- Updated:

- Published:

Australian iGaming: a market where money does not follow demand

Blask data shows that offshore operators capture the majority of Australian iGaming revenue despite holding less than 30% of user demand.

Recent tightening in enforcement helped licensed iGaming brands in Australia capture the vast majority of user demand. Except for one jurisdiction, where the population structure works against them. Yet the money still leaks offshore in almost all Australian states and territories.

A market that keeps dropping

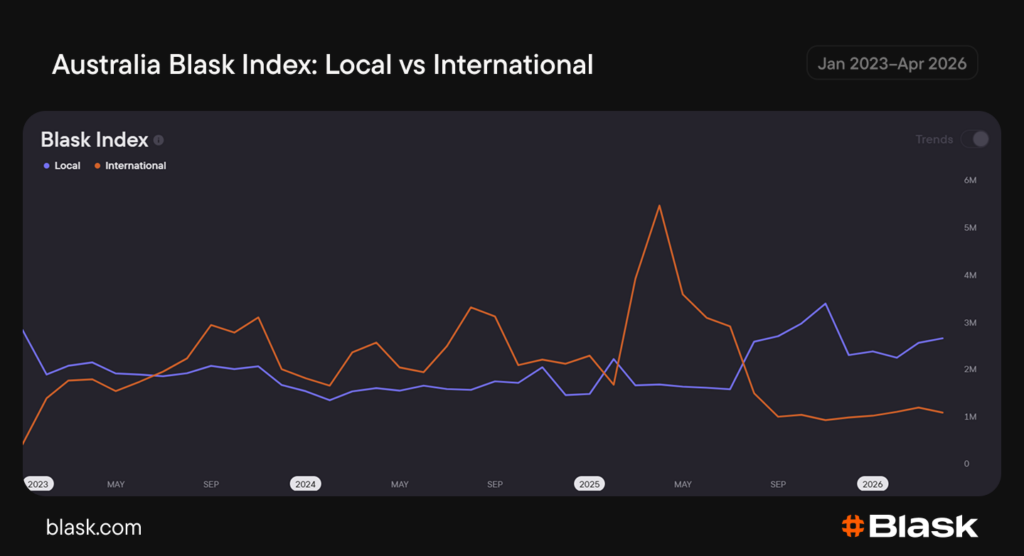

Australia is one of the largest iGaming markets globally, ranked 9th by projected revenue (CEB) for the past 12 months (May 2025-April 2026 period). But it is a declining market. Back in 2023 Australia ranked 5th, in 2024 — 6th, in 2025 — 7th, and now it is 9th by CEB.

In absolute CEB numbers, the market is declining as well. The country’s projected revenue in 2025 fell by 8.8% compared to 2024 and was only 6.9% higher than in 2023

At the same time, Blask Index in Australia rose 13.3% in 2025 compared to 2024, but for the May 2025-April 2026 period, it fell 9.1% on a year-over-year basis. The decline in demand is driven by the offshore segment. It hit its April 2025 peak and has been dropping, while Blask Index of licensed brands has been rising since July 2025.

The rise of Blask Index, though, did not bring the money to the licensed sector. In terms of CEB the Australian market belongs to offshore brands.

High channelization, low revenue capture

The iGaming regulation framework in Australia was set up at the federal level in 2001, introducing a national ban on online casinos while allowing states and territories to license online sports betting. The core rules never changed, but 2017 reforms strengthened enforcement against illegal offshore gambling services.

Since 2023 the system has been evolving by implementing stricter consumer laws, notably banning credit cards, eliminating crypto wagering, and phasing out gambling advertisements during live sports.

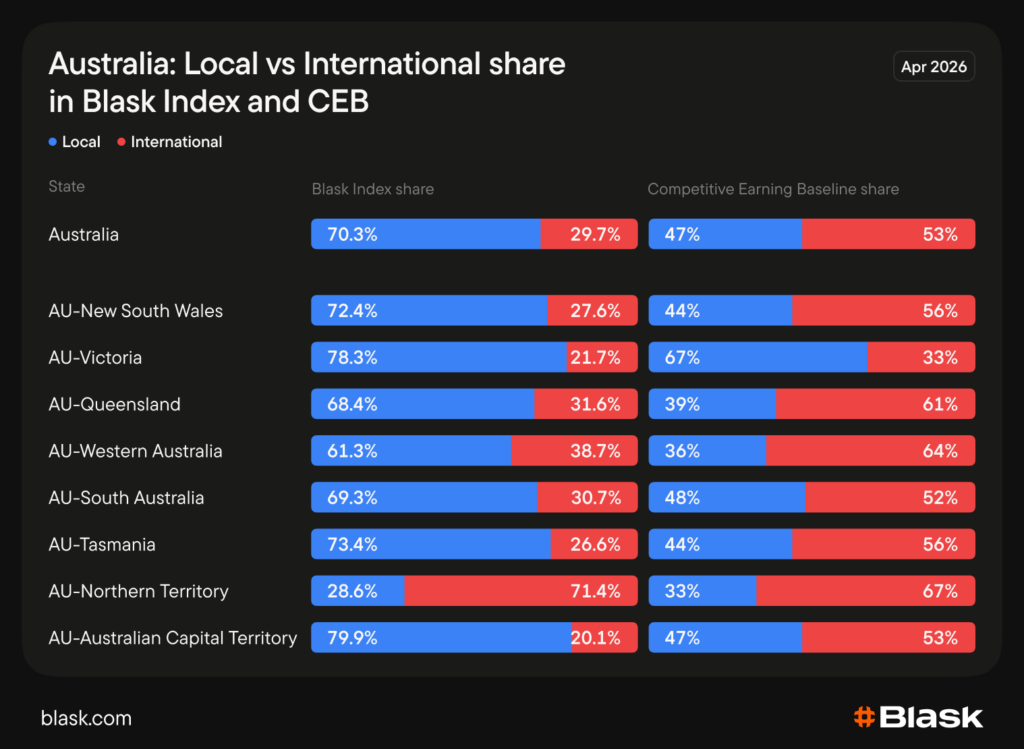

Demand for licensed iGaming brands is significantly higher than the demand for the offshore segment both on a country level and across almost all Australian states and territories. But the CEB picture is completely opposite.

The only exception for the offshore CEB domination pattern is Victoria, the second largest state in the country after New South Wales. Victoria has more than 26x the population of the Northern Territory, which is the only jurisdiction where licensed brands capture less demand than their offshore rivals.

In both markets, top 10 brands dominate demand, sharing 60.5% of Blask Index in the Northern Territory and 72.5% in Victoria. But Victoria has only two offshore brands among the top 10 while the Northern Territory has six, including the leading one — Winx96. As of April 2026 this brand shares 15.4% of the Northern Territory’s Blask Index, but less than 0.3% in every other jurisdiction.

An exception shaped by demographics

The core difference of the Northern Territory is its population structure. It is Australia’s smallest and most demographically distinct jurisdiction: a remote market with the country’s highest First Nations population share. According to the Australian Bureau of Statistics (ABS), Aboriginal people represent over 30% of the population in the Northern Territory, while in other jurisdictions no more than 6% (around 4% on country average).

A 2025 report by the government-backed Australian Institute of Family Studies stated that gambling harm is almost twice as prevalent among Aboriginal adults as among non-Indigenous people. That could explain the higher unlicensed-operator share in Blask Index, as offshore brands are outside Australia’s licensed harm-prevention system.

Bottom line

Australia is the 9th iGaming market by CEB, and most of the money goes to offshore operators. Licensed brands are yet to transform their leading position in demand into a higher revenue share. The only jurisdiction where offshore operators still have a higher demand is the Northern Territory, which statistically has the country’s most vulnerable demographic structure in terms of gambling harm.