- Updated:

- Published:

Russia’s offshore Gaming demand fell 66% – while licensed operators quietly grew

Russia’s offshore and licensed iGaming segments moved in opposite directions.

Between August 2025 and January 2026, three regulatory changes reshaped online iGaming demand: Russia’s gambling regulator (ERAI) accelerated its blocking of illegal sites past 200K domains, Telegram removed over 1M gambling channels, and the government reformed bookmaker taxation — replacing the fixed per-bet levy with 7% of GGR plus 25% profit tax.

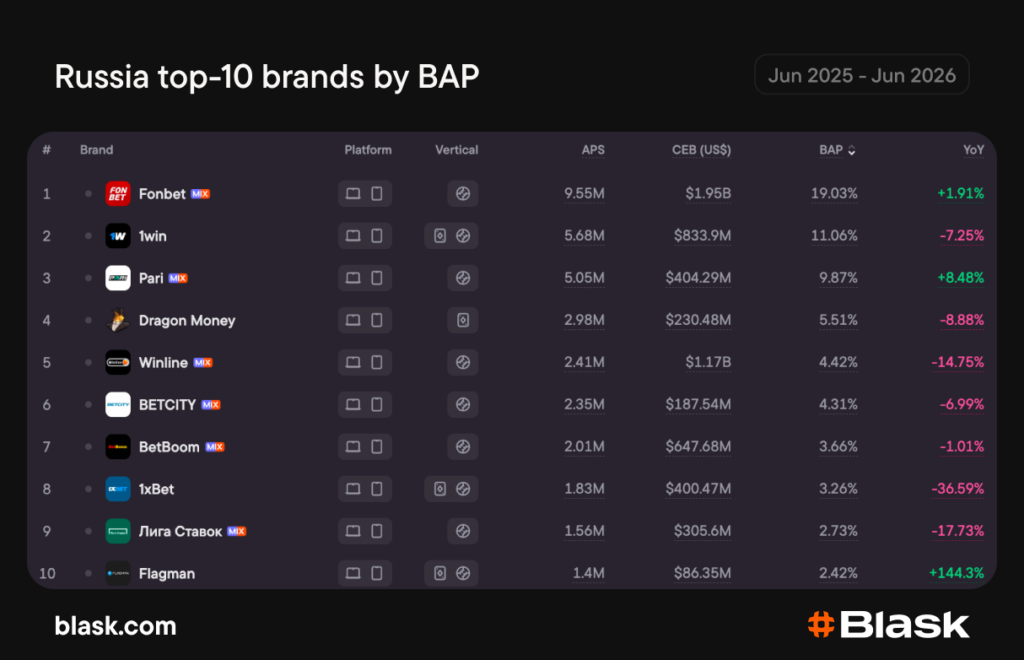

Blask Index for Russia dropped 34% overall compared to June 2025, but the decline is concentrated in the offshore segment: –66% YoY. Licensed operators grew 2%, consistent with ERAI’s official data (+8.4% in revenue). Blask captures both segments simultaneously — official reporting covers only the licensed segment.

Methodology note. Blask Index measures online brand demand — user search activity as a proxy for brand strength. It does not measure deposits, GGR, or revenue. Retail betting shops are not captured. The offshore segment is included — which is why Blask figures may differ from official ERAI reporting, which covers licensed operators only. A brand’s ranking reflects its share of online demand, not its revenue market share.

Site blockings and Telegram channel blockings cut two-thirds of offshore demand

Regulatory pressure on illegal gambling produced measurable results:

- ERAI blocked more than 200K illegal bookmaker sites by the end of 2025.

- In January 2026, Telegram removed over 1M gambling channels — the main distribution and affiliate traffic layer for offshore casino brands.

For 1xBet, the Central Bank also revoked licenses from payment companies serving the bookmaker, pushing Blask Index for the offshore segment down 66% YoY. 1xBet alone lost 36.6% — a clear illustration of how regulatory pressure shows up in demand data.

The licensed segment moved differently. Online demand for licensed operators grew 2% YoY, consistent with ERAI’s reported +8.4% in revenue. Among the top-10 operators, only Fonbet (+1.9%), Pari (+8.5%), and Flagman (+144.3%) ended the year positive. Fonbet and Pari partially absorbed the audience lost by offshore operators. Flagman’s 144% growth reflects a low-base effect: the brand launched roughly a year ago from near zero.

Not all licensed operators benefited equally

The new taxation model, effective January 1, 2026, complicated the picture for the licensed segment. Russia switched to 7% of GGR plus 25% profit tax, replacing the fixed per-bet levy.

For operators that had already committed to heavy marketing spend, the margin compression hit harder. Winline spent more than $450M on sponsorship contracts in 2025 — its second consecutive year at that level — and ended the year with declining revenue. Liga Stavok reported a 41% drop in net profit. These are licensed operators with real market presence; their decline reflects financial pressure.

A third factor accelerated the decline in Blask data: media buyers pulled back from Russia. The regulatory environment raised the cost and risk of buying traffic, while LatAm and Europe offered more predictable conditions — with the 2026 World Cup generating additional demand there.

The January tax shock hasn’t shown up in the data yet

Fonbet and Pari grew because the audience of blocked offshore operators had to go somewhere. The licensed market as a whole grew 2% — but with a growing tax burden, fewer entry points, and media budgets redirecting to other markets, the structural conditions for that growth are narrowing. Targeted contributions to the sports fund also rose — from 2% to 2.25% of revenue.

New illegal site blocking mechanisms signed in June 2026, and a self-exclusion system launching in September 2026, will add further pressure across the whole market — legal and grey alike. The January 2026 tax change has not yet fully appeared in operators’ annual reporting. According to market participants, without restructuring their business models, profitability could fall by up to 50%.

Negative YoY does not always signal a strategic mistake. In a market compressed by inflation and falling consumer spending, brand investment and short-term revenue rarely move together — operators building their position now are preparing for the next growth cycle.