- Updated:

- Published:

UAE regulated iGaming market opens: Play 971 launches as Blask Index surges 44% in 2025

UAE launches licensed iGaming: Blask Index surges 44% before Play 971 enters high-income expatriate market.

Play 971 launched this week as the UAE’s first licensed online casino, marking the region’s official entry into regulated iGaming. This is a logical response to growing iGaming demand: Blask Index grew 44% since January, while CEB (Competitive Earning Baseline) surged 82% at its average value.

Below we break down the market structure, regulatory timeline, and operator opportunity for this newly-regulated market.

What happened: Play 971 soft launch marks UAE’s regulated iGaming entry

Play 971 went live this week as the UAE’s first fully licensed online gaming platform, receiving authorization from the General Commercial Gaming Regulatory Authority (GCGRA). The platform is currently in a soft launch phase, available in Abu Dhabi and Ras Al-Khaimah, with an official full rollout planned for Q1 2026.

The site is operated by Coin Technology Projects LLC, an entity linked to Momentum LLC — the company behind the UAE Lottery, which launched in November 2024 and distributed over AED 147 million in prizes in its first year. Play 971 offers casino games, sports betting, and racing, representing the first licensed online products beyond lottery offerings in the country.

The regulatory timeline: building toward iGaming

The UAE’s iGaming framework began forming in September 2023 with the establishment of GCGRA, a federal regulator with exclusive jurisdiction to license and oversee all commercial gaming operations.

Regulatory milestones:

- September 2023: GCGRA established

- July 2024: The Game LLC awarded UAE Lottery license

- November 2024: UAE Lottery officially launches

- October 2024: Wynn Resorts licensed for casino resort (opening 2027)

- November 2025: Play 971 becomes first licensed iGaming platform

Why now: economics meet regulation

The decision to legalize online gaming stems from several converging factors. First, 88% of the UAE’s population consists of expatriates — many already accessing offshore platforms. Second, the government aims to monetize this demand through taxation rather than allowing revenue to flow to unregulated competitors. Third, the development of major tourism assets like the Wynn resort requires legal gaming as a competitive draw for international visitors and investment capital.

Additionally, the Emirati government maintains a careful balance: while citizens remain prohibited from gambling, the expatriate-dominated population creates a substantial revenue opportunity without implications for domestic social policy.

Blask data: quantifying growing demand

Blask tracked iGaming activity in the UAE throughout 2025 as the regulatory framework progressed toward official market launch.

Pre-Launch market signals

The data reveals extraordinary demand accumulation:

- Blask Index: 44% growth since January (576,900 → 830,700)

- CEB (Competitive Earnings Baseline): 82% growth ($74.09M → $135.8M)

These figures underscore that substantial player bases from the UAE have been actively engaged with offshore platforms. Blask data shows that 160 gaming brands were operating in the UAE as of November 2025, underscoring the scale of player demand that remained unmet by licensed operators.

Market structure: Consolidation by design

The GCGRA’s regulatory framework permits a maximum of one licensed iGaming operator per emirate, meaning the theoretical market cap is seven operators total. However, each emirate independently decides whether to legalize online gambling, so not all seven licenses will necessarily be issued.

Play 971 currently operates in two emirates (Abu Dhabi and Ras Al-Khaimah), leaving five potential licenses available across the remaining emirates, though industry analysts expect only two or three emirates to ultimately adopt iGaming regulations.

This contrasts sharply with traditional market liberalization, where multiple operators usually compete aggressively. Instead, the UAE has engineered a consolidated market structure:

- For the leading operator (Momentum): Stable unit economics and guaranteed profitability without fierce competition

- For aspiring operators: Extreme barriers to entry; only world-class organizations will qualify for the remaining licenses

- For mid-tier players: Virtually no pathway into the market

What this means

For operators: The UAE presents a rare opportunity — regulated scarcity meets a concentrated base of high-income players, creating premium unit economics unavailable in competitive markets.

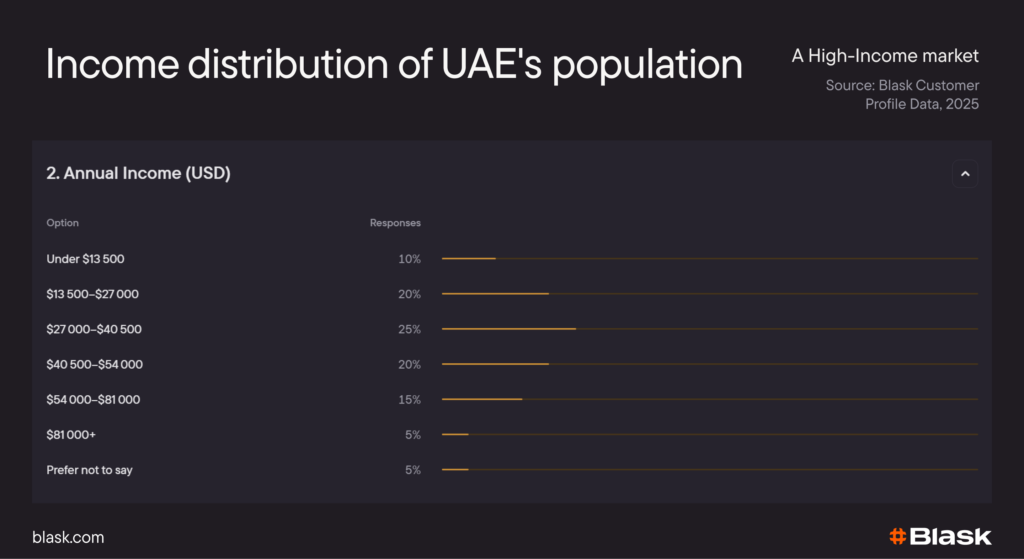

Blask data shows that 90% of the addressable population earns above $13,500 annually, with 25% earning $27,000–$40,500 and 20% exceeding $54,000

For the industry: Play 971’s success could signal a model for other countries considering iGaming legalization, particularly those balancing tourism and investment opportunities with religious and cultural values.

For players and investors: Blask’s pre-launch data tells the decisive story: 44% Blask Index growth and 82% CEB expansion in eleven months confirms that suppressed demand is real and substantial. The moment regulated platforms become accessible, the player migration from offshore to licensed sites accelerates dramatically.

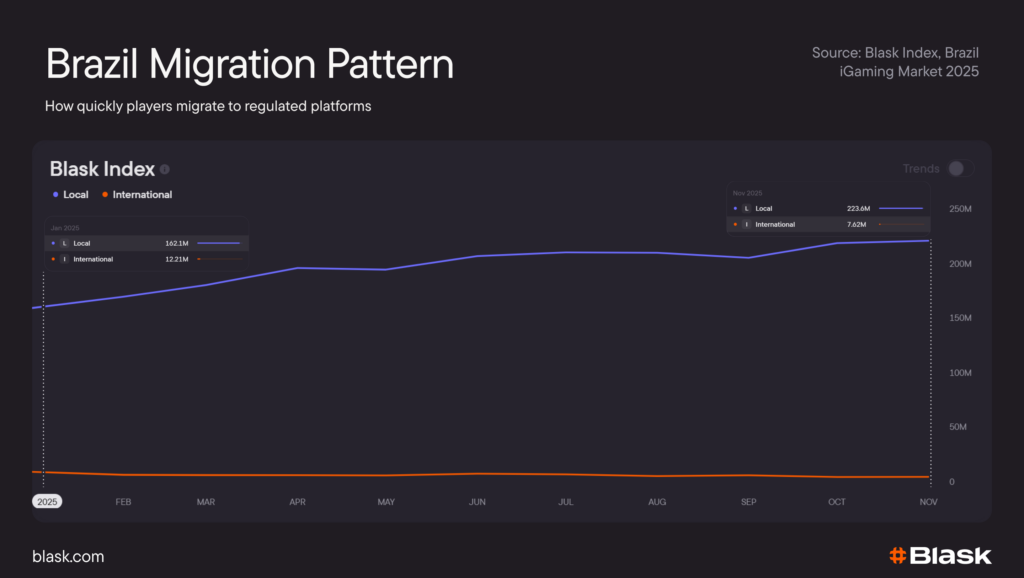

In Brazil, where the regulated market launched on January 1, 2025, licensed operators captured 93% of Blask Index traffic within the first month — a share that grew to 97% by November. This demonstrates that player preference for regulated, safer platforms is immediate and powerful, not gradual.

This same migration pattern is likely underway in the UAE, where 160 offshore brands currently compete for players who will soon have a regulated alternative.