- Updated:

- Published:

European iGaming market outlook 2026: where demand is growing

Blask data across six major regulated markets — the UK, Italy, Germany, Spain, France, and the Netherlands — reveals sharply diverging paths heading into 2026, offering a useful snapshot of broader iGaming industry trends 2026.

Europe’s regulated iGaming market is not one market. It’s six different regulatory frameworks, six different competitive landscapes, and six different answers to the same question: where is demand actually going?

Blask tracked player demand across all six major regulated markets through 2025. The data shows one market accelerating faster than the rest, one caught in a regulatory paradox, and one where illegal supply is eroding the licensed base. Before operators and analysts project 2026, it’s worth understanding what 2025 actually looked like.

What the data measures

- Blask Index is a demand signal built from search activity across iGaming brands. It captures how much player attention a brand generates in a given market — before that demand converts to bets or deposits. It’s a leading indicator, not a lagging one.

- Competitive Earning Baseline (CEB) translates that demand into a revenue benchmark: what a brand should be earning, given its competitive position. CEB is always reported as a min–avg–max range, because market conditions create a spectrum of plausible outcomes. The average is the most likely scenario; the range reflects conservative to favorable competitive assumptions.

- Acquisition Power Score (APS) estimates how many new customers a brand’s position implies, month by month. Like CEB, it’s a range — seasonal swings and campaign timing affect the floor and ceiling.

Together, these metrics give a market-level picture that GGR data alone can’t provide. GGR is reported quarterly, by license holders, with a lag. Blask Index moves in real time across all brands simultaneously.

The European picture in 2025

Any discussion of the top iGaming markets 2026 has to start with Europe’s regulated core. In 2025, the six markets combined — the UK, Italy, Germany, Spain, France, and the Netherlands — generated an estimated $27.1 billion in total CEB, alongside 52 million newly acquired players across the licensed base on an APS average basis. That is the aggregate picture.

Below the surface, the markets are moving at very different speeds.

| Market | Blask Index 2025 | CEB 2025 (avg) | CEB YoY | APS 2025 (avg) | APS YoY |

|---|---|---|---|---|---|

| United Kingdom | 586.7M | $11.52B | +10% | 19.85M | +11.8% |

| Italy | 393.0M | $5.97B | +20.7% | 13.51M | +7.6% |

| Germany | 196.4M | $2.54B | –2.8% | 8.39M | +56.4% |

| France | 63.9M | $3.00B | — | 2.89M | — |

| Netherlands | 68.8M | $2.26B | — | 3.08M | — |

| Spain | 107.0M | $1.76B | +14.2% | 4.47M | +5.0% |

The UK leads by every measure. Italy follows at a distance but is closing the gap faster than any other market. Germany presents the most counterintuitive picture: player acquisition surged 56%, but estimated revenue declined.

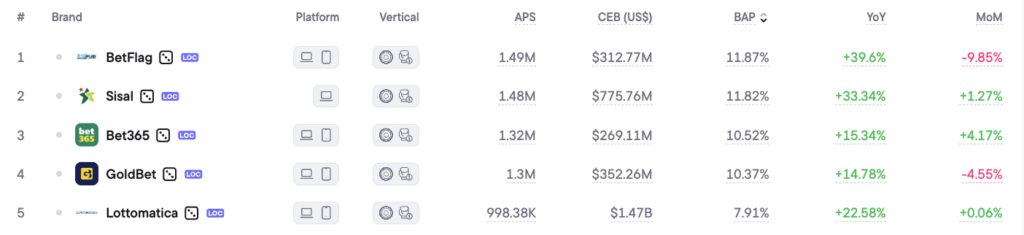

United Kingdom: steady growth, shifting brands

The UK remained the dominant iGaming market in Europe in 2025. Total Blask Index reached 586.7 million, with CEB growing 10% year-on-year to $11.52 billion ($8.39B–$20.9B range) across 335 active brands.

The headline figures are steady. What’s more revealing is what’s happening inside them.

Bet365 held the top position with a CEB of $1.31 billion ($979M–$2.29B) and grew 15% year-on-year. Ladbrokes, ranked third, grew faster — up 21.88%. William Hill, the number two brand by CEB, fell 12.63%. The market isn’t growing uniformly: brands that invested in brand visibility and product are pulling away from those that didn’t.

The UK Gambling Commission’s data published in February 2026 shows GGR trending up through December 2025, consistent with Blask’s demand signals. With the Gambling Act 2005 review still working through implementation, 2026 will see continued pressure on bonusing and affordability checks — both of which affect acquisition efficiency rather than market size.

The UK market is mature but not saturated. Annual APS of 19.85 million new customers in 2025 was up from 17.75 million in 2024 — meaningful growth in a market where every incremental player is harder to acquire.

Italy: the fastest-growing major market in Europe

Italy stands out not just as the story of 2025, but as one of the fastest growing iGaming markets in 2026 to watch from a European demand perspective.

CEB grew 20.7% year on year to $5.97 billion ($4.43B–$10.58B range), against a Blask Index of 393 million — the second-highest figure in Europe. Player acquisition reached 13.51 million.

Italy recorded €3.33 billion in online player spending in 2025, the highest figure the market has ever seen. Casino, poker, and bingo all posted records. The drivers are structural: Italy’s ADM (Agenzia delle Dogane e dei Monopoli) completed a new licensing round in 2024–2025 that cut the number of active brands by roughly 45%. Fewer operators, cleaner competitive field, higher per-brand investment.

The two brands that benefited most are BetFlag (CEB avg $294M, up 33.19% year-on-year) and Sisal (CEB avg $742M, up 34.67%). Both are domestic operators who consolidated demand as smaller international brands exited the licensed market.

Italy’s Blask Index is now two-thirds the size of the UK’s — remarkable for a market that, until recently, was considered a distant third behind Germany. From a demand perspective, Italy and the UK are operating at a different level than the rest of continental Europe.

Live Dealer continues to drive the casino category. Blask’s category data shows Live Dealer demand in Italy at 240K index units (most recent period), ahead of Online Casino (70K). Game shows, blackjack, and roulette dominate within live. Football betting remains the biggest single category, but the casino vertical is where growth is concentrated.

Germany: more players, less revenue

Germany posted the most counterintuitive numbers in Europe in 2025. APS grew 56.4% year-on-year to 8.39 million — the strongest acquisition growth of any major European market. CEB, however, fell 2.8% to $2.54 billion ($1.63B–$5.27B range).

More players, less revenue. The explanation is regulatory.

Germany’s Glücksspielneuregulierungstaatsvertrag (GlüNeuRStV), which came into force in 2021 and has been amended since, caps monthly online casino deposits at €1,000 per player and mandates a €1 per spin stake limit. The regulation successfully channeled players from offshore to licensed operators — hence the APS surge. But the revenue per player is structurally compressed.

A Handelsblatt Research Institute report from November 2025 flagged that the black market in Germany remains substantial, with a significant share of gambling activity happening outside licensed channels. The regulatory framework is limiting licensed revenue without eliminating unlicensed alternatives.

The top two brands in Germany illustrate the market’s structure. Tipico, the longtime leader, holds CEB of $408 million but grew just 2.61%. NV Casino, launched in late 2024 and ranked second by CEB, generated $365 million with no prior year for comparison. New entrants are winning share not through long-term brand equity, but through performance marketing and product positioning within tight deposit constraints.

Germany updated its Interstate Treaty language in 2025 to address deposit limit inconsistencies. Whether the next iteration relaxes constraints enough to unlock revenue growth is the critical 2026 question.

Read more: Germany iGaming market 2026: $3B, 347 brands, and a regulatory war nobody is winning

Spain: steady, local-brand rotation

Spain delivered consistent but unspectacular growth in 2025. CEB reached $1.76 billion ($1.31B–$3.12B range), up 14.2% year-on-year. APS grew to 4.47 million, a 5% increase over 2024. Blask Index stood at 107 million across 112 active brands.

The standout is the brand rotation at the top. Bet365, historically dominant, fell 8.25% year-on-year. Sportium, the domestic betting brand, grew 4.57%. The Spanish market is gradually shifting toward local operators, consistent with what happened in Italy over the past five years.

Spain’s regulator, the DGOJ, maintains a relatively clean licensed environment with product restrictions on advertising. Those restrictions limit acquisition spend but also reduce the wild growth and contraction cycles that characterize less regulated markets.

Read also: Spain iGaming market overview: Maturity meets momentum

France: the sports-only ceiling

France generated a Blask Index of 63.9 million in 2025 — modest relative to market size — and CEB of $3.0 billion. That CEB figure looks high compared to Spain until you factor in France’s market structure: online casino is not licensed in France. The market runs entirely on sports betting, horse racing, and poker.

Gross gaming revenue in France was €5.7 billion in H1 2025, up 3.5% year-on-year. That’s a stable performance driven by sports betting growth rather than product expansion. ParionsSport (owned by FDJ) leads the market, with Betclic second.

The absence of online casino creates a structural ceiling on both Blask Index and per-operator CEB. France’s GGR-per-Blask-unit ratio is the highest of any European market, precisely because sports-only products generate disproportionate revenue relative to search demand. That dynamic is unlikely to change in 2026 unless France opens online casino — a debate that periodically surfaces but has yet to produce legislation.

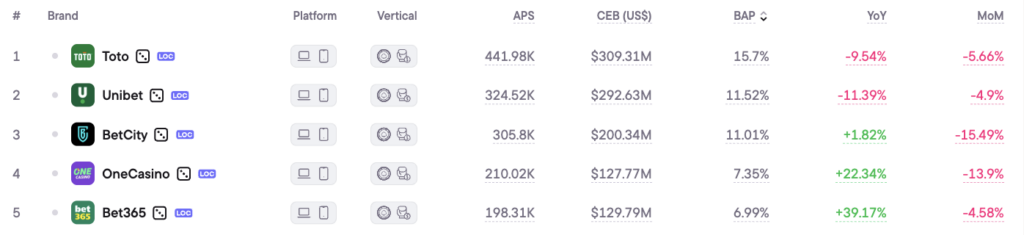

Netherlands: a market under regulatory pressure

The Netherlands opened its licensed online gambling market in October 2021. By 2025, the market had 174 active brands and Blask Index of 68.8 million, close to France in demand terms. CEB averaged $2.26 billion ($1.59B–$4.26B range).

The signal for 2026 is less encouraging. Dutch regulator KSA flagged a 16% decline in GGR in H1 2025 compared to H2 2024, alongside a rise in illegal gambling activity. The licensed market is struggling to retain players who find unlicensed options less restrictive.

Toto, the market leader, saw Blask Index fall 4.18% year-on-year. Unibet holds second position. The market structure is relatively concentrated compared to Italy or Germany — fewer active operators, lower total demand — and the regulatory tension between harm reduction and market attractiveness is unresolved.

Netherlands is the clearest European example of what happens when licensing is strict but enforcement of illegal alternatives is weak: licensed revenue contracts while total gambling activity doesn’t.

What 2026 looks like from the demand side

Six markets, six different stories. What the Blask data makes clear about iGaming market growth by region is that regulated markets perform best when broad product access is matched by a licensing regime that genuinely channels demand toward licensed operators rather than away from them.

- Italy is the benchmark. A reduction in operator count, clear product rules, and effective enforcement of the licensed market produced the strongest CEB growth in Europe in 2025.

- Germany has the players but not the revenue. The gap between APS growth (+56%) and CEB growth (–3%) is the regulatory premium paid by the German market. The 2026 Interstate Treaty update is the variable to watch.

- The UK remains the European market of reference — mature, well-regulated, and still growing at 10% CEB annually. The brands that are winning are the ones investing in demand, not just managing existing share.

For operators mapping their European strategy in 2026, the data points to two priorities: Italy for growth, and Germany for player acquisition optionality pending regulatory evolution.