Ontario market-leader Betty is set to expand into the UK and Alberta, marking the operator’s first major attempt to scale its casino-only model beyond its domestic borders.

The company is launching in the UK, one of the world’s most mature and tightly regulated iGaming markets, while also preparing a full rollout in Alberta after registering with the local regulator.

Betty is growing without following the industry’s broader shift toward “super apps” built around sports betting. Its focus on casino-only allows the brand to compete with major global operators rather than simply defend a niche position.

Betty proves the strength of the casino-only model

Until recently, Betty operated only in Ontario, but the market has already shown that a narrow casino-only strategy can scale. The operator does not build growth around sportsbooks, esports or poker. Its focus is on slots, live casino and online bingo.

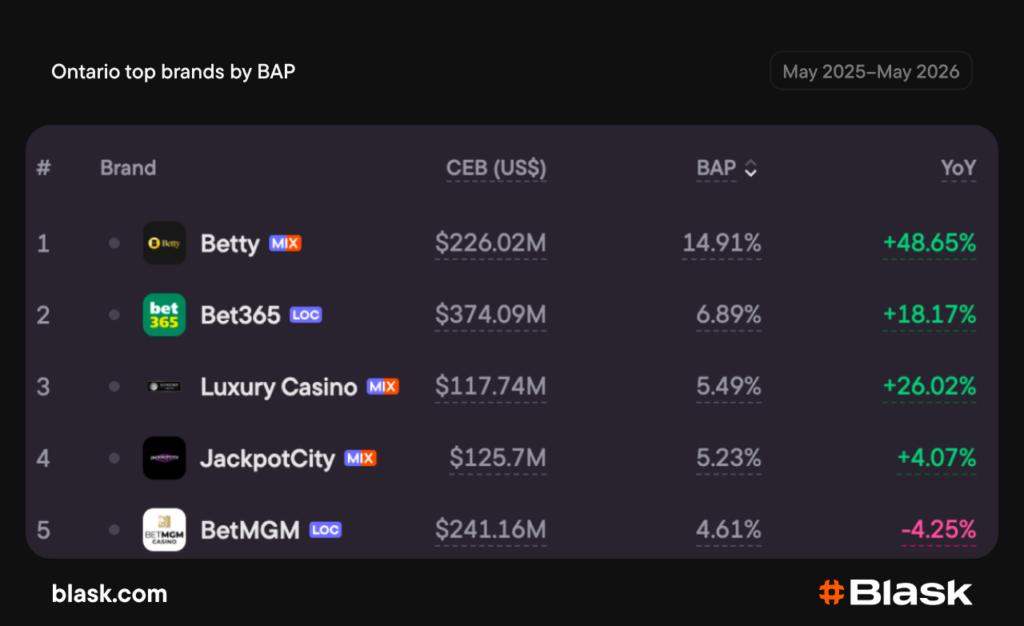

Blask data shows that Betty ranks first by BAP among 292 tracked brands in Ontario. In the top five, only Bet365 and BetMGM have sportsbook exposure, while Betty, Luxury Casino and JackpotCity are casino-first brands. In Canada, a large share of unbranded demand sits in casino categories — which means casino-led operators can compete directly with multi-vertical platforms.

Betty’s Ontario position also keeps strengthening — demand is up 8.92% MoM, building on already dominant BAP.

The UK compliance test

Betty’s UK launch on June 1, 2026 marked the company’s first move beyond Canada. Unlike Ontario, the UK market is already distributed among several large operators, which makes entry difficult for a new brand. The top BAP positions are held by local players with strong brand recognition, broad product lines and established user bases.

The ranking also shows that bingo is already part of the UK casino mix. Gala Bingo ranks eighth by BAP, with $429.63M in CEB and 10.82% YoY growth. For Betty, which has built part of its Canada strategy around iBingo, this gives the UK launch a clearer product logic, even if the competitive baseline is much higher than in Ontario.

Regulatory pressure adds another layer of difficulty. Mandatory affordability checks, slot stake limits and strict marketing controls directly affect the economics of casino traffic.

To reduce upfront costs, Betty is entering through a decentralized model, giving local teams access to its software and platform rather than building a full local operation from day one. The model lowers CapEx, but makes brand safety heavily dependent on the compliance standards of local partners.

Scaling the Canadian experience

Alberta is the natural next step for Betty because it gives the operator a chance to carry its Ontario playbook into another regulated Canadian market, where casino demand already creates a clear entry point for the brand.

The UK launch is a more difficult test because Betty is entering a mature market shaped by long-standing betting brands, broad product portfolios and heavy competition for player attention. The presence of Gala Bingo in the UK top 10 shows that bingo-led casino demand exists, which makes Betty’s iBingo focus relevant, but the market also sets a much higher bar for product differentiation.

For Betty, the next phase therefore runs on two tracks: scaling a proven Canadian casino-only model in Alberta, and testing whether the same focus can hold up in a market where betting heritage still defines much of the competitive landscape.