- Updated:

- Published:

Brazil after regulation: what the data shows, and what a veteran operator sees on the ground

Ricardo Rosada — founder of BR Marketing and co-CEO of BundyBet — joins Blask CEO Max Tesla in the first episode of Signal and Noise to pressure-test Brazil’s regulated market against live data. What follows are the key points, distilled.

The result was an hour of sharp diagnostics, a live walkthrough of Blask’s Brazil analytics, and a handful of ideas that should stay with anyone building in that market.

What follows is the distilled version — no softening applied.

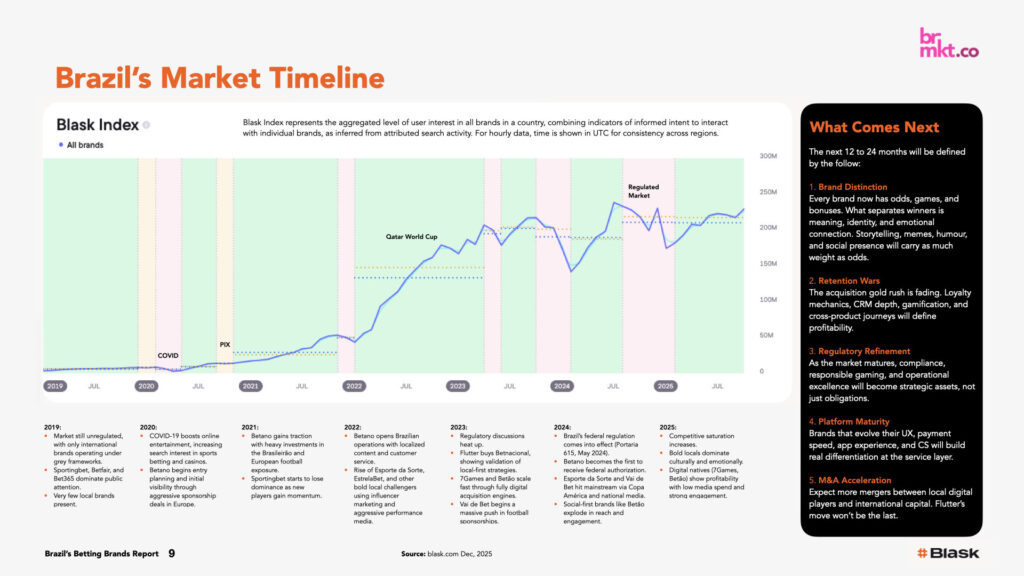

The market that regulation did not kill

Brazil’s regulated era began January 1, 2025. In the first weeks, the numbers dropped. According to Blask data published in early 2025, player engagement fell roughly 28% in January before recovering in February as licensed brands returned, players adapted, and the new payment infrastructure stabilized.

That shock was predictable. What came next was not.

By May 8, 2025 — Blask’s most active single day of the entire year — Brazil had surpassed the peaks logged during the chaotic pre-regulation months.

Blask’s AI-powered Market Explanation traced the driver: the licensed regime had restored trust and visibility, a dense football calendar provided continuous spending moments, and compliant brands finally had the infrastructure to capture that demand.

The all-time peak of Brazil’s Blask Index remains July 14, 2024 — Copa América final day — at 12.15 million daily hits. Pre-regulation. The second-highest day, October 5, 2024, also pre-regulation.

The market’s absolute ceiling was set by football events in a period with no formal framework. The regulated market has not yet touched those numbers — but the Trend line through 2025 climbed 32% from January to October, a staircase recovery that shows where the structural floor now sits.

Read more: Brazil’s betting seasons, explained — the full seasonality breakdown with Blask Index data

“2026 is not the end of the market. It’s the end of the illusion.”

This is the line that defines the episode. Rosada was not being dramatic. He was being precise.

The illusion he describes is the belief that Brazil’s iGaming market rewards improvisation — that volume alone, fueled by aggressive bonuses, influencer spend, and offshore latitude, is a viable operating model. Regulation ended that model.

Ricardo Bianco Rosada

“Compliance is not bureaucracy. It’s a competitive advantage. Budget can buy a lot of noise. Localization buys connection.”

The new cost stack (taxes, licensed payment rails, mandatory KYC, local customer support) eliminated the margin for operators running on structural shortcuts. Companies that had not built operational discipline found themselves exposed.

Max Tesla put it from the data side: “Regulation never kills the market. It kills the improvisation.” The market did not contract permanently — it self-selected.

Three forces shaping Brazil in 2026

Rosada named three structural forces that define the competitive environment this year.

- Regulation and consolidation. The first year filtered who belongs. Brands that came through 2025 intact now have a foundation. Those still improvising are on borrowed time.

- The pressure to be profitable. Free-spending acquisition cycles are over. Taxes are real. Customer support teams cost money. Every cost that was once hidden in an offshore structure is now visible. “Everything becomes more expensive,” Rosada said. “You have a lot of pressure to be profitable.”

- Changing customer behavior. Brazilian players in 2026 are more informed than in 2025. They understand what a good product looks like. They test fast and leave faster. “If they don’t like, they go away. They won’t come back. You have to take care of your product.”

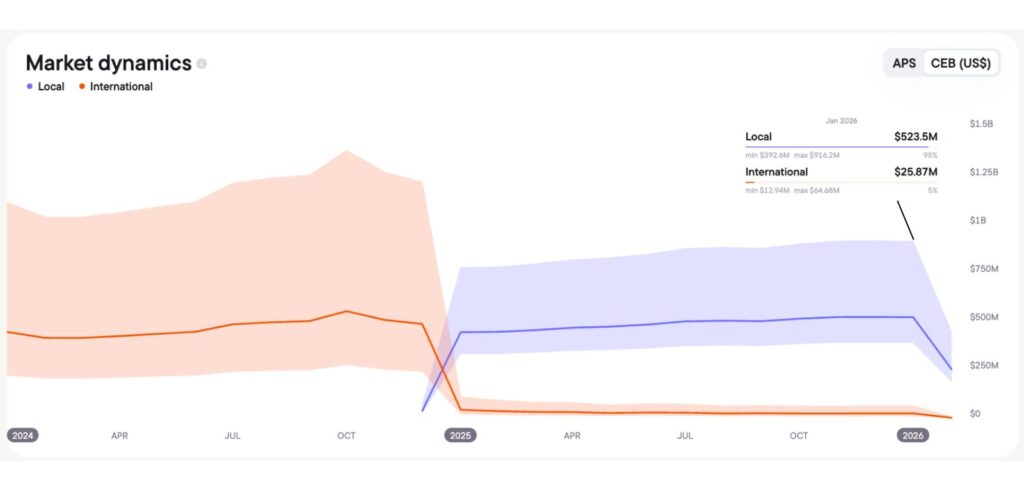

The illegal market: still present, harder to measure than it looks

Blask currently tracks 580 operators in Brazil — licensed and unlicensed. As of early 2026, roughly 78 companies hold formal licenses, generating approximately 138 active brands and an estimated $7 billion CEB in 2025.

According to iGamingBusiness.com, illegal operators hold between 41% and 51% of the total market. Rosada places his estimate at 30–40%, but acknowledges the structural measurement problem: many offshore operators rotate domains, making URL-based tracking unreliable. “They jump from DNS to URL to URL. It’s very hard for any tool to understand who those guys are.”

What Blask’s data does show clearly: as of January 2026, 95% of the Competitive Earnings Baseline — Blask’s metric for estimated revenue extraction — is attributed to locally licensed operators.

Twelve months earlier, the split was far less defined.

Rosada sees the enforcement path as financial.

“Follow the money. Understand which payment providers are serving illegal operators. Block those providers. You will never have zero illegal market, but you can diminish it significantly.”

Brazil already has legislation mandating that payment processors be regulated. Enforcement is the missing variable.

Free report: Brazil’s top 20 operators in 2025 — the brands setting the pace after regulation

Who moved in the rankings — and why

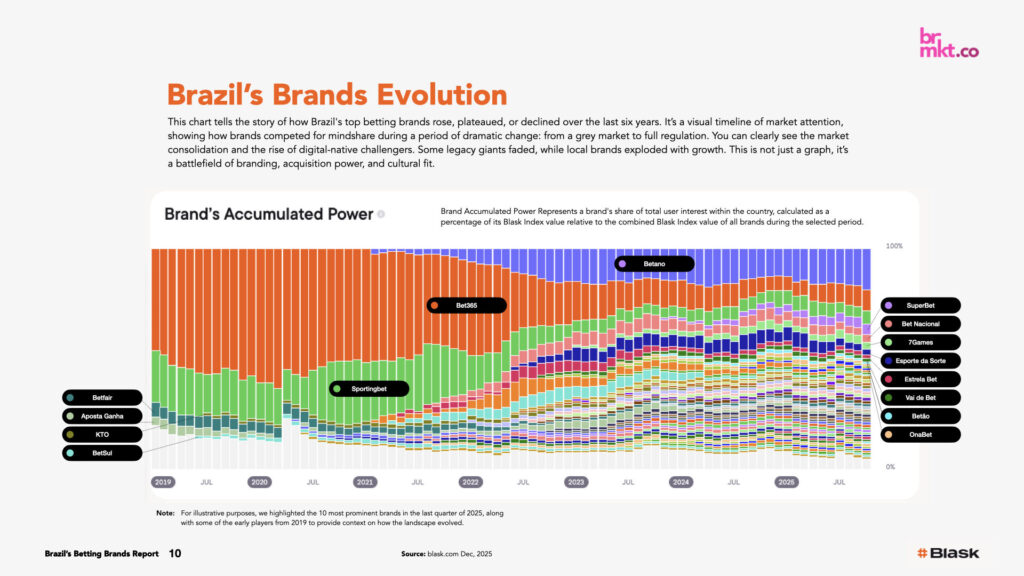

Among the clearest market signals Blask displayed live during the episode: over the past year, only two operators in Brazil’s top 10 changed positions. SportyDaSorte fell from second place to sixth. Superbet rose from sixth to third.

Rosada on SportyDaSorte: not a decline in capability, but deliberate diversification. They hold two brands in the top 10 and launched a third at the end of 2025. “Don’t overestimate this as weakness. They know what they’re doing. It’s a course correction.”

On Superbet’s rise, he was direct: “Discipline and investment. They introduced a social feature where players can share bet slips — a copy-trade mechanic applied to sports betting. Their operation is organized. That’s not luck.”

The pattern embedded in both movements: the operators winning in Brazil are not winning on any single lever. They are executing systematically across product, CRM, and brand.

Retention: the part of the funnel nobody manages well enough

If there is one consistent blind spot Rosada sees across operators in Brazil, it is retention. Not the absence of CRM tools — FastTrack, OptiMove, and Smartico are all strong — but the absence of operator competence with those tools.

“A lot of people don’t take a close look at frequency — how customers bet, deposit, withdraw. They think AI will handle everything. If they got closer to frequency data, churn prediction would be much easier.”

The signal that marks an operator as a tourist: “They talk a lot about cost of acquisition and ignore retention.” The tell is consistent.

The reason retention is structurally underweighted is partly psychological. Acquisition spend feels like growth. Retention spend feels like maintenance. In a market moving as fast as Brazil’s in 2024, the distinction seemed academic. In 2026, with profitability pressure real and welcome bonuses banned, retention is the defining variable.

“Inertia can bring you volume,” Rosada said. “Strategy brings profit.”

Sports and casino are not the same audience

A distinction that does not appear often enough in market analysis: sports bettors and casino players are not the same people using different products. They are psychologically different customers.

Sports is event-driven and emotional, with peaks tied to match schedules. Casino is routine and frequency-based, with a different relationship to time and risk. “You cannot compare,” Rosada said. “If you think a sports player will become a casino player because you’re sending CRM campaigns, you’re wrong.” His estimate: roughly 20–25% of players participate in both verticals. The rest should be approached on their own terms.

This also explains the rapid growth of crash games — BGSoft’s catalogue specifically — in Brazil. Crash sits between categories: it has the simplicity that appeals to sports bettors and the frequency dynamic that casino players understand. It was a product designed for the Brazilian customer before most operators acknowledged that Brazilian customers were distinct.

Free report: Brazil games: player demand and lobby placement across 500+ casinos — GVR vs. SoI data

What a strong brand actually looks like in Brazil

Rosada’s framework for strong brands is specific: clarity, trust, consistency. Not size, spend, or creative ambition.

“You can copy the visual identity. You can copy the structure. But you will never copy the tone of voice, the value proposition, the way promotions are built. The community around the brand — that cannot be transferred.”

Betano is his model for what international brands can achieve: “They basically became a Brazilian brand. They hired local talent, they spent to understand the market, they found the right path.” Bet365’s trajectory is the counter-example. Once dominant in Brazil, now declining — not because it is weak globally, but because it did not adapt locally. Same assessment for Sportsbet.io.

Global scale does not translate automatically into local relevance. Rosada calls full product localization “tropicalization” — a term the industry resists, and one he uses anyway. “The product is never ready. Especially in Brazil.”

The brands that will build durable positions in 2026 are not the ones spending the most. They are the ones building community — what Rosada, citing Patrick Hanlon’s Primal Branding, calls a “movement”: a brand with a creation story, rituals, icons, and believers. “Companies that build a community around them are the ones that will succeed. For sure.”

The seasonality the data confirms

On Blask’s seasonality panel — drawing on data from 2016 — the pattern is consistent: December ranks first, October second, November third. February is last, by a significant margin.

The logic is structural. October carries Libertadores semifinals, decisive Brasileirão rounds, and FIFA international windows stacked on a public holiday. February is shorter, Série A hasn’t started, and Carnival shifts attention away from regular sports content entirely.

The market is currently in a falling trend that began in November 2025 — Copa Libertadores and Série A concluded, a record-prize mega-devirata lottery captured leisure spending, and enforcement actions against unlicensed sites added further disruption. This is expected. Historically, March through May begins the recovery: Brasileirão returns, Copa Betano provides consistent calendar, and the market starts climbing again.

Plan for it. It’s in the graph every year.

Read more: Brazil’s betting seasons, explained — how to time campaigns around the annual demand cycle

Speed, product, and the myth that marketing can compensate for weakness

The episode closed with a direct exchange. Myth or truth: marketing matters more than the product in Brazil.

Rosada: myth. “Marketing accelerates your exposure. But once people realize what you have, they will leave. A good product retains customers. That is the only real leverage.”

The corollary: speed matters, but it cannot substitute for substance. “Speed beats perfection” holds in terms of timing — launch early, learn from real users, iterate in market. It does not hold if speed means launching something broken and hoping nobody notices. “Fake it till you make it? No. Fake until you fake. People realize. You cannot fool someone for a long period of time.”

Brazil tests products faster than most markets. It forgives less.

What 2026 actually demands

Ricardo Rosada spent seven years advising operators on Brazilian market entry. He co-built an operation inside a major media group. He has watched international brands arrive with confidence and budget and leave with neither.

His summary of what 2026 demands is not a framework. It is a threshold.

“If you can’t maintain an active player for 90 days, you have a problem. If you’re not building a community around your brand, you’re building something that someone else can immediately replace. If you’re not looking at retention data, you’re optimizing for the part of the business that does not determine whether you survive.”

Regulation did not make Brazil easier. It made it more honest. The operators who read that as an opportunity are building something durable. The ones who read it as bureaucracy are running out of runway.