- Updated:

- Published:

Spain iGaming market overview: maturity meets momentum

Blask’s view of a mature Western European market where football remains the primary demand engine.

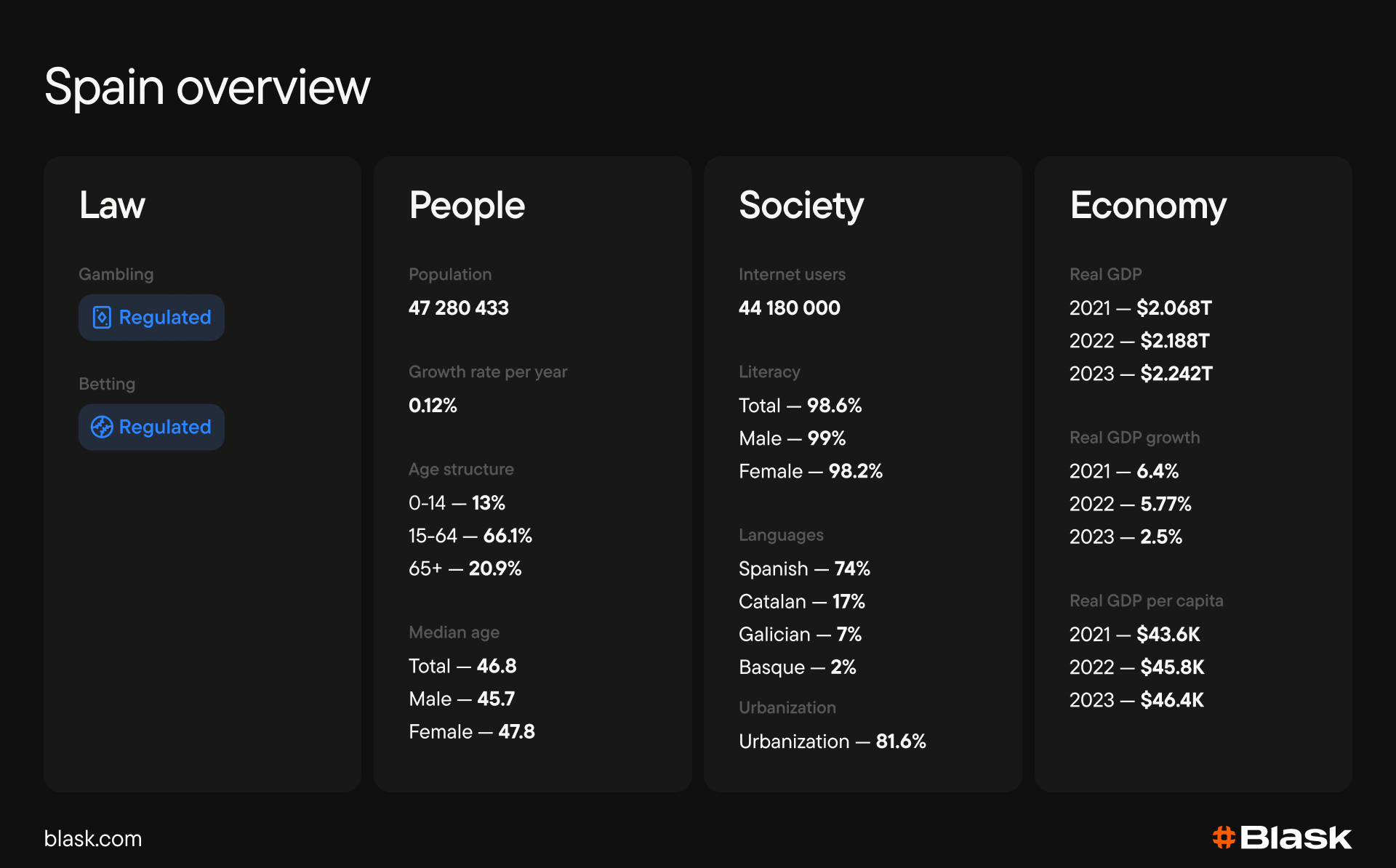

Spain’s regulated online gambling market hit $1.7B GGR in 2024 (+17.6% YoY) — its best year since Law 13/2011 launched the regime. Blask ranks the country #22 globally by CEB ($1.6B), with 114 active brands and Blask Index that climbed +13% through 2025. The narrative: maturity with momentum.

The April 2024 Supreme Court ruling restored welcome bonuses, operators poured €526M into marketing, and domestic challengers like Luckia (+34.6% YoY) started eating into Bet365’s lead. What comes next is tighter responsible gambling rules and a fight for share among the licensed elite.

Compare Spain’s late-2025 trends with nine other European markets in the Europe iGaming Pulse PDF.

Macro context and demand: Football-driven demand in a digital market

Spain is Western Europe’s fourth-largest economy, with 47.3 million people and 96% internet penetration. Social media reaches 89% of adults, and the country’s football obsession translates directly into betting behavior. 55% of players engage with traditional sports, with La Liga fixtures driving predictable weekly spikes.

Surveys show 40% of sports bettors play because it “makes sport more exciting,” while 44% cite earning money. Casino players follow a similar pattern — process enjoyment (35%) and adrenaline (28%) rank alongside financial motivation.

The rules of the game: DGOJ, taxes and the enforcement wave

A brief timeline

- 2011 — Law 13/2011 (Spanish Gambling Act) establishes DGOJ as the national regulator; initial GGR tax set at 25%.

- 2018 — GGR tax reduced to 20%; shared poker liquidity with France and Portugal launches.

- 2020 — Royal Decree 958/2020 imposes strict advertising restrictions, including welcome bonus prohibition.

- 2023 — Royal Decree 176/2023 mandates safer gambling environments and risk detection mechanisms.

- April 2024 — Supreme Court Ruling 527/2024 nullifies key articles of RD 958/2020, effectively reinstating welcome bonuses. Active players surge 21.7% within months.

- 2025 — New data reporting model in effect (March). Joint deposit limit system and standardized risk detection algorithm under development.

Taxes and cost of entry

GGR tax sits at 20% on gross gaming revenue, reduced to 10% for operators tax-resident in Ceuta or Melilla. Player winnings face taxation starting at 19%, with SELAE/ONCE lottery wins over €40,000 subject to 20% withholding. General license applications cost €38,000, singular licenses €2,500 per activity, and corporate tax runs at the standard 25% rate. Gambling activities are VAT-exempt.

Licensing and enforcement

The DGOJ operates a tiered system: General Licenses (10-year validity, renewable) authorize broad gambling categories, while Singular Licenses (3–5 years) cover specific activities like sports betting or roulette. Licenses are awarded through periodic public tenders announced by the Ministry of Consumer Affairs.

In 2024, enforcement intensified dramatically. The DGOJ imposed €142 million in total fines, including €77.4 million in H2 alone — fourteen unlicensed operators were blocked and banned for two years, while eleven licensed operators received €2.4 million in penalties for technical violations. The regulator closed 240 illegal gambling websites in 2023 and maintains active monitoring through its fraud prevention service.

How many operators are active now?

Blask identifies 114 active brands in Spain, the top 10 all hold DGOJ licenses. By vertical, the market strongly favors combined sports + casino operators, pure-play brands are rare exceptions.

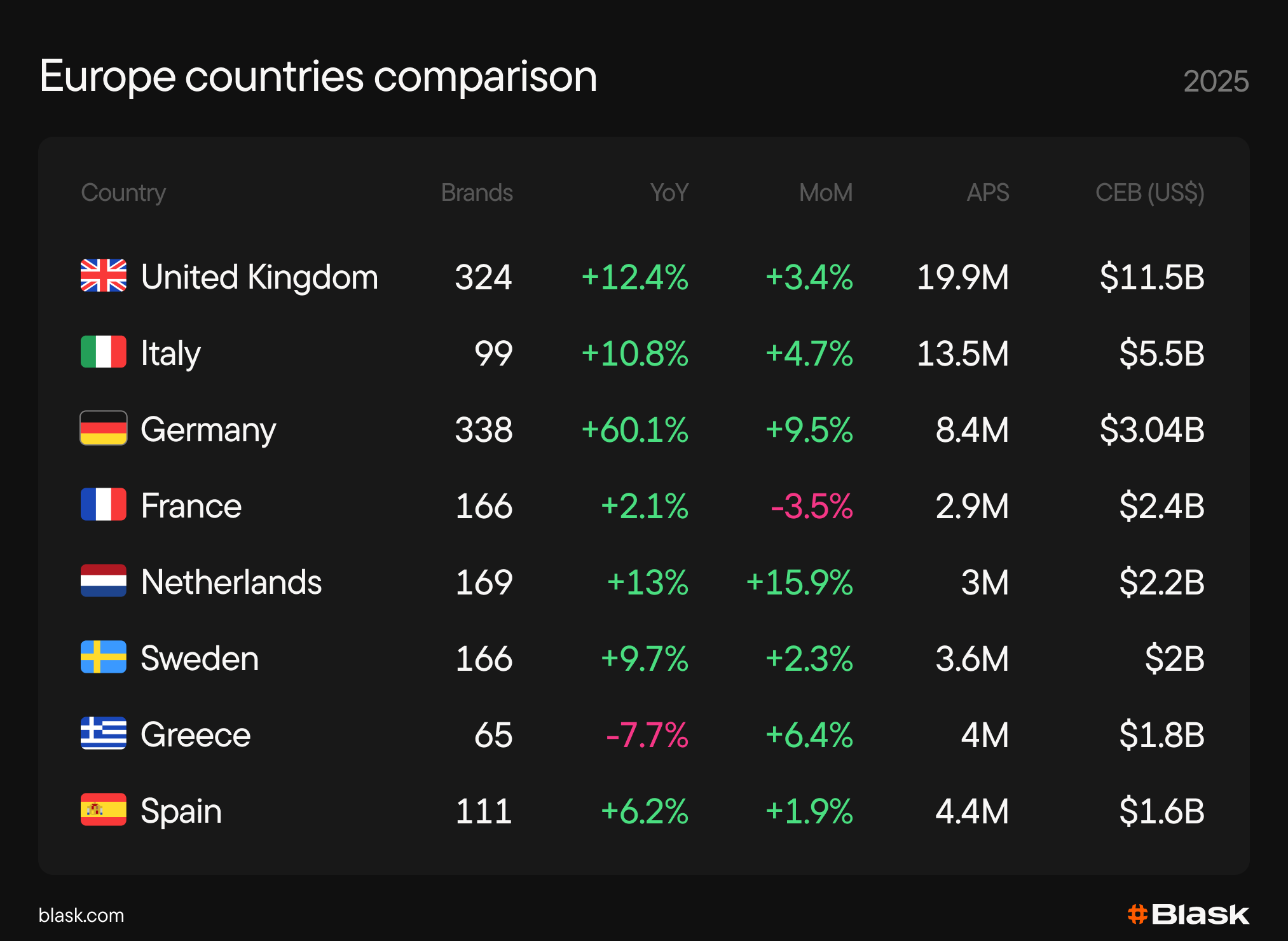

Where Spain ranks globally: European mid-tier

Blask views markets through the lens of potential revenue and statistically attainable acquisition at current brand strength.

For January–December 2025:

- CEB (avg) — Spain ranks #22 worldwide at $1.6B, positioned in the Western European mid-tier alongside Sweden (#20, $1.98B), Greece (#21, $1.82B), and Ireland (#23, $1.57B). The country trails the UK, Germany, Italy, France and Netherlands but outperforms Belgium and Portugal.

- APS (avg) — Spain commands 4.43M monthly acquisition potential, reflecting mature player acquisition dynamics in a saturated market.

Year-over-year CEB growth of +6.19% demonstrates resilience, month-over-month (November–December 2025) momentum of +1.85% suggests steady rather than explosive expansion.

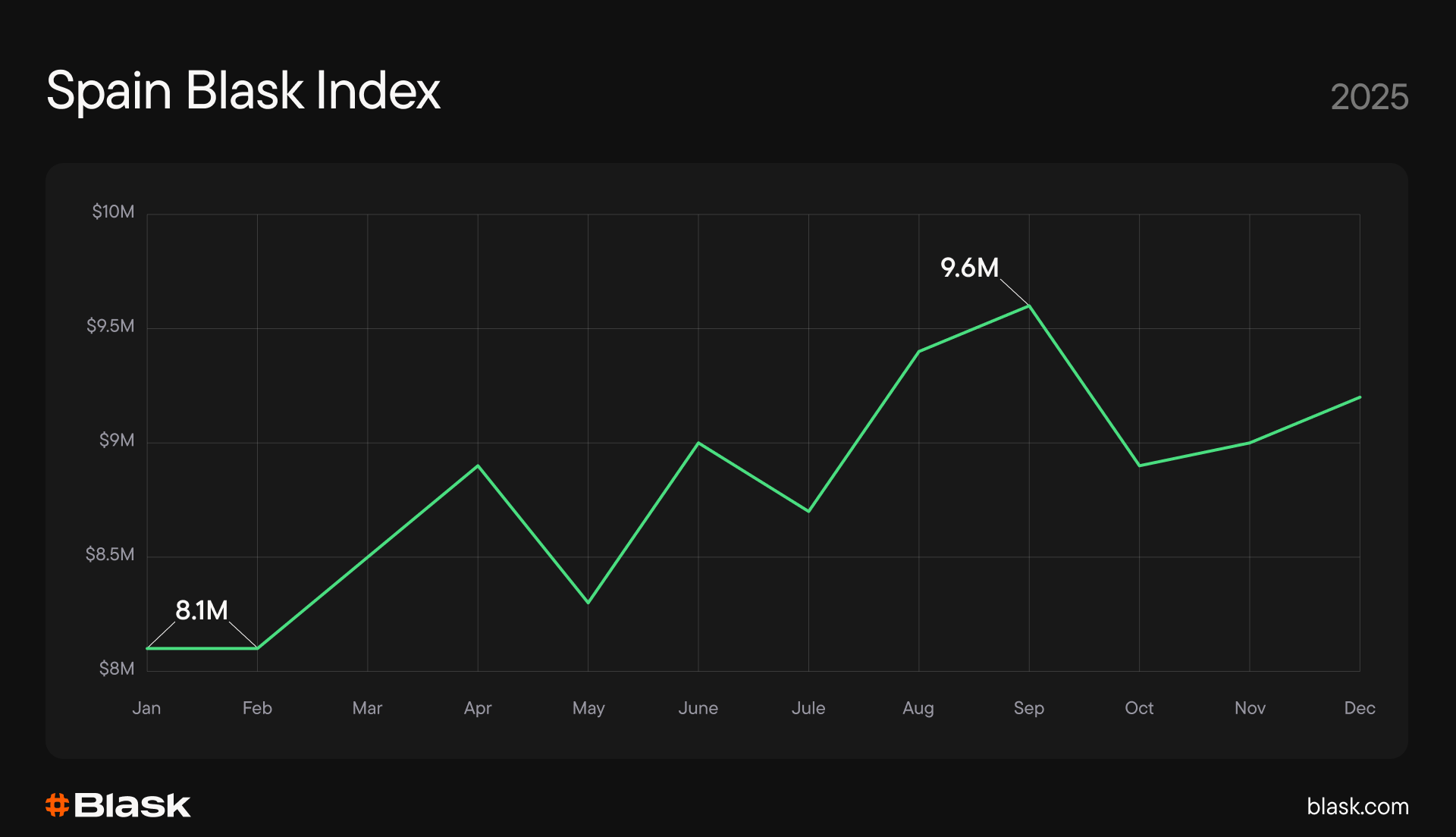

Blask Index: Steady climb through football season

The Blask Index rose from 8.12M in January 2025 to 9.19M by December — a gain of +1.07M (+13.2%). The trajectory reveals a classic European football seasonality pattern: steady growth through winter, a dip during summer (June–July), acceleration as La Liga resumed in August.

The August reading of 9.37M represented the year’s operational peak, coinciding with the La Liga season opener and UEFA Champions League qualifiers. September sustained attention (9.55M) as El Clásico anticipation built.

Market structure and share shifts: Bet365’s grip loosens

Of the 114 active operators, only the top 11 hold more than 2.5% BAP each. Consolidation is visible in 2025: in January, brands outside the top 10 together accounted for 3.13%; by December their combined BAP had compressed to 2.4%.

Leader movements in 2025

- Bet365 remains dominant but lost ground. The leader’s erosion benefited second-tier challengers.

- Codere climbed from #4 to #2, holding steady while others shuffled.

- Sportium slipped slightly, now tied with Codere.

- bwin was a steady top 5 performer.

- Luckia surged +34.57% YoY to claim 6.29% BAP — the year’s breakout domestic brand.

- CasinoBarcelona exploded +57.74% YoY to reach 3.68%, emerging from outside the top 10 to become a serious contender.

- Betfair and Betway struggled: -12.41% and -11.05% YoY respectively, suggesting exchange-focused and UK-centric brands face headwinds against localized competitors.

Domestic challengers with aggressive localization (Luckia, CasinoBarcelona) are gaining at the expense of international brands assuming automatic translation of their strength.

APS and CEB in 2025: The capacity curve

Across January–December 2025, Blask panels show:

- APS: Min 260.6K / Avg 369.5K / Max 670.3K

- CEB: Min $95.4M / Avg $133.2M / Max $242.5M

The year opened from a modest base, with APS averaging 347.4K in January and CEB at $127.2M. Spring brought measured recovery as welcome bonus campaigns ramped. Summer saw a steady climb on the football calendar, peaking in September (APS 391.4K, CEB $137.4M). By December, both metrics were near yearly highs: APS 383K, CEB $138.6M.

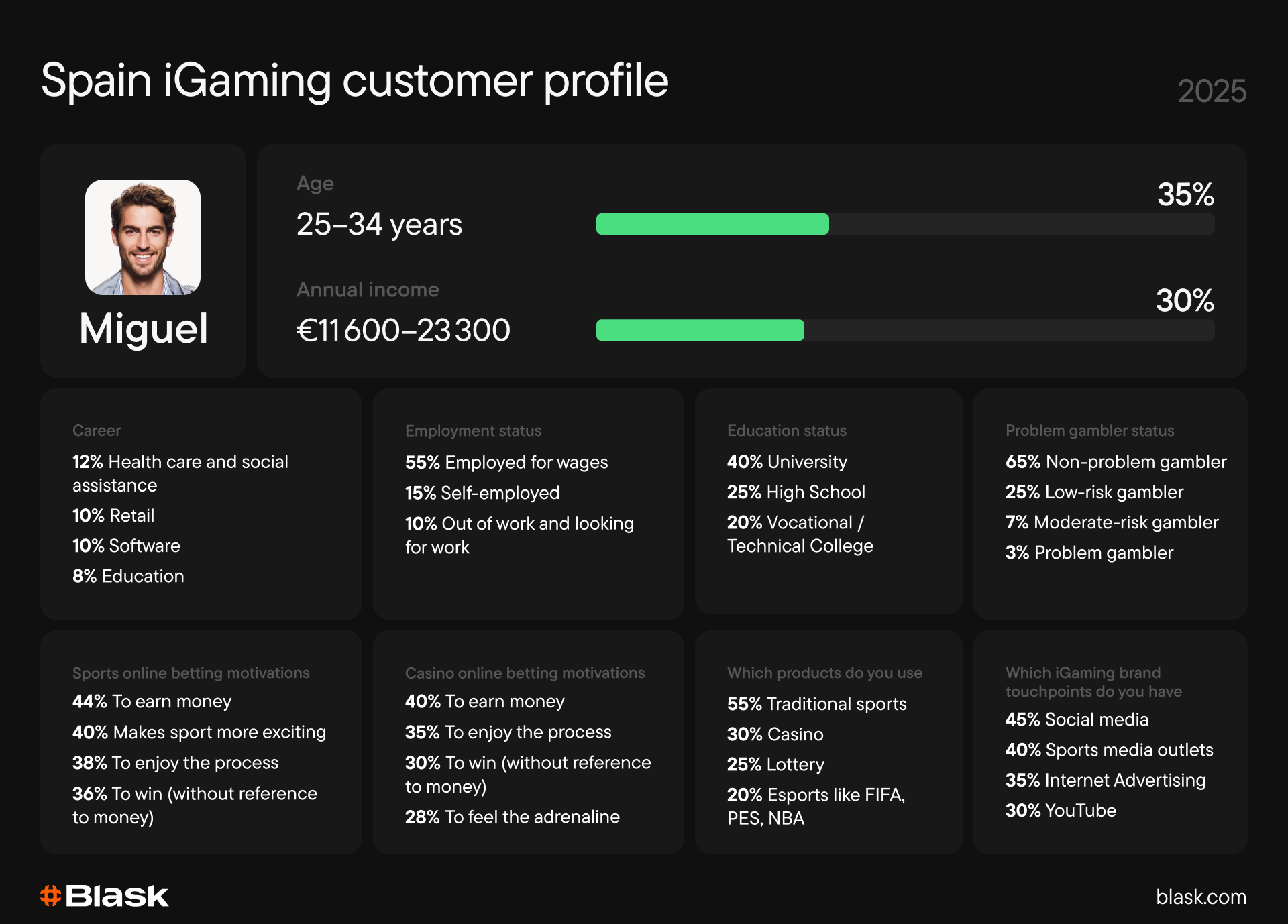

The Spanish consumer: Young, educated, football-obsessed

The typical Spanish iGaming customer is a university-educated male under 35, earning a modest €10,000–€30,000 annually — reflecting the broader Spanish economic context. The motivation split is telling: sports bettors play primarily to enhance the viewing experience and support their team, with money a secondary driver; casino players lean more toward adrenaline and process enjoyment.

Discovery happens digitally: social media and sports media outlets dominate the acquisition funnel, with YouTube and internet advertising rounding out the top channels. Traditional sports betting leads product engagement, followed by casino/live dealer and lottery.

On responsible gambling, the combined 10% moderate-risk and problem-gambler rate aligns with European averages. It will, however, face increased scrutiny under the DGOJ’s forthcoming mandatory risk-detection algorithm, expected to roll out in 2026.

Navigating Spain’s next phase

The market has matured — but it’s still moving. A decade-old regulatory framework provides stability, yet the sector delivered 17.6% GGR growth in 2024 and rising Blask metrics through 2025.

Share is up for grabs. Bet365’s -3.79pp BAP decline demonstrates that dominance isn’t permanent. Domestic challengers with aggressive localization (Luckia +34.6% YoY, CasinoBarcelona +57.7% YoY) are proving that local knowledge and product adaptation beat assumed brand equity.

Regulatory tightening is the next variable. Joint deposit limits, standardized risk detection, and potential advertising restrictions are all in the pipeline. Operators with robust responsible gambling infrastructure will be better positioned when these measures take effect in 2026.

The football dependency is real. La Liga drives the seasonal pattern, El Clásico drives the spikes, and the June–July trough is predictable.

Blask metrics

- CEB (Competitive Earning Baseline) — an external, interval revenue benchmark (min–avg–max) in USD for a brand or country: what an operator should be earning given brand strength and today’s competition.

- APS (Acquisition Power Score) — an external, interval new-customer benchmark (min–avg–max): how many new users an operator should be acquiring at current brand strength and competitive intensity.

- Blask Index — a “stock-market index” of iGaming interest: total demand and how it’s shared among brands, built on the Share-of-Search relationship and cleansed for cross-country, cross-period comparisons.

- BAP (Brand’s Accumulated Power) — a percentage measure of brand strength as a share of category power, stable across swings in absolute market size, designed for cross-country and cross-period comparisons.