- Updated:

- Published:

Mexico iGaming market Q1 2026: brands, demand, and what changed

Demand grew 26.8% year-over-year — but the quarter was defined by a government enforcement standoff that froze major operators for months, forced court intervention, and handed challengers an opening they didn’t waste.

In November 2025, Mexico’s Financial Intelligence Unit (UIF) directed internet service providers to block access to 13 gambling platforms, including Bet365.mx and Betano.mx, over suspected money laundering linked to Grupo Salinas — Ricardo Salinas Pliego’s conglomerate, which operates both as concessions through TV Azteca. The SAT had a tax debt exceeding MX$51 billion (~US$2.8 billion) against Grupo Salinas.

Courts pushed back: a federal judge granted amparos in December 2025 and again in March 2026, ordering SEGOB to restore operations within three days. President Sheinbaum publicly condemned the rulings. The standoff was still unresolved at the end of the quarter.

That backdrop shaped Q1 2026’s numbers.

Total Blask Index — the aggregate of consumer search demand across all iGaming brands — reached 20.2 million, up 26.8% from 15.9 million in Q1 2025. The market added 10 active brands (145 vs. 135). Caliente extended its lead in absolute terms but lost relative share as faster challengers absorbed the market’s growth. Bet365 stayed flat while everything around it moved up.

Three stories define the quarter: Caliente’s transition from acquisition engine to retention machine, the Bet365/Betano enforcement saga and its market-wide ripple effects, and the explosive rise of a new challenger tier that doubled and tripled demand in 12 months.

About the data: The Blask Index measures consumer search demand for iGaming brands. BAP (Brand Accumulated Power) shows each brand’s share of total market demand. APS (Acquisition Power Score) estimates new customer acquisitions per period. CEB (Competitive Earning Baseline) estimates revenue based on brand strength and competitive positioning — always expressed as a min–avg–max range because market conditions create a spectrum of outcomes. All figures for Mexico, Q1 2026 (January–March).

Track Mexico in real time → blask.com/market/mexico

Market demand in Q1 2026

Mexico’s total Blask Index grew from 15.9 million in Q1 2025 to 20.2 million in Q1 2026 — a 26.8% jump and the strongest Q1 on record in Blask’s Mexico dataset. Active brand count rose from 135 to 145, meaning new entrants contributed meaningfully to the aggregate.

Quarter-over-quarter, total CEB declined 2.8% versus Q4 2025 ($526.2M vs. $541.2M). This is a standard seasonal pattern: Q4 concentrates Liga MX Apertura finals, Champions League group stage, and year-end engagement peaks. Q1 typically softens slightly before recovering mid-year. The 2.8% dip is well within the normal range and doesn’t signal demand contraction.

The number that matters: the market’s estimated quarterly revenue reached $526.2M on average ($385.2M–$949.2M range). That’s up $100.9M, or 23.7%, year-over-year. Mexico is now comfortably the largest regulated iGaming market in Latin America by revenue — a position it is unlikely to relinquish soon given its 125 million population, mobile-first user base, and deep sports betting culture built around Liga MX and national team fixtures.

Local vs international: how the market splits

Mexico is a regulated market on both casino and sports betting, governed by SEGOB concessions. The data shows what that means commercially.

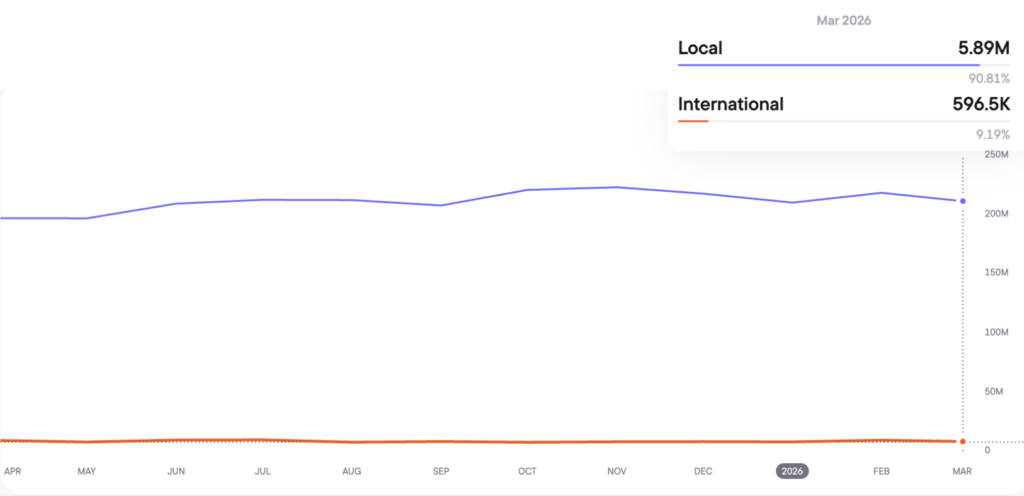

In Q1 2025, licensed local (Onshore) operators held 93.3% of total search demand. By Q1 2026, that share had narrowed to 91.2% — a shift of 2.1 percentage points toward international (Offshore) operators.

On revenue, the shift was identical: Onshore CEB fell from 94.8% to 92.8% of the quarterly total, while Offshore rose from 5.2% to 7.2%.

| Q1 2025 | Q1 2026 | Change | |

|---|---|---|---|

| Blask Index — local | 93.3% | 91.2% | –2.1 pp |

| Blask Index — international | 6.7% | 8.8% | +2.1 pp |

| CEB — local (avg/month) | $134.4M (94.8%) | $162.8M (92.8%) | +21.1% |

| CEB — international (avg/month) | $7.3M (5.2%) | $12.6M (7.2%) | +71.6% |

Two dynamics are at work here.

- First, the absolute growth in offshore CEB (+71.6% YoY) is striking — but it’s growing from a small base, and offshore operators still underperform their demand share. International brands hold 8.8% of search demand but only 7.2% of estimated revenue, a gap of 1.6 percentage points.

In most markets, offshore operators punch above their demand weight on revenue because their CEB-per-player is higher. In Mexico, the reverse holds: licensed local operators — Caliente above all — are significantly more efficient at converting demand into revenue.

That reflects Caliente’s depth in local payment rails, brand recognition embedded in Liga MX stadium signage, and a decade of trust-building that international entrants haven’t matched. - Second, the direction of travel is clear: Offshore demand and revenue share both grew by 2.1pp in a single year. That shift is faster than most regulated markets. The UIF crackdown on Bet365/Betano may have contributed — disrupted onshore operators lost demand share, and some of that migrated to offshore alternatives.

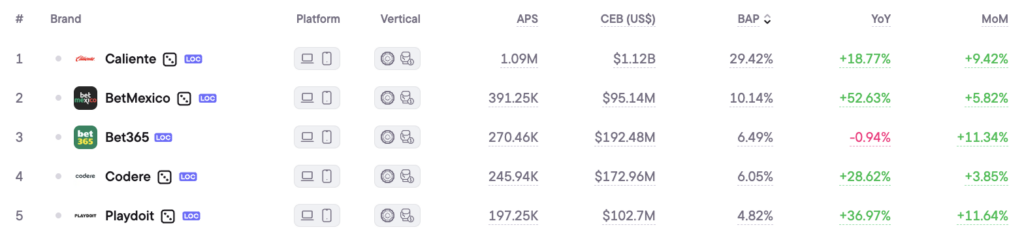

Top brands in Q1 2026

| Brand | Rank | APS (Q1 total) | CEB avg (Q1 total) | YoY demand |

|---|---|---|---|---|

| Caliente | 1 | 196,822 | $239.8M ($179.9M–$419.7M) | +18.8% |

| BetMexico | 2 | 80,271 | $21.4M ($16.0M–$37.4M) | +52.6% |

| Codere | 3 | 48,134 | $36.6M ($27.5M–$64.1M) | +28.6% |

| Bet365 | 4 | 33,006 | $33.4M ($25.0M–$58.4M) | –0.9% |

| Playdoit | 5 | 48,659 | $24.1M ($18.1M–$42.2M) | +37.0% |

| AFun (MX) | 6 | 35,582 | $6.6M ($5.0M–$11.6M) | +547.7% |

| Betmaster | 7 | 31,107 | $8.3M ($6.2M–$14.5M) | +104.0% |

| Rushbet | 8 | 28,668 | $9.1M ($6.9M–$16.0M) | +58.5% |

| Brazino777 | 9 | 26,042 | $7.1M ($5.3M–$12.5M) | +168.3% |

| Novibet | 10 | 26,682 | $12.7M ($9.5M–$22.3M) | +98.8% |

Ranked by BAP (Blask Index share). APS = estimated new customer acquisitions for the quarter. CEB = estimated quarterly revenue (avg, with min–max range).

Caliente remains Mexico’s dominant brand by a wide margin. Its estimated quarterly revenue of $239.8M represents 45.6% of total market CEB — on roughly 22% of APS. That gap between revenue share and acquisition share tells a specific story: Caliente is converting its existing base at a significantly higher rate than competitors, even as its new-user acquisition declined 3.1% versus Q1 2025. The brand is maturing. It’s no longer the fastest-growing operator in Mexico — but it extracts more value per player than anyone else.

BetMexico is the most interesting story in the top five. Up 52.6% YoY and now clearly the #2 brand, it grew faster than Codere, Bet365, and Playdoit combined. Its APS of 80,271 — double that of Codere and Playdoit — suggests it’s winning the new-user battle aggressively. The brand’s CEB of $21.4M is lower than Codere’s $36.6M despite higher APS, indicating it’s acquiring more users but monetizing them at a lower rate than the more established local brands.

Bet365 held rank 4 but grew –0.9% YoY while the market grew 26.8%. That’s a relative loss of approximately 21 BAP percentage points in competitive terms. The brand was blocked by UIF in November 2025 and only partially restored through amparos in December and March. Its MoM recovery rate by March (+11.34%) suggests demand bounced as access was restored, but Q1 as a whole reflects a brand that spent most of the quarter offline or constrained.

The real story below rank 5 is the new challengers. AFun (MX) grew 547.7% YoY, rising from obscurity to #6. Brazino777 — a Brazilian brand that expanded into Mexico — grew 168.3%. Betmaster more than doubled (+104%). Novibet was close behind (+98.8%).

All four entered or accelerated during a period when Bet365 and Betano were suppressed. Whether that’s correlation or causation is impossible to separate cleanly, but the timing is precise: the UIF blocking in November 2025 removed two well-funded international brands from active marketing at exactly the moment these challengers were scaling acquisition spend.

What drove the quarter

The Bet365/Betano affair. This was the defining event not just for those two brands but for the whole market. The UIF’s November 2025 blocks were framed as anti-money laundering enforcement, but the underlying dispute involved a tax debt of over MX$51 billion between the SAT and Grupo Salinas — which controls both platforms through TV Azteca concessions. Courts repeatedly overruled SEGOB: a federal judge in December 2025, another in January 2026, and a second federal court in March 2026. President Sheinbaum publicly criticized the judiciary for blocking her government’s enforcement actions. The legal outcome remained contested at the end of Q1. The market impact was immediate: two of Mexico’s top four brands spent Q1 in partial or total suspension, and the resulting demand vacuum flowed to everyone ranked below them.

The 2026 Fiscal Package. Mexico’s 2026 Fiscal Package raised the IEPS (excise tax) on gambling to 50% and required all platforms to register with tax authorities and withhold applicable taxes in real time. The SAT also gained authority to access real-time transaction data. This is a structural cost increase for every operator in the market. It likely contributed to Bet365’s monetization challenges and may explain why some challengers — including offshore-adjacent brands like AFun and Brazino777 — gained disproportionate traction: they operate with different cost structures and regulatory exposure.

New Federal Gaming Law proposal. In October 2025, Congressman Ricardo Mejía Berdeja proposed a new Federal Gaming Law to replace legislation dating to 1947. The bill would create a National Institute of Games and Sweepstakes, introduce responsible gambling tools, and establish a 21-year minimum age. Codere CEO Aviv Sher put it bluntly: “Mexico does not have real regulation, but concessions from the mid-20th century.” If passed, the law would restructure the entire licensing framework. No timeline is confirmed, but the proposal is active in Congress. Operators with existing concessions — Caliente, Codere — are watching closely.

Operator moves. In March 2026, RubyPlay and Codere Online announced a content partnership to expand Codere’s casino offering in Mexico. Separately, REEVO went live with Betsson in Mexico in March — a signal that international brands are still entering the market despite the regulatory uncertainty. Betsson doesn’t yet appear in the top 10, but content partnerships and tech investments typically precede BAP growth by 1–2 quarters.

Q1 2026 vs Q1 2025 — year-over-year shift

| Metric | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total Blask Index | 15,943,961 | 20,223,652 | +26.8% |

| Blask Index — local share | 93.3% | 91.2% | –2.1 pp |

| Blask Index — international share | 6.7% | 8.8% | +2.1 pp |

| Market leader | Caliente | Caliente | — |

| APS avg (quarterly) | 738,677 (537K–1,342K) | 890,707 (643K–1,635K) | +20.6% |

| CEB avg (quarterly) | $425.3M ($313.5M–$760.9M) | $526.2M ($385.2M–$949.2M) | +23.7% |

| CEB — local share | 94.8% | 92.8% | –2.0 pp |

| CEB — international share | 5.2% | 7.2% | +2.0 pp |

| Active brands | 135 | 145 | +10 |

The structural shift is clear: the market grew in every direction, but locally licensed operators are losing ground to international brands — slowly, but consistently. The 2.1pp demand shift toward offshore in a single year is the fastest such movement in Blask’s Mexico dataset. Regulatory turbulence is the most likely driver: when established licensed operators face enforcement actions, the beneficiaries are brands that operate outside that framework.

What this means for operators

Mexico is growing fast and getting harder to enter cheaply. The top five brands are pulling ahead in both demand and revenue, and Caliente’s monetization advantage over the field is expanding, not contracting.

For operators considering the market, the Q1 data suggests two viable entry paths: go direct at sports-betting acquisition (where BetMexico’s +52.6% growth proves it’s still possible to scale against Caliente), or build through content and product investment now, ahead of the 2026 FIFA World Cup in June — which Mexico co-hosts and which will produce the largest betting demand spike this country has ever seen. The operators that have their tech stack and licensing in order by May will have a structural advantage for the quarter that matters most.

The regulatory situation introduces real uncertainty. The 50% IEPS tax raises the cost floor for every licensed operator. The proposed Federal Gaming Law, if passed, would reset licensing rules from scratch. Any Q2 planning should include legal and tax scenario analysis — not as a compliance checkbox, but as a commercial input.

Conclusion

Mexico’s Q1 2026 numbers confirm what the market structure has been signaling for two years: demand is growing faster than any single operator can capture, local licensing protects incumbents but doesn’t guarantee efficiency, and enforcement actions — no matter who initiates them — create openings that faster, lighter challengers exploit.

Caliente will likely hold its #1 position through the World Cup cycle. But the margin between it and a resurgent Bet365, a surging BetMexico, and an AFun that wasn’t even on the map 18 months ago is compressing. Q2 2026 will be shaped by which operators show up to the World Cup with momentum — and which are still fighting in court.