- Updated:

- Published:

UK iGaming after the 40% tax: which brands are gaining market share while smaller operators exit

Blask data from the first three months of the UK’s 40% Remote Gaming Duty shows which operators are absorbing the blow — and which are already losing ground.

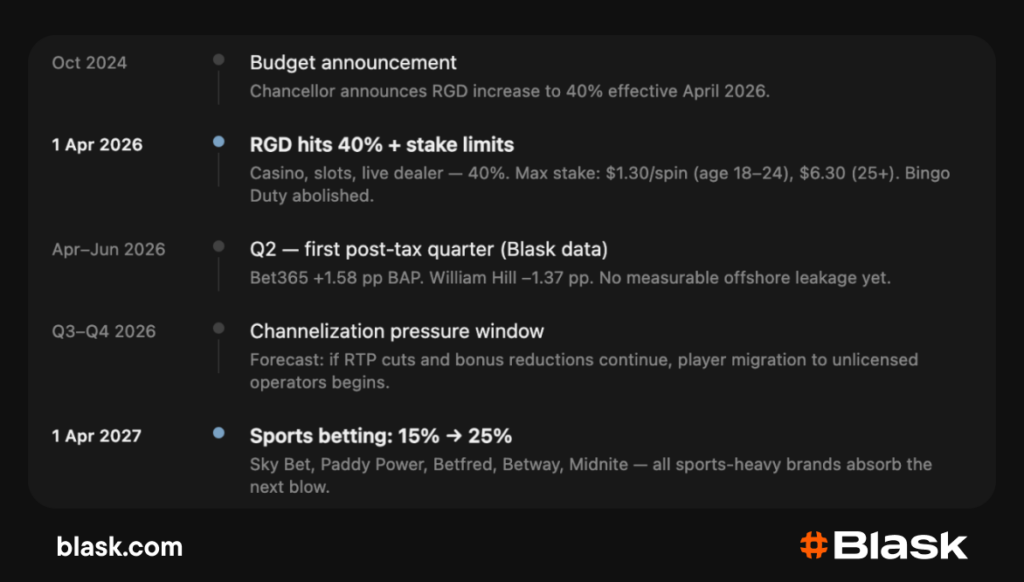

On 1 April 2026, the UK’s online gambling tax rose from 21% to 40% — the largest single increase in the history of the British market. The formal name is Remote Gaming Duty (RGD). Stake limits were introduced simultaneously: £1 maximum per spin for players aged 18–24, £5 for all others.

Blask tracks the UK market in real time and answers the question the entire industry is asking: which operators are winning under these conditions, and which are already losing market share?

The tax nobody could absorb equally

The arithmetic is simple and brutal: at 21%, an operator with $25M GGY (Gross Gaming Yield) paid $5.3M. At 40% — $10M. The $4.8M annual gap eats into EBITDA margins across the board, but not equally.

Flutter Entertainment estimated the net impact on adjusted EBITDA at $235M for 2026, after mitigation measures including reduced marketing and promotions. Entain recorded $255M in additional annual costs. Evoke — owner of William Hill — within 24 hours of the budget announcement launched a process to close 200 retail shops, putting 1.5K jobs at risk.

This is the first layer of the Flutter Entain bet365 UK market split: the largest operators are not exposed to the new tax in the same way. Tier-1 groups with diversified portfolios — international markets, sports betting, land-based retail — are absorbing the hit. Mid-tier and challenger brands without an international buffer are in a fundamentally different position.

One technical point matters here: the new 40% rate applies to remote gaming products — casino, slots, live dealer. Sports betting remains at 15% for now, with the new 25% rate only taking effect from April 2027. This is the core UK remote gaming duty 40% impact: casino-led operators absorbed the immediate blow, while brands with a stronger sports mix gained a temporary structural advantage. Bingo Duty was abolished entirely from April 2026 — bingo operators received a structural windfall at the moment the casino segment came under pressure.

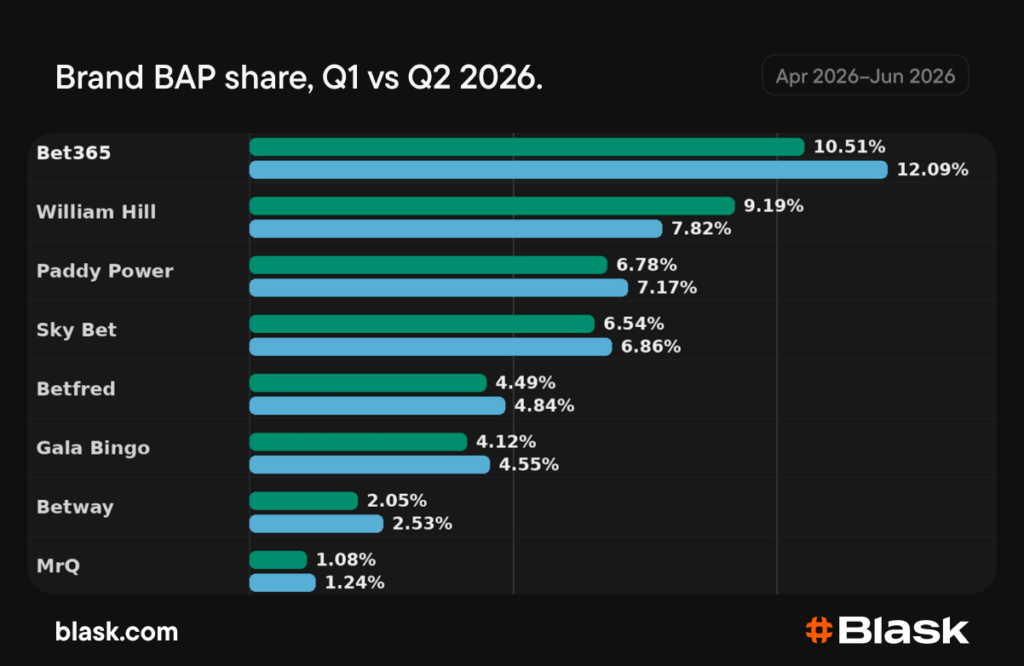

First post-tax quarter — UK market

Three months of data reveal a clear competitive split. Brands built on sports betting are capturing share while casino-heavy operators without international diversification are retreating — the tax rewrote the market’s competitive map in a single quarter.

Winners: sports product and scale:

Bet365 was the clear winner of the quarter. BAP rose from 10.51% to 12.09%, a gain of 1.58 p.p, while the brand grew 28% YoY. As the largest operator with a strong sports mix, bet365 is better positioned than most to absorb margin compression

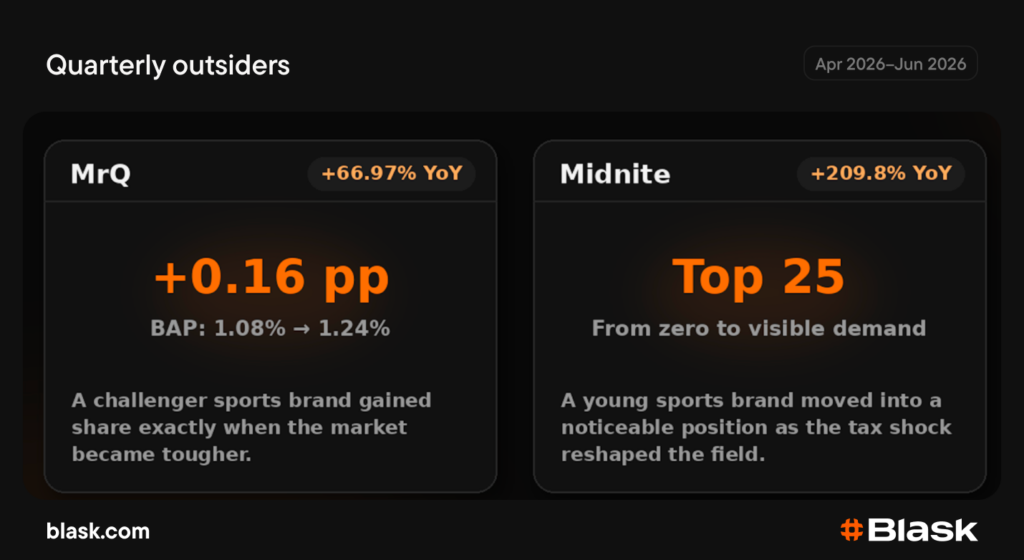

Flutter brands also moved higher. Paddy Power increased to 7.17% BAP after a 19.35% monthly jump, while Sky Bet rose to 6.86%, up 17.67% month on month. Betfred moved from 4.49% to 4.84%, and Betway added 0.48%, with YoY growth of 41.61%. Gala Bingo gained 0.43%, benefiting structurally from the removal of Bingo Duty in April 2026 — exactly as casino operators were hit by the higher tax burden.

The pattern

Sports-heavy brands with scale are gaining share. Casino-heavy operators without international diversification are losing ground. The tax shift rewrote the UK competitive map in a single quarter.

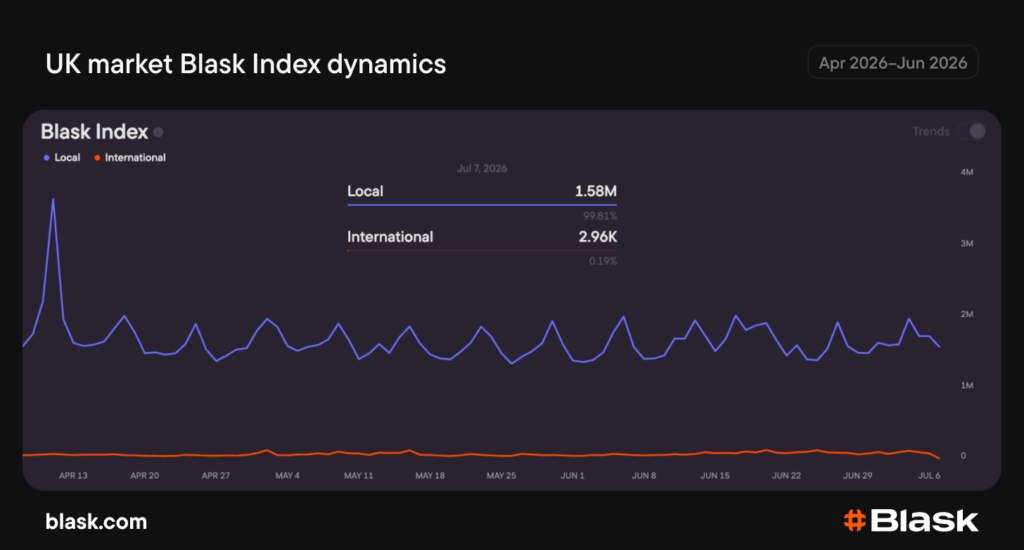

UK online casino operators 2026: no offshore shift yet, but pressure is building

Flutter CEO Peter Jackson publicly warned before April that the “big win” from tighter conditions would go to unlicensed operators. The UKGC received $33M in additional funding specifically to counter the black market.

Blask tracks the gap between licensed and offshore demand in the UK market. Data for April–June 2026 shows that offshore activity remains close to zero, in line with the January–March period. No measurable audience shift towards offshore is visible yet.

The risk has not disappeared, however: three months is too short a horizon for behavioural change. Slot RTP is falling and bonuses are being cut, but the gambling audience responds with a lag — real pressure on channelization may begin to emerge in Q3–Q4 if operators continue to squeeze terms.

April 2027 will hit those who are currently growing

From April 2027, the Remote Betting Duty rate will rise from 15% to 25%. The next blow falls on the brands currently performing most strongly. Sky Bet, Paddy Power, Betfred, Betway and Midnite all grew on sports betting, and will hold their accumulated BAP only if they absorb margin compression as effectively as the largest players handled the remote gaming duty.

From April 2027, sports-heavy brands will occupy the same position casino-heavy operators held in April 2026 — and unlike the first round, they will have no temporary structural advantage in the form of a lower tax rate.