- Updated:

- Published:

Ohio wants to ban online sports betting. 79.8% of demand is already with operators the state can’t touch

Four Republican representatives introduced the Save Ohio Sports Act on April 8, targeting Ohio’s $10 billion online betting market. Blask data shows the bill would directly affect only a fraction of where actual demand lives.

What the bill proposes

Reps. Riordan McClain, Gary Click, Johnathan Newman, and Kevin Ritter unveiled the Save Ohio Sports Act at the Ohio Statehouse on April 8, backed by the Centre for Christian Virtue, the Ohio Suicide Prevention Foundation, and addiction specialists from the Lindner Center of Hope.

The bill’s core provisions:

- End all app-based sports betting in Ohio

- Confine legal wagering to the state’s four land-based casinos

- Cap individual bets at $100 with a maximum of eight bets per day

- Eliminate prop bets, parlays, in-game wagering, and all collegiate sports betting

- Prohibit credit card deposits

- Bar sports betting ads during live broadcasts and inside professional venues

The sponsors describe it not as a regulatory update but as a full rewrite of Ohio’s wagering framework — one designed to add friction, slow access, and reduce what they call “fast, repetitive betting.”

Ohio legalized sports betting in December 2021 through House Bill 29. Both retail and online wagering launched simultaneously on January 1, 2023. Governor Mike DeWine signed that law. He has since publicly expressed regret, calling the market “a huge problem among young males up to 45” and telling reporters in November he would sign a repeal if it reached his desk — though he doubted the votes were there.

Ohio’s sports betting market in numbers

Ohio has become one of the top sports betting markets in the country in just three years. Ohioans wagered more than $10 billion on sports in 2025, generating $1.04 billion in taxable revenue — up 15.6% from 2024. At Ohio’s 20% tax rate, the state collected roughly $209 million for the year, most of it distributed to K–12 education.

More than 98% of all wagers are placed online. In November 2025 — Ohio’s record-breaking month with $1.15 billion in handle — online betting represented 98.5% of total wagers.

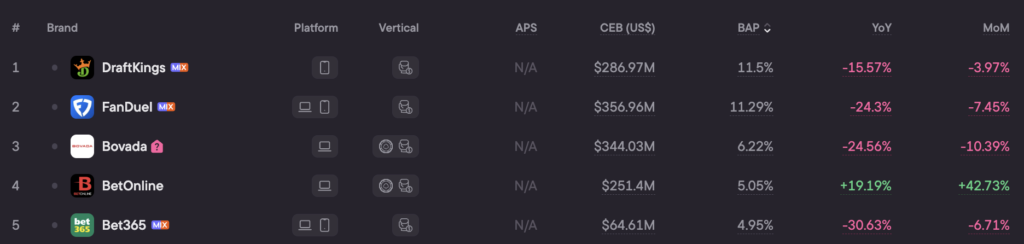

Ohio’s top brands by Blask demand

Blask Index measures consumer demand for gambling operators by aggregating Google search signals — how actively users in a market are looking for specific brands. It reflects real user intent, not marketing spend or operator self-reporting.

For Ohio (April 2025 to March 2026), Blask tracks 346 brands in the state, with 314 active. Combined market Blask Index: 3.6 million. Total market CEB (Competitive Earning Baseline) stands at roughly $4.36 billion.

What is CEB? The Competitive Earning Baseline is Blask’s AI-driven revenue projection for a market or brand — what operators should realistically capture given current demand signals, competitive dynamics, and market conditions. It is built from search behavior and external data, not operator P&Ls, and is expressed as a range to reflect different competitive scenarios.

Two findings stand out. Four out of five major brands show declining year-over-year demand — the regulated market is maturing and contracting even as handle grows. And two of Ohio’s five most sought-after brands — Bovada and BetOnline — operate without local license.

79.8% of Ohio’s earning baseline is already offshore

Blask’s onshore/offshore split of the Ohio CEB is the most consequential number for understanding what the Save Ohio Sports Act would actually do.

Over the 12 months from April 2025 to March 2026, offshore operators — brands active in Ohio without a local sports betting license — accounted for 79.8% of Ohio’s total $4.36 billion competitive earning baseline. Licensed onshore operators captured the remaining 20.2%, roughly $880 million.

This does not mean unlicensed platforms collect 79.8% of Ohio’s actual revenue. CEB is a demand-side projection, not an accounting figure. But the ratio reflects where user intent is concentrated — and that concentration has held steady through every month of the past year.

Bovada and BetOnline operate in the regulatory grey zone that exists in every US state: they hold licenses in offshore jurisdictions (typically Curaçao or Panama), accept American users, and are not subject to state-level sports betting regulation.

An online ban would not reach most of the market

The Save Ohio Sports Act’s logic is that removing app-based access adds friction that reduces harmful betting behavior. That reasoning applies to the 20.2% of Ohio demand flowing through licensed platforms.

It applies less clearly to the 79.8% flowing offshore — which would remain accessible regardless of what the Ohio legislature does.

BetOnline is already showing signs of gaining ground: its Blask Index rose 19.2% year-over-year in Ohio, and 42.7% month-over-month in March 2026. That growth is happening while licensed operators are losing demand — FanDuel -24.3% YoY, Bet365 -30.6% YoY, DraftKings -15.6% YoY. The pattern suggests some demand is already migrating from regulated to unregulated channels.

A complete online ban at the state level would not eliminate online betting for Ohio residents. It would shift remaining licensed-platform demand to platforms with no consumer protections, no self-exclusion tools, no responsible gambling infrastructure, and no tax contribution to Ohio’s schools or problem gambling fund.