Official statistics from the Swedish regulator record symbolic market growth of 0.8%. Blask Index points to a different dynamic.

Sweden’s gambling regulator, Spelinspektionen, reported that licensed operators earned $700M in the first quarter of 2026 — a modest 0.8% year-on-year increase. By the standards of a mature, regulated jurisdiction, the figure looks like a plateau, but Blask data points to a more nuanced reality.

A mature regulated market remains a field for redistribution of shares

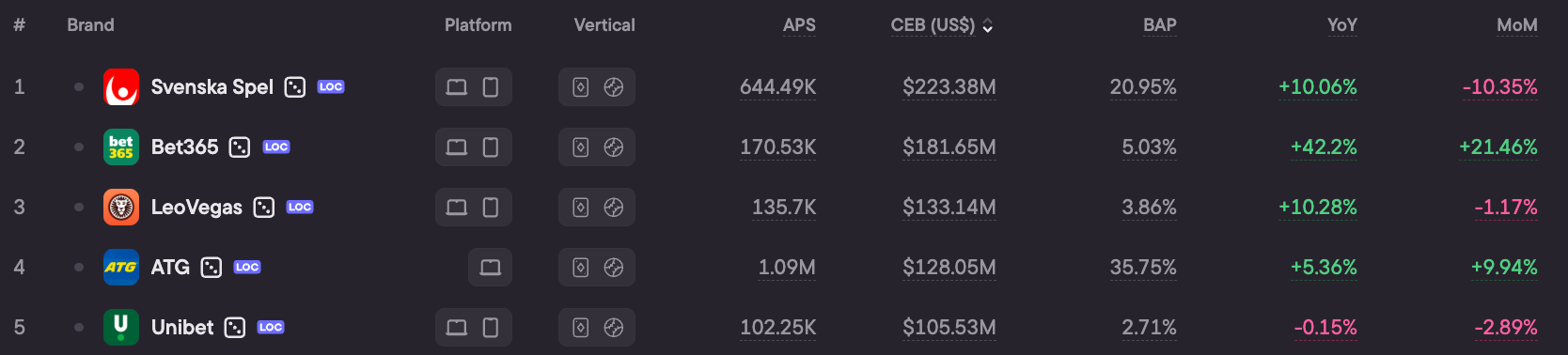

Bet365 became the main source of growth in Q1 2026: its YoY Blask Index increased by 42.25%, the highest figure among the top five operators by CEB. In absolute CEB terms, Bet365 still trails Svenska Spel: $181.65M versus $223.38M respectively, but it is growing much faster.

The shift is clear when compared with older local operators. Svenska Spel Sport & Casino and Paf have been licensed since Sweden’s gambling reform began on January 1, 2019. Bet365 entered the current licensing period in 2024, and its growth shows how an international brand is gaining momentum in a mature market still led by local players.

By the end of Q1 2026, almost 138K players were blocked through Spelpaus.se — growth of 2.6% over the quarter. This is a stable trend: every quarter, more people register in the self-exclusion register. For operators, this is a direct limitation of the addressable market.

The meaning of this dynamic for investors

Official GGR points to a near-flat Q1 for Sweden’s licensed market. Blask data tells a different story: CEB grew 11.3% and the Blask Index grew 9.7% YoY, while officially reported revenue barely moved at 0.8%.

Regulatory constraints, including the Spelpaus exclusion register, likely prevent some of that demand from converting into reported revenue. Inside the licensed segment, market-share shifts — particularly Bet365’s continued acceleration against more established local players — are the most useful indicator of where the market is heading.