The Netherlands tightened its gambling rules to protect players — and pushed the most valuable ones straight to unlicensed operators.

The Netherlands’ licensed online gambling market grew 6% in 2024, reaching €1.47B in full-year GGR. By 2025, licensed GGR had fallen roughly 18% from that 2024 baseline, according to KSA data.

Two policy changes followed in quick succession: deposit limits (€700/month for adults 25+) introduced in October 2024, and a gambling tax increase from 30.5% to 34.2% in January 2025, rising further to 37.8% in 2026.

High-value players, who generate a large share of GGR, moved to offshore operators where no caps apply. By early 2025, legal GGR channelisation had dropped to 49%.

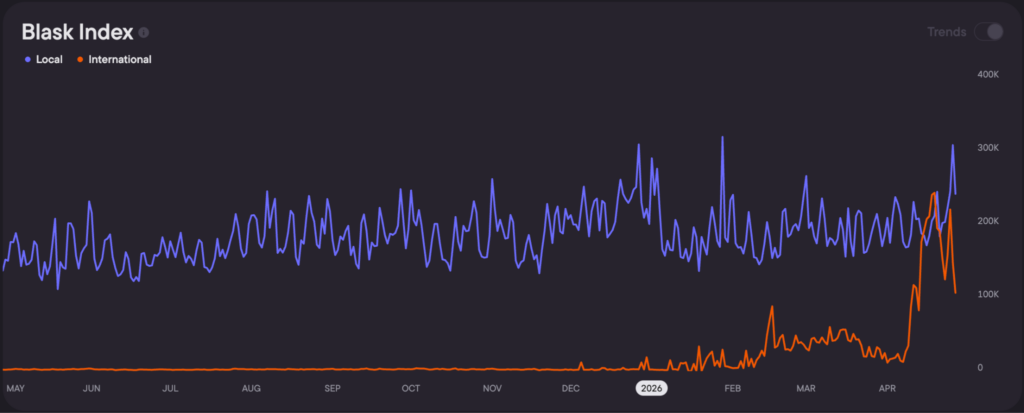

Offshore gains as Dutch deposit caps reshape demand

For most of 2025, offshore demand in Blask Index remained near zero, while licensed operators held steady. From February 2026, offshore demand increased sharply, and by April reached levels matching — and briefly exceeding — the licensed market. A signal that had stayed flat for nearly a year moved to parity within three months.

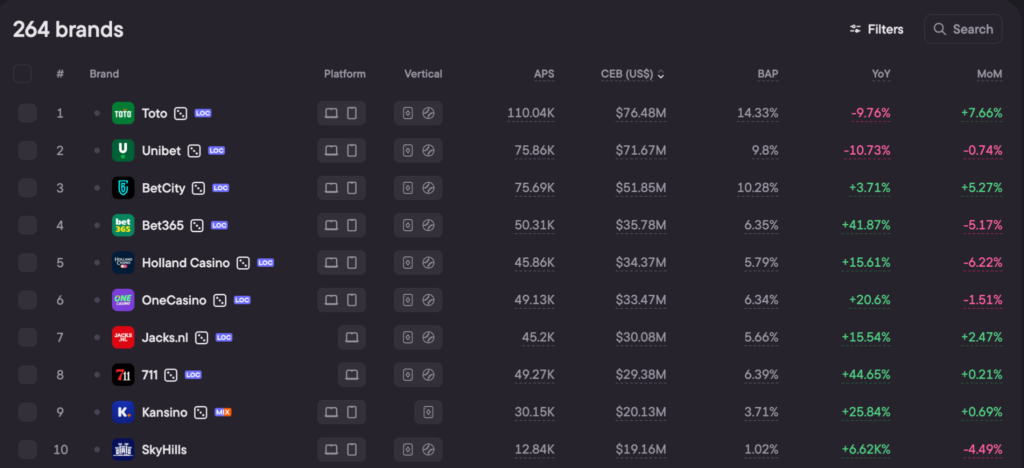

Who holds the licensed market

Three brands, Toto, Unibet and BetCity, hold 35% of player share combined. The remaining 65% is split across 261 others, none above 7%.The two largest operators, Toto and Unibet, are down year-on-year. The remaining eight brands in the top 10 are all growing, indicating a gradual de-concentration at the top (January–March 2026).

Nine of the top ten brands operate under a local licence, with only one offshore operator — SkyHills — in the group.

Headline figure misses the revenue reality

The deposit cap did not affect the market evenly. The result is a clear shift: regulation reduced licensed segment demand and redistributed it toward offshore operators. Blask data reinforces that trend, showing a visible increase in offshore demand — even as the market remains predominantly onshore.