting for the majority of active white label brands globally.

SOFTSWISS

SOFTSWISS is a leading iGaming technology company with offices across Europe, operating under Curaçao and Malta licensing frameworks. Their Casino Management System powers hundreds of active brands and is particularly strong in crypto gambling infrastructure. Their in-house game studio BGaming adds proprietary content to the catalog. Strong presence in CIS, LATAM, and crypto-native markets.

BetConstruct

BetConstruct is an Armenia-headquartered provider offering a full-spectrum white label package: online casino, sportsbook, virtual sports, poker, and live dealer. Licensed under Malta and Curaçao frameworks. Particularly strong in CIS, MENA, and African markets. Offers both combined and standalone casino or sportsbook white label products.

EveryMatrix

EveryMatrix is a Malta-based B2B provider operating under MGA licensing. Their CasinoEngine aggregates content from 300+ game studios. Known for deep game catalog, API-first architecture, and regulatory compliance in markets including UK, Germany, and Scandinavia. Offers both revenue share and SaaS flat-fee commercial models.

Soft2Bet

Soft2Bet is a Malta-registered operator-turned-provider known for gamification-heavy platform design. Their white label product draws on experience operating their own brands in European regulated markets. Strong in engagement mechanics and player retention tooling.

Aspire Global

Aspire Global (acquired by NeoGames in 2022) operates white label casino and sportsbook products under MGA and UKGC licensing. One of the few providers offering genuine UKGC white label products. Known for compliance rigor and fully managed service options, including player support and risk management.

GiG (Gaming Innovation Group)

GiG is an Oslo-listed technology company operating both a Platform Services division and a media (affiliate) arm. Their white label offering is distinctive in combining platform infrastructure with organic traffic acquisition tools from their affiliate network — giving operators access to player acquisition support alongside the technical product.

Pros and cons of white label casinos

Pros: fast launch, low upfront cost, no license hassle

Speed to market. A white label casino can be operational in 4–8 weeks. An independent operator building from scratch — including licensing, platform development, and payment integration — typically requires 12–24 months. In markets where first-mover advantage matters, this gap is commercially significant.

Capital efficiency. The absence of independent licensing ($30,000–$500,000 depending on jurisdiction) and platform development ($200,000–$1,000,000+) reduces required startup capital by 80–90% compared to independent operation. This makes iGaming accessible to operators without institutional funding.

Operational simplicity. Platform maintenance, game integrations, payment processing, compliance, and technical support are all managed by the provider. The operator’s team can focus exclusively on brand building and player acquisition — the two activities most directly correlated with revenue.

Reduced technical risk. White label eliminates platform development failure risk, payment processor application rejection, and the complexity of direct game studio contract negotiation. All of these are material risks for first-time operators without iGaming-specific technical expertise.

Cons: lower margins, less control, provider dependancy

Permanent margin compression. The 30–50% GGR revenue share is the structural disadvantage of the white label model. Operators who scale successfully often spend more in provider revenue share annually than they would spend owning the equivalent infrastructure independently.

Limited product differentiation. Multiple operators sharing the same platform, game catalog, and bonus engine templates creates a ceiling on player experience differentiation. Brand and marketing become the primary competitive variables — a disadvantage against operators with proprietary technology.

Provider dependency. Business continuity depends on the provider’s license status, platform uptime, payment processing relationships, and commercial stability. Provider-side problems translate directly into operator-side problems, with limited recourse.

Restricted market access. Most white label licenses are Curaçao-based, which excludes regulated markets including the UK, Germany, Sweden, the Netherlands, and Ontario. Operators targeting regulated markets typically need provider-specific solutions or eventually transition to independent licensing.

When to choose white label (vs turnkey or in-house)

The model selection should be driven by capital availability, target market regulatory status, long-term strategic intent, and internal operational capacity.

| Operator profile | Recommended model |

| First launch, limited capital (<$500K) | White label |

| Scaling operator, proven market, own license target | Turnkey |

| Enterprise operator, own technical team | In-house build |

Choose white label when: startup capital is limited, the goal is market validation before committing to infrastructure, the target market accepts Curaçao or MGA sub-licensing, and no in-house technical team exists.

Choose turnkey when: the operator has capital for independent licensing, targets regulated markets requiring own-license operation (UKGC, BNL, MGA direct), and has a 12–24 month runway to launch.

Choose in-house when: the operator is an established brand with consistent $5M+ monthly GGR seeking to control full margin, has an existing development team, and is building proprietary features that no existing platform offers.

White label sportsbook: same model, sports focus

The white label sportsbook model applies identical infrastructure logic to sports betting. A provider supplies the odds feed (sourced from Betradar or IMG Arena), risk management and trading infrastructure, cash-out functionality, live betting interface, and markets across major sports — bundled under the same commercial and licensing framework as a casino white label.

Providers including BetConstruct, Altenar, and SBTech (integrated into DraftKings’ B2B arm) specialize in sportsbook white label alongside casino products. Combined casino-and-sportsbook packages are the most common commercial arrangement, allowing operators to offer a full-service gambling product from a single provider agreement.

The key operational distinction in sportsbook white label is risk management. Unlike casino products where the house edge is fixed mathematically, sportsbook operators carry live exposure on individual events. Most white label sportsbook providers offer a managed trading service, handling odds compilation and liability management on the operator’s behalf — an essential service for operators without in-house trading expertise.

Common mistakes in white label casino launch

Underestimating marketing costs. The most common failure in white label launches is treating the platform cost as the primary budget item. Player acquisition in competitive markets typically costs $300–$800 per depositing player. New operators without an established affiliate network or organic traffic channel routinely run out of acquisition budget within six months.

Choosing provider by price alone. A lower setup fee does not translate to lower total cost. Platform stability, game catalog depth, payment method fit for the target market, and the provider’s compliance track record are more commercially significant than headline setup pricing.

Ignoring payment method fit. A platform offering only Visa/Mastercard and Skrill will structurally underperform in markets where local payment methods dominate: PIX in Brazil (representing approximately 30% of online transactions per Banco Central do Brasil), OXXO in Mexico, M-Pesa in East Africa. Payment method coverage directly drives deposit conversion.

Neglecting responsible gambling infrastructure. Even in unregulated markets, responsible gambling tooling is increasingly required by PSPs as a condition for maintaining merchant accounts. Operators who treat this as optional frequently encounter payment processing problems within 12–18 months.

No exit strategy. Operators who do not plan the eventual transition to independent operation from day one often find themselves permanently trapped in the revenue share model with no viable path to margin improvement.

How to transition from white label to independent operator

The transition from white label to independent operation becomes commercially justified when the ongoing revenue share cost exceeds the annualized cost of owning equivalent infrastructure — typically at approximately $500,000–$1M monthly GGR.

Step 1. Obtain an independent license. Begin the application process 12–18 months before the intended transition. MGA Malta, Isle of Man, Gibraltar, and jurisdiction-specific licenses (UKGC for UK, BNL for Netherlands, AGCO for Ontario) are the most common targets. Application fees and timeline vary significantly.

Step 2. Contract a turnkey platform. Identify a platform provider offering direct licensing, or begin in-house development. Establish direct game studio contracts — most studios require minimum monthly revenue guarantees of $10,000–$50,000 per contract.

Step 3. Establish direct merchant accounts. Apply for direct PSP relationships. This requires compliance documentation, demonstrated business history, and typically a minimum processing volume commitment. Allow 3–6 months for approval.

Step 4. Plan player database migration. This is the most legally complex step. Players must consent to data migration under GDPR and applicable local data protection law. The process requires careful legal structuring and ideally begins while the white label relationship is still active.

Step 5. Parallel operation and cutover. Run both platforms simultaneously during the transition period, then redirect domain traffic to the independent platform once all systems are confirmed operational and stable.

Future trends in white label casinos for 2026

Crypto-native white label. The sustained growth of crypto gambling has driven provider investment in blockchain-native infrastructure. Providers including SOFTSWISS now offer crypto-first white label products with integrated wallet management, provably fair game certification, and stablecoin (USDT, USDC) payment rails. This is the fastest-growing white label segment by new operator launches.

AI-driven personalization. Provider platforms are integrating machine learning-based personalization into game lobby display, bonus offer sequencing, and player communication timing. This narrows the product experience gap between white label and custom-built platforms, as operators can deliver individualized player journeys without proprietary technology.

Regulated market expansion. As major markets complete or mature their regulatory frameworks — Brazil finalized its sports betting and casino regulation in January 2025, with full casino licensing underway — demand is increasing for white label products pre-certified for those markets. Providers with local payment integration and compliance infrastructure for Brazil, Colombia, and Mexico are positioned for significant commercial growth.

Headless architecture. New white label products increasingly offer API-first, headless delivery — providing backend services (game aggregation, payments, bonus engine, compliance) while giving operators full frontend freedom via custom development. This substantially narrows the customization gap between white label and turnkey arrangements.

Provider consolidation. The white label providers market is consolidating: Aspire Global’s acquisition by NeoGames, EveryMatrix’s continued platform expansion, and GiG’s growth all reflect a trend toward fewer, larger platforms. Operators evaluating providers should factor financial stability and long-term roadmap into their selection criteria alongside the current feature set.

According to Mordor Intelligence, the B2B iGaming software and platform market is projected to grow at a CAGR of 9.2% through 2029, driven by mobile adoption, emerging market regulation, and AI integration into player engagement systems. White label iGaming infrastructure will continue to be the primary entry mechanism for new operators in this market expansion — and increasingly, a viable long-term operational model for mid-market operators who choose depth of marketing over depth of technology ownership.