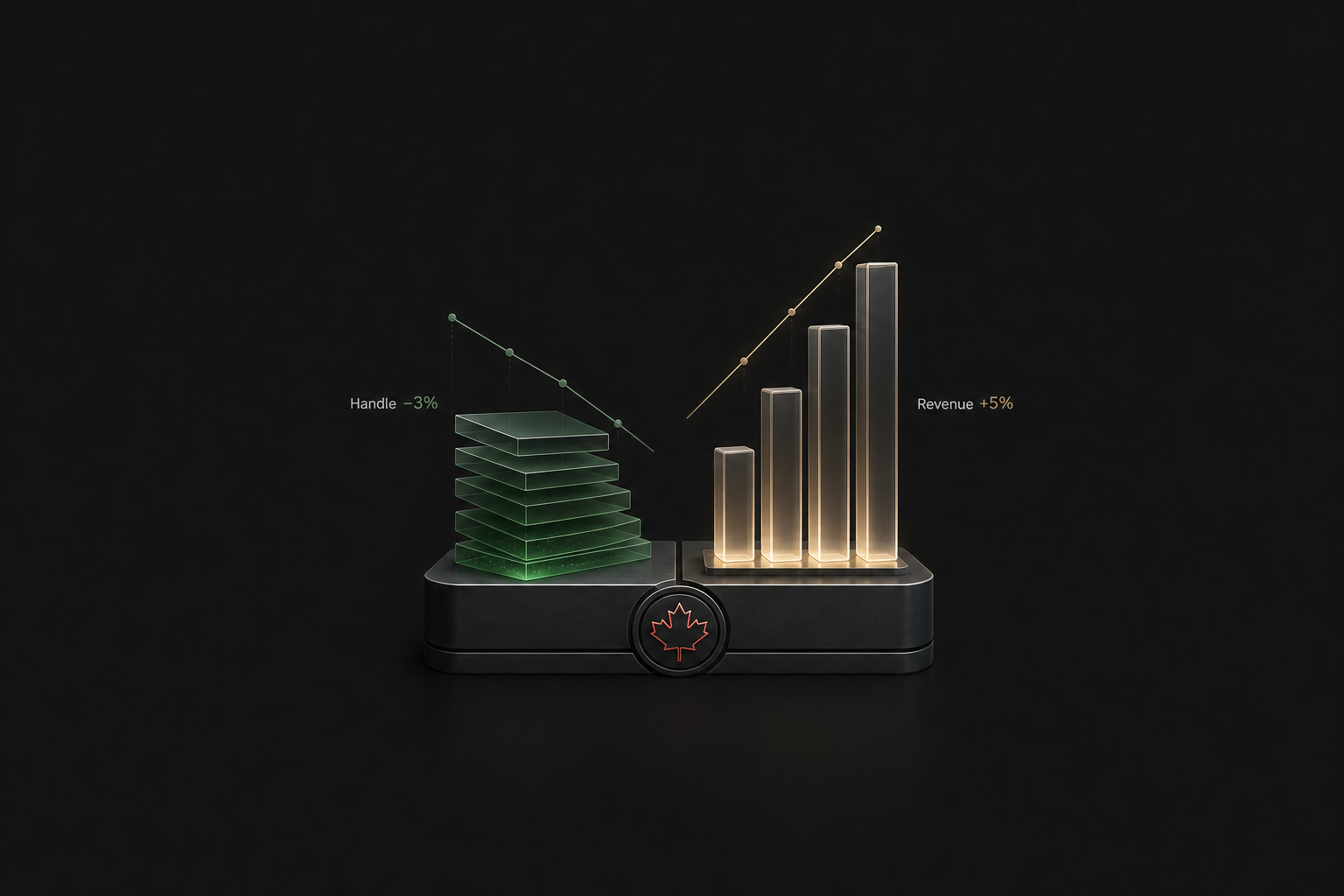

April data from iGaming Ontario shows lower betting volume but higher revenue. Blask data points to a similar slowdown in demand, making April a useful benchmark ahead of Alberta’s July launch.

According to iGaming Ontario, betting volume fell 3% in April to $6.8B, while NAGGR grew 5% to $296M. The number of active player accounts increased by 2% to 1.26M.

Gaming remained the dominant vertical, accounting for 87% of total handle. Sports betting handle fell 3% to $759M, but segment revenue rose 40% to $63M on stronger margins. P2P poker was the weakest segment, with handle down 30% and NAGGR down 24%.

By the end of May, Ontario had 44 licensed operators across 77 websites. Casumo and Conquestador exited the market in spring, while Hard Rock Digital was preparing to launch.

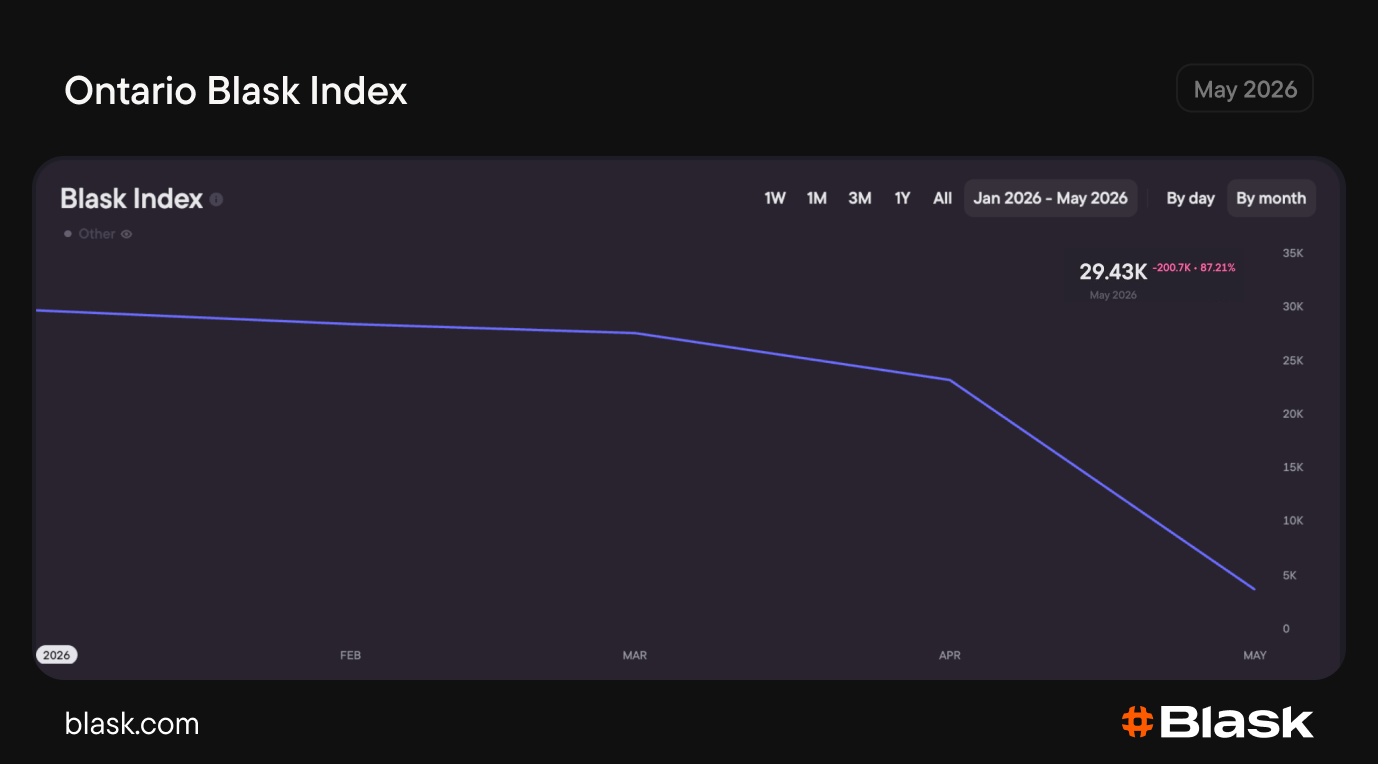

Blask data shows market maturity

Blask data shows the same cooling in demand. In April, Ontario’s Blask Index fell 4.1% MoM, while market CEB declined 1.7%, from $286.5M to $281.7M.

Both indicators moved closer to iGaming Ontario’s handle than to NAGGR. This shows the gap between demand and revenue: the market could generate less volume while earning more through margin and activity mix.

In April, Ontario’s Maturity Index stood at 12.46, pointing to a market where branded demand dominates: players more often go directly to operators rather than through broad search categories.The remaining non-branded demand is concentrated in a few verticals. In April, Online Casino, Fantasy and Lottery led category demand.

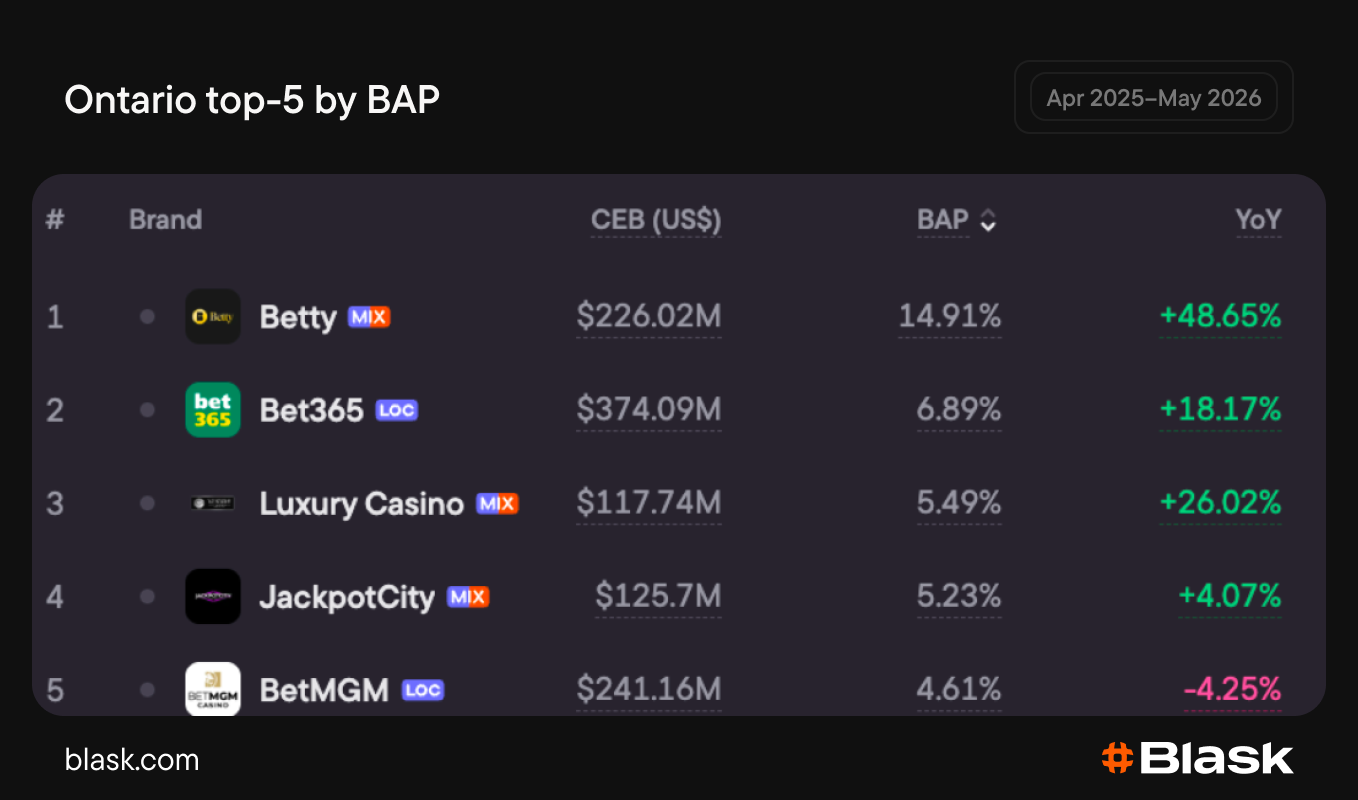

Brand ranking shows a clear split at the top. Betty leads by BAP and also posts the strongest growth among the top five, while Bet365 remains second with positive YoY and MoM dynamics. BetMGM is the only top-five brand in decline on both measures.

What this means for Alberta

For Alberta, April in Ontario is a ready-made stress test. The province’s market opens on July 13 with 30 brands, 25 of which already operate in Ontario. Blask estimates Alberta CEB at around $128M in April, while offshore operators hold most of the revenue baseline before launch.

Ontario shows that fast demand capture is not the only thing that matters after launch. In a mature phase, handle, revenue and active accounts can move in different directions.